"I've been doing this as some kind of Chief Investment Officer since 1978. And this is about the wildest cocktail I've ever seen in terms of trying to figure out a roadmap.”

Stanley Druckenmiller, Duquesne Family Office, speaking on Goldman Sachs’ Talks at GS, 4 February 2021.

Any investor hoping to find a fund manager who outperforms in all market conditions will be sorely disappointed. It's an elusive goal. At the moment, there’s a great divide between those who believe investing conditions are excellent and those who see risks everywhere. Time will tell whether funds which outperformed in recent years continue to do so, but signs are the tide is turning.

Fund managers have different perspectives

Experienced investors with decades in the market are currently the most cautious. World-famous names such as Howard Marks, Charlie Munger, Jeremy Grantham and Stanley Druckenmiller see bubbles everywhere. Locally, luminaries such as Hamish Douglass, Anton Tagliaferro and Andrew Clifford issue warnings. On the other hand, some lesser-known fund managers such as Thomas Rice of Perpetual, Alex Pollak of Loftus Peak and Joe Magyer of Lakehouse see disruption and tech as great opportunities, and their funds performed well in 2020.

One reason for the divide is the type of investing they believe in. One side would never invest in Tesla or Afterpay or Zoom at high multiples of revenue, often without profits, and the other side who would never invest in traditional industrials such as financials and energy (fossil fuels) because they are old world stories.

It’s a variation on ‘growth versus value’. It's not a clear distinction, but 'growth' stocks hope to grow faster than the economy due to some special factor, such as tech or healthcare, while 'value' stocks are trading below what they are worth and are expected to grow in line with the economy, such as consumer goods and financials.

It's been a fascinating divide in the last few decades, as shown in the chart below. Between 1975 and 2008, the market in which our most experienced fund managers cut their teeth, value strongly outperformed growth. In the last dozen years, especially driven by the rise in tech stocks, growth has killed value, and with it, the relative performance of many long-term managers. But in the six months to end February 2021, value achieved a strong 8% reversal.

MSCI World Value Index relative to MSCI World Growth Index

Source: Van Eck using Bloomberg data

Where should an investor put their money?

Investing is more art than science, and the answer lies in what an investor wants from their fund manager. Do you jump on the growth bandwagon believing the momentum until the end of 2020 will return, or back the expertise of fund managers with long-term records in more traditional stocks?

Morningstar global research shows that of the hundreds of funds that have outperformed their benchmark by more than 1% annualised over 10 years, 100% of them underperformed the benchmark in a 12-month period. Investors who jump from fund manager to fund manager risk always backing the wrong horse.

It's the same as selecting hot cross buns

Let’s step away from the desk and into the kitchen and find some experts to help select hot cross buns.

Heading into Easter and being rather fond of fruit bread and hot cross buns, I checked the Choice website for their favourites. You’d be struggling to find a better panel of judges than the three experts rating a selection of buns. There was Christopher Thé, who after training in fine dining restaurants including Bel Mondo, Claude's and Quay, opened his own boutique patisserie, Black Star Pastry, in Newtown. He’s worked on tasting panels for Gourmet Traveller and Good Food. Then there’s Brigid Treloar, a food consultant for over 30 years, author of eight cookbooks and a judge in the Sydney Royal Fine Food Show Bakery Competition. Plus Ian Huntley, a pastry chef for 35 years, who after working in Sydney's InterContinental and Regent Hotels started his wholesale patisserie business. He is Chief Assessor for patisserie at Le Cordon Bleu.

Surely, in seeking guidance, this is an incredibly well-credentialed trio. These are not Instagrammers or Facebookers or Influencers who jumped on the web during COVID.

I’ll spare you the full details of the Choice review, but here is the winner.

Coles Traditional Fruit Hot Cross Buns

- Choice Expert Rating: 80%

- Price: $0.58 per bun ($3.50 per 6-pack)

- Made from at least 95% Australian ingredients, the highest percentage of local ingredients of all products on test. At 27%, these buns also contain the most fruit.

- Experts say: "Even cross, good colour, shiny! Bouncy texture. Quite a lot of fruit. Great balanced mouth feel and flavour. A nice hot cross bun despite its slightly odd shape."

So I dutifully headed down to Coles and bought the best. At the first bite, I thought ‘fake food’. Too sweet, little texture. The judges seem to like a bouncy ‘mouth feel’, but I want firmness. Give me a bit of substance to the bite, and who cares about ‘slightly odd shape’.

One hundred years of combined culinary expertise and that’s the best they can do.

A few days later, The Sydney Morning Herald of 23 March 2021 posted its own bun review. Rating for the exact same Coles buns? A measly 2/5, as the SMH said, “… a bland aftertaste. Needs more spice.”

Wait a minute. Aren’t they all experts?

It’s the same with fund managers. What suits me might not suit you, regardless of the level of expertise.

