The view (strongly expressed in the AFR Superannuation Lending Roundtable for example) that super funds should do more long-term lending has much merit, despite bank objections. There is, in fact, a fundamental mismatch in terms of the channels by which household savings flow to those wanting finance for investments in real assets.

The Australian financial system has still not caught up with the realignment of household savings into long-term investments brought about by the growth of superannuation.

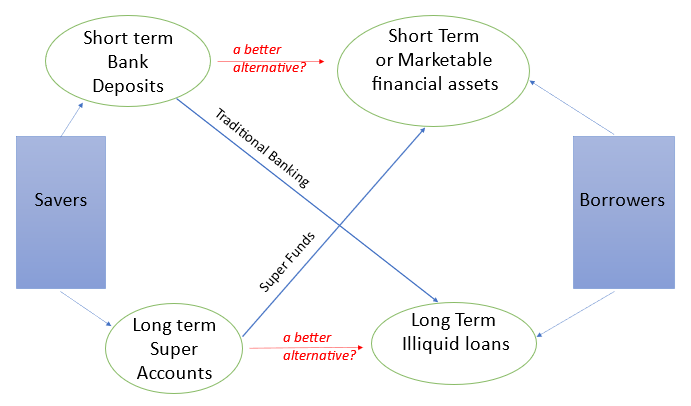

A fundamental mismatch

Essentially, and at only minor risk of over-simplification, the mismatch is as follows. Banks provide liquid (short-term) facilities for savers but tend to make longer-term loans.

Super funds provide long-term saving facilities, but tend to invest primarily in liquid and marketable investments, such as equities and debt securities tradeable in markets. The figure illustrates this mismatch.

Bank profits benefit from investing in longer-term loans because of the liquidity premium built into the expected return on such loans, but they need to hold some liquid assets to manage the resulting liquidity risk mismatch. Super funds, by investing predominantly in marketable (liquid) securities rather than longer term less-liquid loans, forgo the available liquidity premium to a cost to their members.

It makes sense to have long-term savings directed more to financing long-term investments and short-term savings (which involve liquidity risk for the institutions accepting them) invested in shorter-term investments. Otherwise, the growing stock of long-term savings needs to be diverted to banks for their credit creation via super funds on-lending to banks, involving, at least, a cost of double-handling.

Traditional roles

Of course, there is more to it than just a realignment of investment patterns. Banks are generally seen as creators of new financial assets in the form of loans (or facilitating companies to access debt and equity markets) and use their expertise in credit risk assessment to do this (hopefully) well. Super funds are traditionally seen as investors in already existing assets (such as securities traded on financial exchanges).

Yes, eventually the investments made by super funds will provide the ultimate funding of securities created by banks (bonds, securitisations, equities, etc.). But might it be better to have the ultimate funding aligned with the initial funding via the super funds being the creators of new financial assets?

More generally, with the growth of illiquid (super) savings, is there as much need for the risky liquidity creation traditionally undertaken by banks and the high liquidity premium cost built into longer-term funding?

The banks will argue that credit risk assessment and management of illiquid loans is a skilled task, involving expertise which super funds do not currently have. That may be so, but three counter-arguments are relevant.

First, individuals with, and systems providing, credit risk expertise and capabilities, are transferable resources which can be ‘poached’ or purchased.

Second, it would be possible for super funds to outsource the credit risk task to a trusted third party who has sufficient ‘skin in the game’ to ensure their objectives are aligned with the super fund.

Third, the explosion in data availability due to the digital revolution (and open banking) is reducing the value of the traditional customer relationship role in credit risk assessment.

The banks also have a strong self-interest rationale for their stance. More competition in long-term lending can be expected to impact adversely on bank profits. And if they are undertaking less liquidity creation and holding more short-term assets, profits will be affected by less liquidity premium rewards.

Of course, super funds have already moved into the creation of new long-term financial assets, through such investments as funding new infrastructure projects. But there is scope for more long-term financial asset creation from a lending role.

There are clearly risks involved which warrant attention. There is also the problem of valuing illiquid assets and the potential for mis-valuation of non-traded assets to adversely affect the ability of APRA to identify underperforming funds. But discussion of a lending role for super funds is warranted.

Kevin Davis is Emeritus Professor of Finance at The University of Melbourne. Kevin’s free e-text reference book 'Bank and Financial Institution Management in Australia' is available on his website. Kevin was also a member of the Financial Systems Inquiry ('The Murray Report') in 2014.