Industrial has been Australian real estate’s star performer for a decade, notching up an annualised 10-year return of 14.2%1. While the rate of new supply has increased, the availability of space has been unable to match pace with surging demand. Australia has become the lowest vacancy industrial market in the world2, contributing to record rental growth of almost 25% in the year to March 20233. The sector’s strong momentum continues, and the outlook is bright, as several long-term tailwinds drive demand.

E-commerce

The shift in retail activity from physical stores to digital channels drives demand for industrial space in several ways:

- warehouse space is needed to store inventory which would have otherwise sat in a store;

- e-commerce tends to offer a wider range of products, rather than the curated selection that a specific retail store might be limited to, necessitating more storage space; and

- goods purchased online have higher rates of return, and space is needed to handle the reverse logistics.

Increased storage and space needs mean pure-play e-commerce requires three times the distribution space of traditional retail4. Customer preferences are primarily driving the shift to online, particularly as demographic change sees ‘digital natives’ become the dominant consumer segment. As scale and investment lead to greater efficiencies and profitability, the shift may gain another momentum boost.

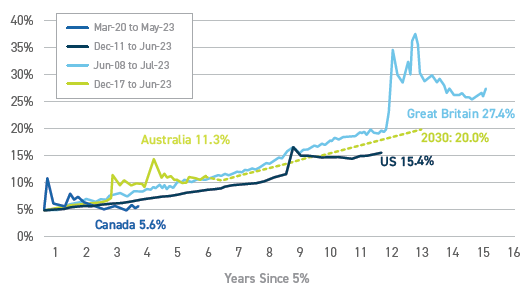

E-commerce in Australia is following a similar trajectory to Great Britain – it is on track to hit a market share of 20% of all retail sales by 2030 despite growth slowing from pandemic peaks. With 70,000sqm of logistics space needed for every incremental $1 billion of online sales5, e-commerce alone could generate industrial space demand of almost 600,000sqm p.a. over the next seven years6.

Figure 1: Online share of retail sales - based to 5% share

Source: ABS; ONS; StatCan; US Census Bureau; Cromwell.

Different country inclusions/exclusions for Food/Auto & Gas.

Supply chain resilience

One of the most immediate and lasting impacts of the pandemic has been supply chain disruption, with erratic swings in demand exacerbated by congested ports and border restrictions. The pendulum is now swinging from the prevailing ‘Just-In-Time’ supply chain philosophy, where goods are shipped on demand and arrive just before they are needed, back towards a ‘Just-In-Case’ approach. Under this approach, higher volumes of inventory and production are stored and undertaken locally, where it can be better guaranteed.

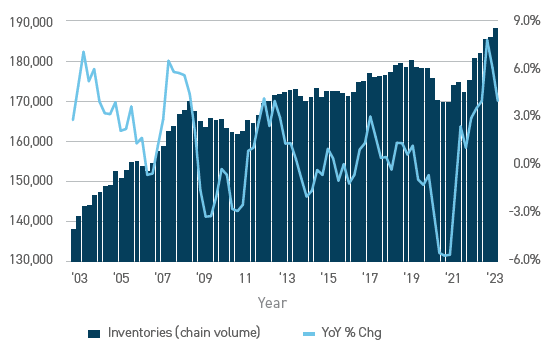

Supply chain experts estimate the majority of Australian occupiers are currently holding approximately 30% more inventory compared to pre-pandemic levels7. While this degree of buffer will likely decrease as supply chain disruptions ease, a full return to previous inventory levels is unlikely, meaning more warehouse space will be needed on an ongoing basis for storage.

Figure 2: More space is needed to store stock

Australian Inventory Levels

Source: ABS (Mar-23); Cromwell.

A 2022 BCI Global survey found over 60% of respondents are expecting to onshore or re-shore (i.e. localise) activity in the next three years8. The push to diversify production and improve supply chain resilience is being supported by the Government through the $15 billion National Reconstruction Fund. It should expand the manufacturing industry in Australia and increase demand for associated industrial real estate.

Infrastructure

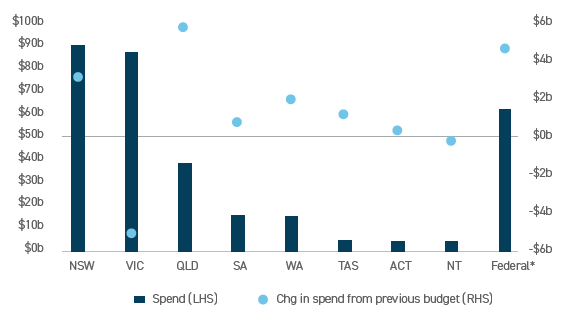

Infrastructure development is a key priority in Australia as we contend with ongoing urbanisation and densification, along with surging population growth. Across the 2022-23 Budgets, $255 billion in government expenditure was allocated to infrastructure for the four years to 2025-26, an increase of $7 billion or 2.7% compared to 2021-229. In dollar terms, NSW has the highest allocation to infrastructure ($88 billion), while QLD saw the largest increase on the previous year ($5.7 billion). The three East Coast states of NSW, Victoria, and QLD account for 83% of the committed infrastructure funding.

Figure 3: Budgeted infrastructure spend: 2023-26

Source: Infrastructure Partnerships Australia (Nov-22); Cromwell

*The Federal Government primarily funds state infrastructure projects

Infrastructure investment stimulates demand for industrial real estate in a couple of ways. As new infrastructure is built, congestion and connectivity improve, lowering transport and operating costs and allowing more efficient movement of people and goods. This helps businesses to grow and increases the supportable population base. More activity and more people, mean more demand for industrial space to power the ‘engine room’ of a bigger economy. The more direct source of infrastructure-related industrial demand occurs during a project’s construction phase, as space is needed to manufacture, assemble, and store materials and components.

