It started out as a news story about cars, not investing:

“When a Google self-driving car edged into the middle of a lane at just a bit over 3km/h on St Valentine’s Day and hit the side of a passing bus, it was a scrape heard around the world.”

Although the incident was big news in the car industry and at Google, it has no apparent connection to investing. But then the story took a delightful twist:

“The accident illustrates that computers and people make an imperfect combination on the roads. Robots are extremely good at following rules … but they are no better at divining how humans will behave than other humans are.”

Starting to sound familiar? Rather like markets and behavioural economics? Here’s the punch line:

“Google’s car calculated that the bus would stop, while the bus driver thought the car would. Google plans to program its vehicles to more deeply understand the behaviour of bus drivers.”

You gotta laugh. Good luck with that one, Mr Google. Will you be programming the bus driver who is texting, or the one who drank too many beers last night, or the one who fought with his wife as he left for the bus depot, or the one onto his fifth coffee?

Welcome to the world of investing and human behaviour which is anything but rational.

Behavioural finance and the struggle for explanations

Every human emotion plays out when investing, making financial markets unpredictable and struggling for a theory based on scientific evidence. We have covered the subject of behavioural finance many times in Cuffelinks, such as here and here. Often, investment decisions are driven by emotions rather than facts, with common behaviours such as:

- Loss aversion – the desire to avoid the pain of loss

- Anchoring – holding fast to past prices or decisions

- Herding – the tendency to follow the crowd in bursts of optimism or pessimism

- Availability bias – the most recent statistic or trend is the most relevant

- Mental accounting – the value of money varies with the circumstance.

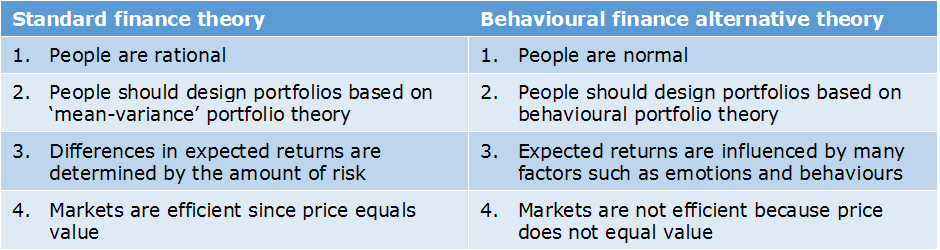

A new book to be published soon, written by Meir Statman, called Finance for Normal People, argues that the four foundation blocks of standard finance theory need rewriting, as follows:

The unfortunate truth is that if an investor went to ten different financial advisers, it’s likely they would end up with ten different investment portfolios. Investors have their own views on issues such as diversification, risk, active versus passive, efficiency, short run versus long run, etc, and often settle for ‘rules of thumb’ as a guide to investing. The bestselling book, Nudge, by distinguished professors, Richard Thaler and Cass Sunstein, quotes the father of modern portfolio theory and Nobel Laureate, Harry Markowitz, confessing about his personal retirement account,

“I should have computed the historic covariance of the asset classes and drawn an efficient frontier. Instead, I split my contributions fifty-fifty between bonds and equities.” (page 133)

That’s it! One of the greatest investment minds of the twentieth century simply goes 50/50. This is all the industry has achieved despite decades of research, complicated theories and multi-million dollar salaries paid to the sharpest minds from the best universities.

Economics as a ‘social science’

Why is investing so imprecise, replete with emotions and strategies with little supporting evidence, when other ‘sciences’ have unified theories? Why does a physicist know how gravity works, an arborist knows how a tree grows and a doctor can treat a patient with cancer, while fund managers around the world have different view on markets, stocks and bonds?

Consider Newton’s third law of motion:

“When one body exerts a force on a second body, the second body simultaneously exerts a force equal in magnitude and opposite in direction on the first body.”

There is no equivalent of this certainty in economics. For example, we do not know how the market will react when a central bank reduces interest rates. Maybe it happened because the economy is slowing, which is bad for the markets, and the hoped-for stimulus does not occur. And so the central bank plunges into unproven QE and even negative interest rates as it runs out of ideas.

Although economics pretends to be a ‘science’, it is a social science of politics, society, culture and human emotions.

It is often said that economics suffers from ‘physics envy’. Economists cannot test a theory in a controlled laboratory-style experiment in the way a physicist or chemist can. Ironically, economists usually earn a lot more than physicists, and are called upon as the experts in almost everything. Economists don’t even need empirical validation of their theories.

Which leaves markets prone to irrational bursts of optimism and pessimism, as we have seen in the last month. January and February 2016 started off with dire predictions on oil, other commodities and China and the market fell heavily, and then in early March, it staged a strong rally as the banks and resource companies recovered some of their losses. Prices were higher despite no apparent improvement in underlying fundamentals. Morgan Stanley analyst Adam Parker advised clients:

“If the consensus is right that we will chop up and down, then by the time we feel a little better, we should take off risk, not add some. Maybe you should do the opposite of what you think you should do. That’s the new risk management.”

Do the opposite of what you think you should do

That’s the advice! Maybe it’s not as crazy as it sounds.

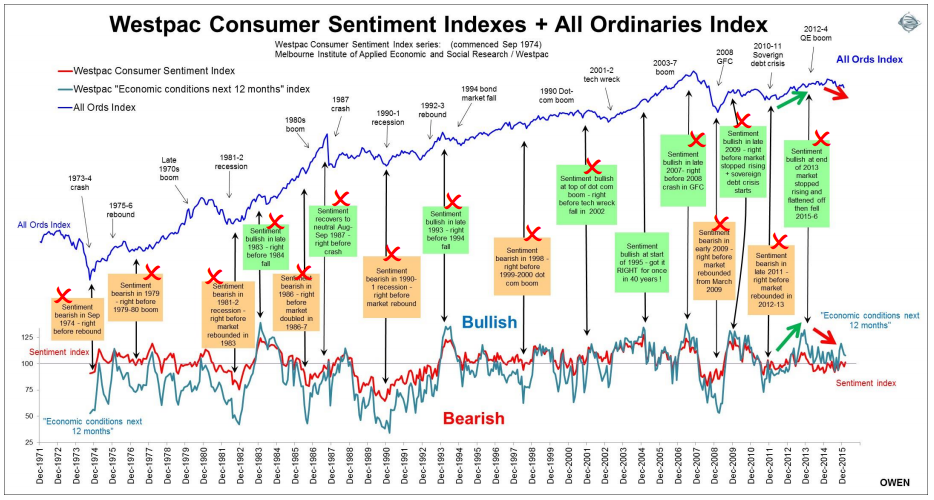

Consider the above chart, courtesy of Ashley Owen. It compares the Westpac Consumer Sentiment Index with the All Ordinaries Index. It shows that bearish sentiment (the blue line for economic conditions in the next 12 months) is usually followed a rising share market. Bullish consumer sentiment is followed by a falling market. It’s why people tend to buy high and sell low, and empirical evidence is that investors usually underperform the index by poorly timing the market.

Let’s leave the final words to Jack Bogle, Founder of the Vanguard Group:

“The idea that a bell rings to signal when investors should get into or out of the market is simply not credible. After nearly 50 years in the business, I do not know of anyone who has done it successfully and consistently.”

Good luck with that, Google

I can imagine the scientists and engineers doing what we all do to start a new project, and Googling about human behaviour as they attempt to model how bus drivers might behave. They could do worse than study a good book on behavioural finance.

Graham Hand is Editor of Cuffelinks and confesses his own SMSF has a growth/defensive allocation of about 50/50. If it’s good enough for a Nobel prize winner …