Last month I discussed the long-term cycles in Australian house prices and whether prices are destined to keep rising, crash suddenly, or suffer a mild correction and then remain subdued for several years. In the past few weeks there has been an escalation in the national debate over how to make housing more affordable.

Giving buyers money inflates prices

There are two main ways to make houses more affordable - cut prices or give buyers more money. Bringing down house prices would be political suicide. Many recent buyers have so little equity in their houses that cutting prices via savage bank rationing or big interest rate hikes could trigger widespread defaults and a collapse in construction activity causing an economic recession.

Instead, governments have focused on making housing more affordable by giving buyers more money. Simple! Every state already provides free (ie tax-payer funded) gifts to first home buyers and there is a range of discounts and waivers of property taxes like stamp duties. The debate has recently turned to allowing buyers to use their retirement funds to buy housing. There has even been a proposal whereby the government (tax-payers again!) would contribute 25% of the cost for first home buyers. None of this works. Giving buyers more money to spend inflates prices even further.

Address availability of credit

The real problem is credit. High prices are a function of high levels of credit extended by ever-willing lenders to ever-willing borrowers. Bank regulations are skewed toward favouring housing loans over loans to businesses. Even after the massive losses on housing debts in the US, UK and much of Europe over the past decade, banks and their tame regulators still have their heads in the sand in thinking that housing debt is virtually risk-free.

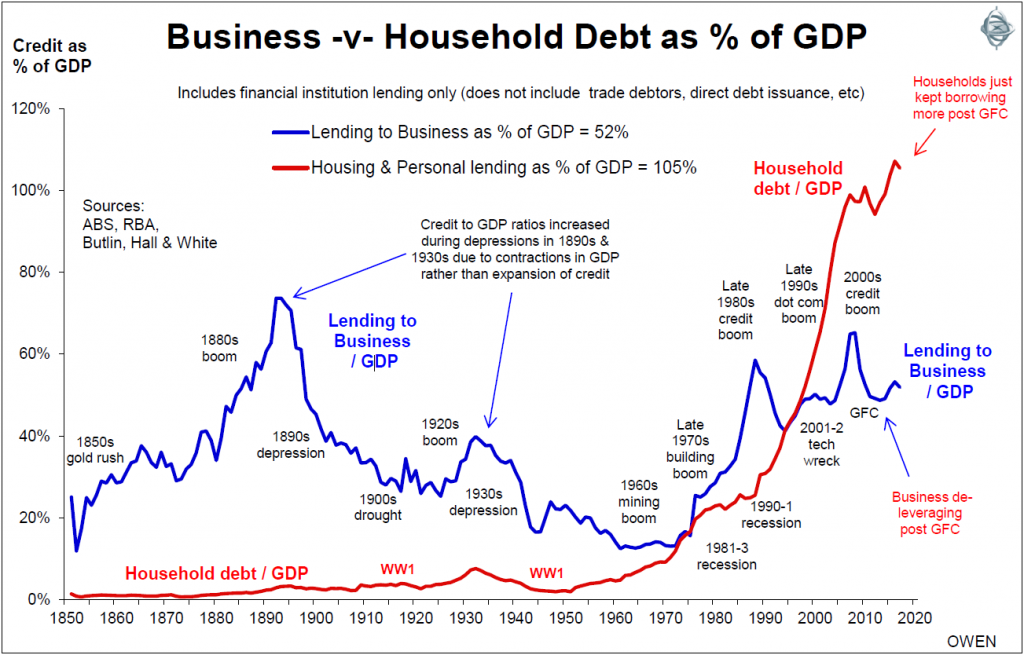

This chart shows lending to businesses and households in Australia as a percentage of national income since 1850.

There is something very worrying about this. The wealth and lifestyles we enjoy today were built by companies, and much of that was funded by business debt. In a healthy economy, household borrowing should not exceed business borrowing. Ever since bank deregulation and the housing-skewed bank capital rules (known as ‘Basel’) were introduced, lending on housing has swamped business lending. Household debt is now double the level of business debt.

After the GFC, companies in Australia and around the world de-leveraged. However Australian households piled on more and more debt thanks to our Reserve Bank’s rate cuts and bankers who keep on lending on ‘risk-free’ housing to keep their bonuses rolling in.

Business lending in the US and Europe has finally picked up, and that is driving their economic recoveries, especially the US. In Australia, it may take another crisis like the 1973-74 credit squeeze or the 1990-91 recession before regulators and banks return to a more healthy and productive balance between business and housing lending.

Ashley Owen is Chief Investment Officer at independent advisory firm Stanford Brown and The Lunar Group. He is also a Director of Third Link Investment Managers, a fund that supports Australian charities. This article is general information that does not consider the circumstances of any individual.