Every week, investors ask some version of the same question: Are we in a bubble?

It's a reasonable question. Stock markets have been at elevated valuations. Geopolitical tension is real. Interest rates remain high by recent historical standards. There's plenty to feel nervous about.

But that question – is there a stock market bubble? – may be the wrong one to ask.

The more important question is this: Is there an earnings bubble?

That distinction matters more than almost anything else right now, because the data tells a story that runs counter to most of the market commentary you’ll hear.

Company earnings aren’t just holding up – they’re accelerating. And in many sectors, earnings growth has actually been outpacing price growth. That’s not what you’d expect from a market in irrational bubble territory. Here’s what the numbers are telling us, and what it means for how you should be thinking about your investments.

The earnings story most investors are missing

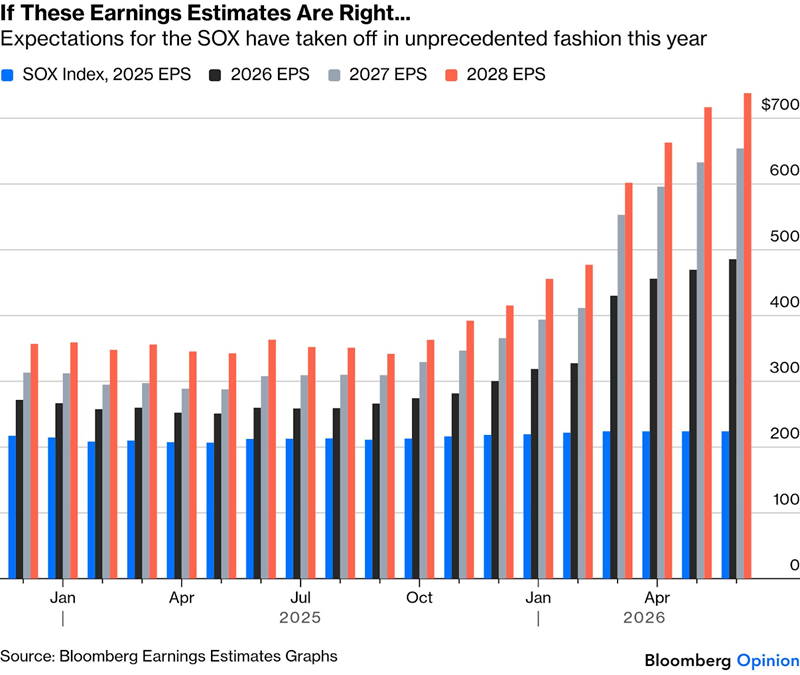

Over the past couple of years, something unusual has happened. Global earnings have risen sharply, with forward earnings growth estimates now sitting at close to 25% for 2026 and nearly 18% for 2027. To put that in context: these are not slow, steady gains. This is an earnings acceleration that exceeds what we saw following both the financial crisis and the COVID-era recovery.

What’s driving it? Look at what’s happening across sectors:

- Technology forecasts have been upgraded by 30%+ this year alone.

- Communication services have seen earnings upgrades of 20% or more.

- Energy has seen even larger moves - but for different, more complicated reasons.

- Crucially, earnings upgrades are now broadening across sectors - not just confined to a handful of mega-cap tech names.

And here’s the thing that should make long-term investors sit up: in most of these sectors, the forward price-to-earnings ratio has actually declined. In other words, stocks have gotten cheaper relative to their earnings – even as prices have risen in absolute terms.

That’s not how a speculative bubble typically behaves.

Why the tech sector warrants a closer look

None of this means everything is straightforward.

Technology – and particularly semiconductors – demands careful scrutiny.

The semiconductor industry is notoriously cyclical. Companies like Micron have, at various points in past cycles, traded at just three or four times earnings at peak – precisely because investors knew a supply glut was around the corner. When new factories come online, supply swamps demand, prices collapse, and earnings follow.

That same dynamic is playing out today, in slow motion. TSMC has flagged roughly a 40% increase in capital expenditure. Samsung is spending 70–80 billion dollars on capex and R&D. SK Hynix and Micron have similar timelines. The supply is coming.

But – and this is the crucial point – most of that new capacity isn’t coming online until 2027 or 2028. Which means the supply constraints that are driving extraordinary semiconductor earnings right now are likely to persist for at least the next 12 to 18 months, possibly longer.

The memory sector alone is a striking illustration: revenues were roughly $200 billion in 2025, are forecast at $600 billion in 2026, and projected to approach $800 billion in 2027. Much of the 2026 number is already contracted. This isn’t speculation – it’s supply chain reality.

That said, long-term analyst forecasts are starting to look crazy. No sector sustains that pace forever.

