It’s always useful to study the asset allocation of Australia’s sovereign wealth fund, the Future Fund, as it takes an unusual approach to investing. Whereas most institutional superannuation funds hold at least 25% of their assets in Australian equities, the Future Fund’s allocation at 30 September 2017 included only 6% to Australian equities. The main categories where it is overweight versus the industry are private equity at 12% and alternative assets at 15%. Cash is a healthy 19%. That’s nearly half its $134 billion in assets in these three categories, two of which barely move the needle for most SMSFs.

The main reason for this structure is the desire to protect capital. Its investment mandate is to achieve CPI plus 4% to 5% “with an acceptable but not excessive level of risk”. In its investment beliefs, it shows why assets such as private equity and alternatives figure highly:

“Markets can be inefficient, albeit that the degree of inefficiency varies across markets and over time. Skillful management can add value after fees, and such added value can be uncorrelated to market returns over time and can therefore be highly beneficial to the total portfolio investment characteristics. Capturing skill-based returns requires an appropriately resourced and disciplined process.” (my bolding)

Their beliefs drive them towards long term, illiquid and uncorrelated assets to extract returns for risk.

Five insights from the 2017 Sohn Conference

The Future Fund’s Chief Investment Officer, Dr Raphael Arndt, spoke at the recent Sohn Hearts and Minds Investment Leaders Conference. He identified five megatrends changing the world of investing:

1. The end of the leverage tailwind means asset prices are not supported by as much debt, making price growth less sustainable.

2. Declining population growth will reduce economic growth, with the United Nations forecasting global population growth will fall from the current level of around 1.5% to 0.25% by the turn of the century.

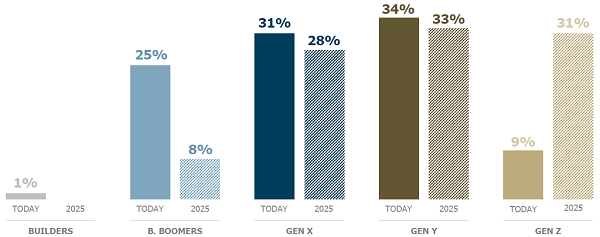

3. Changes in the workforce and consumer preferences mean the best future investments will differ from the past, because younger generations consume and work differently. He included this chart showing that by 2025, baby boomers will comprise only 8% of the Australian workforce, while both millennials (Gen Y) and Gen Z (roughly, those born after 2000) will each be about one-third.

Changes in the Australian workforce, today and 2025

Source: Future Fund, Mark McCrindle

4. Income inequality is increasing populism and populist policies, with many people in developed countries receiving little growth in wages in the last 20 years. The rich have become richer through asset price growth but populist policies will reduce economic growth.

5. Technology is changing how society interacts, with new platforms achieving adoption faster than at any time in history.

Investments can become worthless quickly in the face of disruption by new technologies or competitors, and the past should not be taken as a guide to the future. This is one reason why the Future Fund holds so much cash. He emphasised the Fund’s desire to find returns which are uncorrelated to the equity markets and companies adversely hit by these trends, which explains the alternatives (or hedge fund) allocation.

Over the last seven years, the 9.9% return delivered by the Future Fund comfortably exceeds the CPI+ target of 6.5%.

Graham Hand is Managing Editor of Cuffelinks.