What do you want in a fund manager?

Let’s examine what might appeal in a fund manager by checking the recent results of one of the best-known stock pickers in Australia, Anton Tagliaferro.

Anton has been around for decades. At the risk of torturing the analogy, if you’re wondering whether he is capable of ‘hot and cross’, well, I sat in front of him at the Australia versus Japan game in Kaiserslautern, Germany, at the football World Cup in 2006. In the 26th minute, a Japanese player barged into Australian goalkeeper, Mark Schwarzer, and the ball drifted into the net. It was a clear foul and Anton let the referee know. I learned a few new words that day, especially since Australia did not equalise until the 84th minute (Tim Cahill scored the country’s first ever World Cup Final goal). By that time, Anton was well and truly hot and cross.

What do Morningstar’s analysts think of Anton’s Investors Mutual? Of the 78 Australian equity funds rated by Morningstar, only 14 receive a gold rating, including Investors Mutual, with this comment from analyst, Edward Huynh:

“Investors Mutual Australian Share’s shrewd investors and a class-leading process make this strategy one of our favourites in the value space. IML was founded by Anton Tagliaferro in 1998, and IML has maintained the same value quality approach to a fault.

One of the hallmarks of the strategy is strong downside protection. This came to the fore during the recent coronavirus sell-off as IML’s strategies achieved the lowest decline amongst the category. However, IML missed out on the violent rebound as low-quality names and high-flying tech stocks outperformed, which IML typically avoids. We’re confident that when value returns to favour, IML Australian Share’s talented investors and rigorous process are best positioned to capture the value premium, making this one of our favourites.”

IML gives downside protection but its process doesn’t participate in the expensive growth winners such as in the tech sector.

It's a bit like a firm hot cross bun without the exciting extras, and not a fluffy one that blows with the wind.

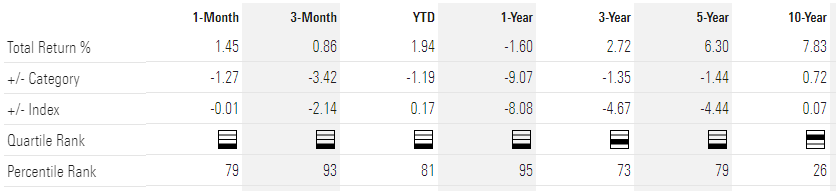

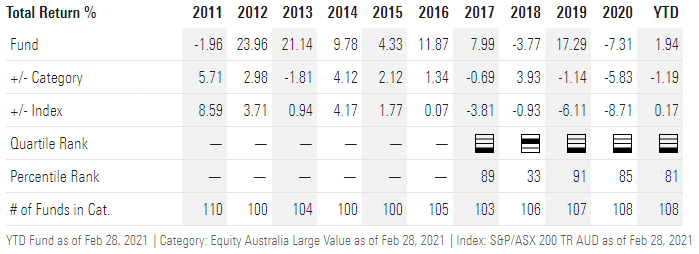

A look at its short-term performance is not encouraging. According to Morningstar, as shown below, over one year it is 8% under the index and beaten by 95% of the funds in its category. Even over 10 years, it is flat with the index. Yet Morningstar rates it gold and a top pick.

A breakdown of performance into calendar years shows a strong run from 2011 to 2016, outperforming the index every year and by 8.59% in one year.

Here is Edward Huynh again:

“The value tilt and mistrust of speculative stocks caused underperformance during the resources-led bull run from 2003-07. IML outperformed substantially in the 2007-08 turbulence. However, the strategy gave back that outperformance during the junk rally in 2009. The strategy performed strongly from 2010 to 2013 as sustainable income producers led the market. In 2014 and 2015, the strategy dodged plummeting mining and energy names ... The year 2016 was solid despite a resources resurgence, finding winners in CSL, Steadfast, AGL, and IAG. In 2017, IML struggled as growth and momentum stocks rallied. Underperformance was attributable to zero or underweight positions - such as ANZ and Rio Tinto - rather than picking losers ... Performance for 2020 has been mixed with class-leading downside protection during the Covid-19 sell-off; however, the lack of tech and resource holdings hurt the strategy on the rebound.”

How an investor feels about IML depends if they understood what they were buying and prefer Anton to stick to his process. On one level, he is well under the index for five years, so what is an investor paying for? On the other, he’s better at protecting the downside and will probably do well in the 'value rotation'. It's the future that matters in investing, and the market may be moving steadily towards traditional industrial stocks over resources and technology. Since inception in 1998, the Australian Share Fund is well ahead of the index.

IML might not use the words ‘hot and cross’ to describe the current market, but similar words such as 'outrageous' and 'ridiculous' can be found in its February 2021 report:

“This is why it remains so important to maintain perspective and to not get caught up in hype, and to not subscribe to theories about a so-called ‘new era’ touted to justify outrageous increases in share prices and the many ridiculous valuations that we are witnessing today.”