Analyst forecasts at cycle peaks tend to reflect euphoria, not fundamentals. When the cycle turns, the revision will be sharp.

Some stocks, NVIDIA, for example, have an argument for a sustained period of higher margins due to a mix of technological leadership and growing AI demand. For most of the sector, though, that argument does not stack up. There is enough competition and technological parity among the leading stocks that margins will eventually return to trend. It is just a question of when the supply arrives.

The multiplier effect: Why this is bigger than just tech

Here’s where the narrative gets more interesting.

For most of the past several years, major tech companies – think Google, Meta, Microsoft – were sitting on vast cash reserves. They were generating enormous profits but not deploying them into the real economy. Share buybacks, debt reduction, cash accumulation.

Economically, that’s a drag: money being pulled out of productive circulation.

That’s now changing, rapidly.

These same companies are raising capital, taking on debt, and spending heavily on data centres – infrastructure that represents more than 2% of US GDP in new capital expenditure. And capital expenditure has multiplier effects. The data centre needs electricians, construction workers, logistics, and materials. Those workers spend their wages. Those wages flow through local economies. Other sectors are beginning to see the benefits.

This is what’s driving the earnings broadening we’re now observing. The consumer sector remains under pressure – household budgets are squeezed by higher prices and interest rates. But company earnings across a broader range of sectors are growing, because AI infrastructure spend is flowing outward into the wider economy.

The result is a curious disconnect: a consumer sector that’s struggling, alongside corporate earnings that are accelerating. Both can be simultaneously true when capex-driven multiplier effects are at work.

Now the multiplier will one day go into reverse – but for now the effects are positive.

Three things that could derail this

Being invested in a rising earnings environment makes sense. But “the earnings are strong right now” is not the same as “nothing can go wrong.”

There are three macro risks that deserve close monitoring:

1. Inflation and interest rates

If inflation re-accelerates – driven by supply chain pressures, wage growth, or fiscal stimulus – central banks will respond. Higher rates compress consumer spending and increase borrowing costs for the very companies now spending heavily on infrastructure. This is the most obvious risk.

2. Oil prices

The energy sector’s earnings surge looks impressive on a chart, but rising oil is a cost for nearly every other sector and every consumer. If geopolitical tensions in the Middle East escalate and oil approaches $200 a barrel, that’s not a sign of economic health – it’s a warning of potential recession and demand destruction.

3. The earnings cycle turning

The most important risk is internal to the market itself. Right now, markets are pricing in strong earnings growth – and getting it. But the valuation math is unforgiving when the cycle turns.

Here’s a simple illustration: if earnings growth this year comes in at 25% as expected, but next year’s growth slows from an expected 18% down to 8%, you face a double compression. Earnings expectations fall by 10%. And investors, no longer willing to pay a premium multiple for high growth, reprice the market down. You can easily construct a scenario where that combination produces a 20% drawdown –10% from earnings downgrades and 10% from valuation compression.

The good news? We’re not seeing signs of that turn yet. The earnings growth looks durable for now. But it bears watching carefully.

What this means for you as an investor

There’s a clear takeaway here, and it runs counter to the instinct to “wait for a pullback” or stay on the sidelines while markets feel elevated.

When earnings are growing at the 99th percentile of historical rates, it’s reasonable – arguably rational – to accept valuations at the 80th percentile. You’re paying a premium for genuinely exceptional growth. That’s not a bubble; that’s a defensible price for real earnings power.

The risk is not that prices are high today. The risk is being slow to identify when earnings begin to roll over – and being caught holding high-multiple stocks at precisely the moment the growth justification disappears.

That’s why the focus needs to be less on price levels and more on earnings sustainability. Watch the data. Watch semiconductor capex timelines. Watch whether the broadening of earnings beyond tech continues. Watch oil and rates.

The investors who will do best through this period are not those who predicted a correction at every high, but those who stayed invested through strong earnings periods and had a clear, evidence-based framework for when to reduce risk.

The bottom line

Stop asking whether there’s a stock market bubble. Start asking whether there’s an earnings bubble.

Right now, the honest answer is: not obviously. Earnings are strong, growing, and broadening. Valuations, while elevated in absolute terms, are not extreme relative to those earnings. Supply constraints in semiconductors will persist for 12 to 24 months. AI capex is generating real multiplier effects across the economy.

There are warning signs – particularly in analyst euphoria around long-term tech growth projections and the cyclical risks in semiconductors. But the near-term picture is more solid than the bear case would suggest.

Damien Klassen is the Chief Investment Officer at Nucleus Wealth. This article is general information and does not consider the circumstances of any investor.