Customer proximity

The time it takes to reach the customer is of critical importance in modern supply chains. Customers increasingly expect products to arrive faster, more flexibly, at the time promised, and with lower delivery costs. While not a driver of aggregate space demand, the focus on customer proximity does contribute to stronger rental growth for well-located properties.

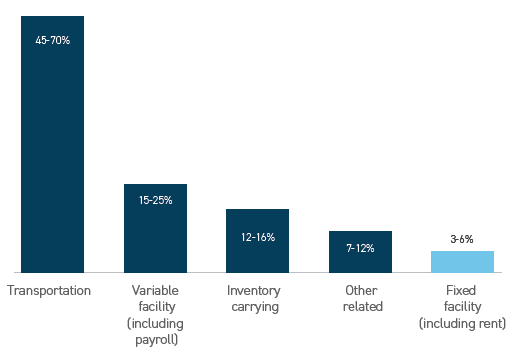

Transport accounts for 45-70% of logistics operator costs compared to 3-6% for rent10. This low proportion of cost means well-located industrial assets with good transport access and proximity to customers have long runways for rental growth, as occupiers prioritise lower (cheaper) transport times – an up to 8% increase in rent can be justified if a location reduces transport costs by just 1%.

Figure 4: Share of logistics costs

Source: 2022 Global Seaport Review, Dec-22 (CBRE Supply Chain Consulting)

But what about supply risk?

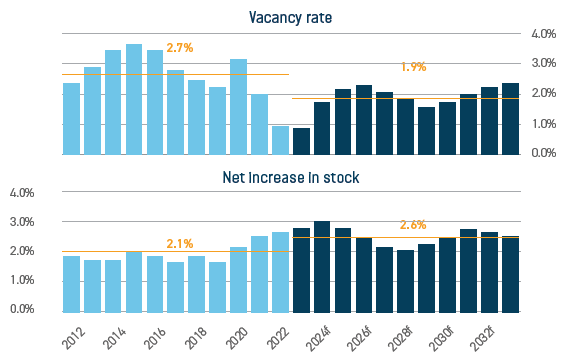

While the demand drivers for industrial are clear, the supply-side response is just as important in determining asset performance. In previous cycles, downturns have arisen from excess speculative development creating too much stock and dampening rental growth. But there are several reasons why the sector is insulated from a supply bubble this time around. Firstly, labour and materials shortages are making it challenging to physically build new assets, even though development is commercially attractive. Secondly, there is a lack of appropriately zoned, serviced land available for development. While land is becoming available farther out from metropolitan centres (e.g. Western Sydney Aerotropolis), this land is not appropriate for many occupiers or uses which require closer proximity to customers. It will also take time for this land to become development-ready, due to planning, infrastructure (e.g. road widening), and utility servicing (e.g. water connection) delays. Finally, the sector has matured and become more ‘institutional’ over the current cycle, with a shift in ownership from private capital to large, sophisticated owners and managers. Institutional owners take a more cautious approach to development, contingent on higher levels of tenant pre-commitment, reducing the risk of a speculative supply bubble. These factors will make it difficult for supply to keep pace with – let alone surpass – demand.

Figure 5: Vacancy rate forecast to remain below pre-COVID average despite higher supply

Indicative East Coast Industrial, Buildings >5,000sqm (YE Jun)

Source: Oxford Economics Limited (Feb, May & Jun-23); Cromwell

Demand story remains intact

Industrial has been the “hot” sector in recent years, and it’s reasonable to question whether it’s been squeezed of all its juice. The pandemic provided a boost to many of industrial’s demand drivers (e.g. e-commerce) and introduced new ones (e.g. supply chain resilience). While these tailwinds have abated somewhat from their pandemic highs, they continue to contribute to a positive demand outlook. Arguably more importantly, the supply response remains constrained by shortages (e.g. labour/materials/land) and delays (e.g. planning), and it will take several years for the sector to return to a more normal supply-demand balance. As a result, Cromwell expects healthy rental growth to be a key driver of industrial returns, and for the sector to remain attractive despite expansionary pressure on cap rates.

1. The Property Council-MSCI Australian All Property Digest, June 2023 (MSCI)

2. Australia’s Industrial and Logistics Vacancy 2H22, December 2022 (CBRE Research)

3. Logistics & Industrial Market Overview – Q1 2023, May 2023 (JLL Research)

4. What Do Recent E-commerce Trends Mean for Industrial Real Estate?, Mar-22 (Cushman & Wakefield Research)

5. Australia’s E-Commerce Trend and Trajectory, September 2022 (CBRE Research)

6. Projection based on historical 15-year retail sales growth of 4.0% p.a. (Cromwell, Jun-23)

7. Is ‘Just-in-Time’ a relic of a time gone by in Australia?, March 2023 (JLL)

8. Global Reshoring & Footprint Strategy, February 2022 (BCI Global)

9. Australian Infrastructure Budget Monitor 2022-23, November 2022 (Infrastructure Partnerships Australia)

10. 2022 Global Seaport Review, December 2022 (CBRE Supply Chain Consulting)

Colin Mackay is a Research and Investment Strategy Manager for Cromwell Property Group. Cromwell Funds Management is a sponsor of Firstlinks. This article is not intended to provide investment or financial advice or to act as any sort of offer or disclosure document. It has been prepared without taking into account any investor’s objectives, financial situation or needs. Any potential investor should make their own independent enquiries, and talk to their professional advisers, before making investment decisions.

For more articles and papers from Cromwell, please click here.