More recently in the global sphere, another gold-rated fund has experienced a few difficult months. We published the full transcript and webinar explanation from Magellan’s Hamish Douglass a few weeks ago. My colleague at Morningstar, Emma Rapaport, wrote an article on 24 February 2021 called ‘Will Magellan Global Fund’s underperformance persist?’. Wrote Emma:

“The gold-rated Magellan Global Open Class fund had its worst year in a decade in 2020, delivering investors a negative return (-0.2%) and underperforming both the Morningstar World Large Blend category (5.69%) and the MSCI World Ex Australia NR AUD index (5.73%) ...

Morningstar fund analyst Chris Tate says Magellan's returns were hampered by three key decisions lead portfolio manager and Warren Buffett-disciple Hamish Douglass took during the year: a big bet on Chinese e-commerce giant's Alibaba; energy sector exposure; and a dash for cash in the March-downturn. Tate says uncertainty remains over Magellan's short-term performance. "They'll do well if volatility returns to the market; if it keeps going up in a straight line they could lag." However, he hesitates to describe their position as bearish, pointing out that the strategy continues to hold a host of quality growth names.

(Links including to the full article are available to Morningstar Premium subscribers).

The hot, happy (not cross) funds

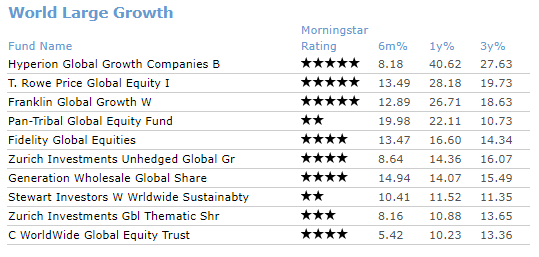

Some fund managers have bought into the world of disruption and have delivered excellent results, especially in global markets with better tech opportunities. A check of the Morningstar database of World Large Growth shows the following leading the pack on 12-month performance.

How did Hyperion generate a 41% return in a year? Says Morningstar’s Christopher Franz:

“Hyperion’s concentrated portfolio hosts some punchy bets. Technology and consumer discretionary names have long been well-represented, and alongside communication services stocks, accounted for around 80% of assets as at 31 March 2020. Hyperion believe they have an edge identifying companies in these sectors, as many stocks maintain strong competitive advantages and high returns on equity. High-conviction holdings here include Amazon.com and Microsoft, both of which eclipsed 10% of assets, slightly below the fund’s 13% cap on any single stock. They’ve also gravitated towards payment companies and nonbank financials, like Visa, Mastercard, and PayPal, companies they believe are taking advantage of the shift from cash to electronic payments. The portfolio also holds several luxury goods brands like LVMH and Hermes, which they believe to be at the pinnacle of brand equity and pricing power.”

Where do we find a high tech hot cross bun and fund?

Maybe Choice magazine and its experts were looking in the wrong place at the traditional high street retailers. Let’s turn to the online, trendier publication, Broadsheet, for its own take on the best hot cross buns (HCB). Some of these buns cost $5 each versus 60 cents for Coles Traditional, but do you get what you pay for?

“From a frankincense-glazed beauty by a cult bakery to a gluten-free bun that’ll impress those with gluten intolerances and the gluten-loving alike and myriad varieties (including choc-chip, apple-cinnamon crumble and classic fruit), there’s loads to love in the HCB realm this year.”

These are the private equity funds of the HCB world. High cost with potential high returns. For a special treat to give some upside, maybe a couple of buns with “a special spice blend, Earl Grey-macerated fruit and house-made candied orange” or “organic sultanas, candied peel and loaded with spice” or “cranberries, raisins and candied orange peel” will spice up a portfolio.

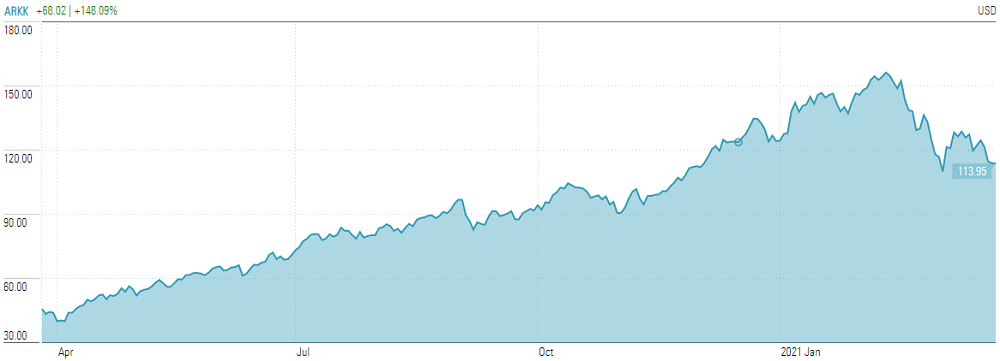

The ultimate HCB fund of the last year was Cathie Wood’s NYSE-listed Ark Innovation ETF (ARKK). Wood and her colleagues look for companies that benefit from disruptive innovation, posting a total return of more than 150% in 2020 and raising about US$10 billion in net inflows for the year (and US$1 billion on each of 9 February and 11 February). It is the fastest-growing fund in the US, holding only US$3 billion a year ago versus over US$20 billion in March 2021.

