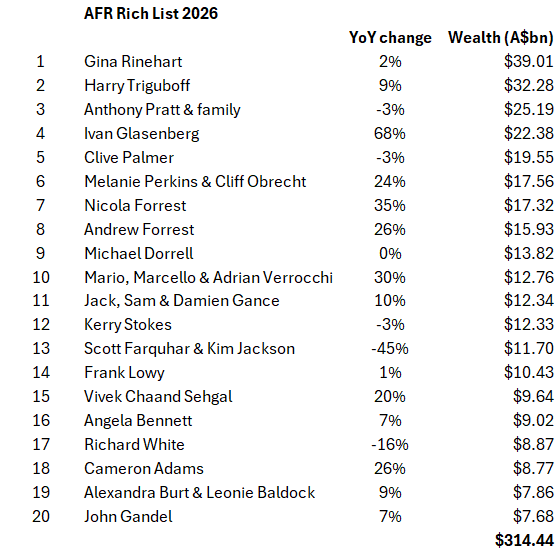

Australia’s billionaires increased their wealth by $25.7 billion over the past year such that the 20 richest Australians now boast more wealth than the poorest three million households, says Oxfam Australia.

Source: The Australian Financial Review

In the US, Federal Reserve data shows the richest 1% of Americans owned a record 31.9% of US wealth at the end of 2025. Plutocrats, the richest 0.00001%, possessed an all-time high 12%, while the poorest 50% owned just 2.5%. The trillion-dollar floats tied to artificial intelligence will send more wealth towards the rich amid talk AI will create an underclass of displaced workers.

Still in the US, labour’s share of economic output this year has plunged to 51%, the lowest since records began in 1947, while the profit share sits near a record high of 12.1%. That’s because real wages have only grown 3% since 2019, while profits have soared 50%.

These statistics are just some of many that hark to the widening gap between the haves and have-nots in most developed and developing countries due to how free-market economic reforms in recent decades created a winner-take-more society.

The rich and skilled thrived as governments took decisions that allowed capital to dominate labour just as new technology and the globalisation it enabled eroded the bargaining power of the semi-skilled and unskilled. The highest marginal income-tax rates were slashed while taxes aimed at the rich such as those on capital gains and inheritances were reduced or abolished. Fighting inflation took priority over reducing unemployment. A push to maximise shareholder value reigned, while organised labour was defanged through regulation and outsourcing. Government assets were sold, often cheaply, and turned into private monopolies. Low, even negative, interest rates and central-bank purchases boosted asset prices, especially stocks and housing. The other side of the surge in asset prices is that to keep up much of the public became indebted, especially to educate and house themselves.

This all took place, of course, as living standards rose. So what’s the problem? It’s this. Inequality comes with political and economic risks that threaten future wealth creation.

One political risk stems from the associated feeling that everyone is out for themselves. This impression undermines the social cohesion that lubricates economies and societies. As people become more selfish and insecure, corruption flourishes, crime jumps, anti-social behaviours increase, labour unrest stirs and legal disputes tied to commerce rise.

A second political risk tied to inequality is that resentment against economic injustice nurtures an environment ripe for demagogues promoting populist politics that are economically damaging – note how surveys show the young in advanced countries are leaning socialist. Democracies across the Western world including Australia are prone to a political backlash that undermines economic efficiency whether the populists be left- or right-wing.

A third political risk is the concentration of economic power can undermine democracy because it gives the mega rich too much political power. As the wealthy – or the ‘Epstein class’ as the unaccountable elite are now known in the US – use their financial muscle to expand their economic interests (via, for instance, subsidies or anti-competitive protections around their assets), the core political institutions of society erode. Rule of law and connected property rights, liberties such as free speech, open debate and fair elections are among protections vulnerable if society tilts towards ‘wealthtocracy’.

The extreme case with these political risks is that people eventually react when they feel they no longer live in a fair society or one where they or their children have opportunities. Inequality combined with economic hardship can thus lead to labour unrest and upheavals that topple governments and change political systems. Rarely does such turmoil lead to prosperity.

A fourth problem linked to inequality is that unequal societies prove to be faulty and inefficient economies. When too much income and wealth streams to the top, the middle and lower classes are incapable of marshalling the purchasing power needed to fan sustainable economic growth. The lack of aggregate demand tied to the perennial inequality of Latin America has retarded these countries economically as well as politically. Federal Reserve officials have lately warned the loss of demand due to widening inequality increases the risk of a US downturn.

Rising inequality can thus force indebted governments to run larger fiscal deficits to keep the economy running, perhaps to the point (like now) where public debt poses a menace for financial stability.

Another way inequality undermines economic growth is that people don’t work as hard if they feel they are not rewarded properly. Another is that inequality directs economic activity towards acquiring government-sanctioned monopolies rather than innovation.

Politicians often talk about tackling inequality. Solutions proffered involve higher taxes on the rich and capital gains and the closing of tax loopholes that favour the wealthy. Governments promise to spend more on education, health, welfare payments and public works, especially in poorer areas. But that costs money indebted governments don’t have. Another category of remedies is to raise minimum wages, tilt employment laws towards labour and tighten anti-competitive regulations. But the first two reduce competitiveness and fan inflation while the third is often window-dressing.

While the end of easy money could cool asset markets and decrease inequality, the indebted will struggle under higher interest rates and any rise in joblessness would devastate these households. Less regulation might allow smaller businesses to rise and challenge Big Business. But vested interests are skilled at pressuring governments to impede capitalism’s inherent creative destruction.

The challenge for policymakers is to overcome how no easy solutions loom to tackle the economic and political damage wrought by inequality. But something needs to be done.

It should be noted that some argue that inequality measures would be less alarming if factors such as homeownership, taxes, transfers, pension entitlements and the way people move through income brackets across their lives are taken into account. Perhaps. It’s true that the masses are better off these days on GDP-per-capita measures. But people because don’t feel better off because they aren’t relatively better off.

Sometimes it seems like the only way inequality will be diffused as a political rallying cry is a crisis that destroys wealth, similar to how wars and depressions reduced inequality in for most of the 20th century.

A more optimistic view, however, would be that well-designed policies that promote shared prosperity would help economies and liberal democracies thrive too.

Michael Collins is a freelance writer and editor, economist, and investment specialist. Republished with permission from the author’s Substack newsletter @denouementwatch.