But then … as shown below, the main fund dropped 30% from almost US$160 to US$111 in February and March 2021, including over 6% on one day. It’s a portfolio full of future promise and low current-day earnings, with the median price/sales ratio for ARKK's companies at 22 versus 2.5 for the overall stock market. Only one third of its investee companies are currently profitable (as at early March 2021).

If this is what you want from your ‘frankincense-glazed, organic sultana, home-made candied peel’ fund, then there’s a place in a portfolio. But there's only room for a small allocation in the retirement portfolio of someone protecting capital.

What other types of funds might be hot and cross?

In a market where a stock can go from $8 to $150 in a year (Afterpay), or the top-performing large cap stock in the world, Sea Limited, which listed in the US in 2018 and rose 395% in 2020, managers who short stocks face risks way beyond their normal models. The most a stock can fall is 100% but it can rise, in theory, to any level. And we all know what happened with GameStop (up from US$40 to US$480), backed by an army of Reddits and Robinhooders who don’t care about value. They expect that someone else will pay more next week.

Shorting has not only become more dangerous, but in a world where poor quality companies without earnings can rally strongly, even a ‘correct’ analysis can blow up a fund. Many hedge funds, or long-short funds, have decided to either close their shorts or manage risk by shorting the index rather than a single stock. Australia’s best-known hedge fund, Bronte Capital, is down around 20% this financial year.

Another high-profile long-short manager forced to reassess its process is VGI Capital, which advised investors in a letter of January 2021:

“This environment has conversely driven an acceleration in the creative destruction of business models. Short selling in recent market conditions has been arduous as the market has been both far less discerning of questionable accounting and more willing to look through short-term business performance, even if it may be a strong indicator of long-term issues.”

Hedge funds expect there will come a time when market conditions favour shorting, as historically, the most-shorted stocks have performed poorly and the market should punish companies with a weak business. For the moment, the dough is left to prove.

Another manager underperforming in recent years is Platinum Asset Management, which until Magellan came on the scene, dominated retail flows into global equities. It was positioned away from the US where much of the global success due to the FAANGS is located. Writing on 11 March 2021, Morningstar analyst Adam Fleck said:

“While its strategies have outperformed over the long term, in the last five years, they have generally underperformed their benchmarks ... Most of the asset manager’s strategies outperformed over the year to January 2021, supported by recent stock price appreciation of cyclical and deep value stocks following promising vaccinations news ... the market is already pricing in the likely benefit of prospective outperformance, that being an immediate resumption of new inflows”.

And there we have a prime example of the problems fund managers face. Despite its good long-term results, Platinum has been unable to generate inflows in recent years, as investors wait until after a good run before investing, backing last year’s winners.

Co-Chief Investment Officer at Platinum, Andrew Clifford, spoke at an investor presentation on 30 March 2021, saying:

“The speculative mania in growth stocks will end badly for those who stay too long, just as it did in the tech bubble and countless other speculative manias. When you hear people say, ‘It’s not like the 2000 tech bubble’, I must say, I agree. This is a much bigger bubble.”

Should you invest in hot, cross funds?

Over time, active fund managers need to justify their fees, but cycles will work both for and against them. Any investor deciding on active over passive should consider it a 10-year decision. Otherwise, they are likely to redeem just before the fund manager becomes hot and happy.

However, fund managers also need to consider that disruption is permanent, and some companies are expensive for a reason – they have outstanding long-term prospects. Disruption is accelerating, and trends in biotech, AI, automation, robotics, cyber and a massive range of new technologies will continue to flourish. There is a place in every portfolio for added spice.

Similarly, hot tech funds need to recognise when the market reaches ridiculous levels, pricing to the moon stocks with little permanent competitive advantage and ongoing losses, such as Uber. There is a time for a reality check.

Either way, enjoy Easter

Whether buns or funds, the most expensive are not necessarily better. It’s subjective and personal, but I reckon it's worth including a couple of the $5 HCBs from a boutique bakery, even if you also like the 60 cent basic from Coles. You can fill the rest of your supermarket trolley (and your portfolio) with home brands (index funds) to save money, or if there is a name brand (an active fund) worth paying for, back the one you have always relied on.

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances or dietary requirements of any investor or HCB-lover.