Australia not long ago was a world-beater on global stock markets. Now it’s lagging other nations, with even once steadfast names on the slide. Meanwhile, the US economy and markets look attractive and dynamic. Is it time to revisit your global equity allocation?

This is a question many investors have been asking as sentiment around the Australian market sours. Faltering local share prices, rising interest rates, and bitter policy debates about tax now prompt thoughts of reweighting away from Australia.

It’s a contrast to the ‘miracle economy’ days of two decades ago after China’s entry to the World Trade Organisation set off a resource boom that fired up local stocks and made this country one of the few to avoid a recession after the GFC.

Now there are worries that the twin forces that buttressed Australia during those years – its resource sector plugged into China and its banks leveraged to a relentless housing boom – are leaving it sidelined in a world in transformation.

As we approached the end of the 2026 financial year, the Australian equity market was badly lagging, up 7% in 12 months to the end of May, compared with gains of close to 30% in the US. Global developed markets as represented by the MSCI World ex Australia index were up 14% unhedged and 27% hedged over the same period. The technology-heavy NASDAQ index was up over 40%.

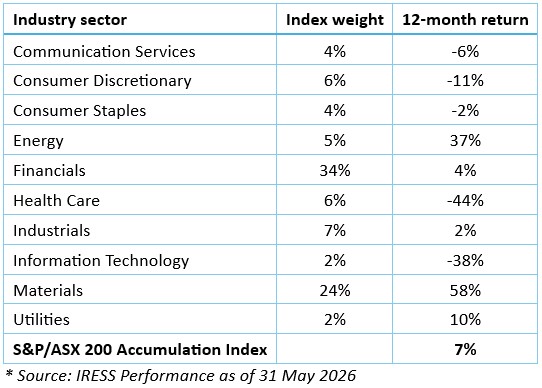

Cornerstone stocks like Cochlear (-62%), CSL (-60%), and Brambles (-27%) took a shellacking for the 12 months to the end of May. Even CBA was down 3.5%.

But for the performance of the miners and energy stocks (as the industry sector performance table below demonstrates), the picture would be even worse.

Added to market underperformance is gloom about prospects for the Australian economy. The RBA has raised interest rates three times already this year, citing a material pick-up in inflation and heightened uncertainty about the domestic outlook.

Increasingly, there is envy about the US market, which has been outperforming the world for years thanks to the dominance of a handful of high-growth tech companies, the AI boom, an entrepreneurial culture and a favourable low-tax environment.

Against that background, some clients are asking whether it is time to revisit their Australia versus global allocation.

A case for home bias

While debates can be had about certain issues at a policy or political level, investors should not allow ‘recency bias’ (a tendency to give undue weight to recent events or performance that dominate headlines) to overly influence a decision to reweight away from Australia. Reactive decisions usually result in errors of judgement.

There is clearly a case for global equities given the depth and breadth of international markets beyond our banks and miners, the exposure to industries that don’t exist here and to emerging names that may lead the next wave of innovation.

And, of course, diversification is also a benefit on its own, in offering exposure to uncorrelated stocks, industries and economic forces that reduce portfolio volatility. With one sector always doing better than another, diversification reduces the temptation to chase whatever just performed the best.

But there is more to this story. While Australia has always been a concentrated market, dominated by two sectors and by a small number of names, the US market is now highly concentrated itself. At time of writing, the so-called ‘Magnificent Seven’ accounted for more than a third of the S&P 500’s market capitalisation.

There also remain significant advantages for Australian investors in retaining a significant domestic allocation beyond this country’s 2% footprint in global markets.

Broadly, these include Australia’s historically high dividend yields, franking credits for local investors, familiarity with domestic names, transactional simplicity, and reduced currency risk. For those in retirement, there is also a better match between investing in assets and funding their liabilities (i.e. future spending needs) in Australian dollars.

Australia’s big banks, miners, REITs and infrastructure stocks tend to generate high, stable cashflows and pay higher dividends. Traditionally higher cash dividend yields, together with the benefits of franking credits, add up to a total effective yield of about 4.5% including franking, compared with about 1.5% from global equities.

Familiarity with household local names (Woolworths, CBA, Telstra, AGL etc) also can be advantages for local investors. After all, one of the core tenets of investing is understanding what you are investing in.

All other things being equal, holding securities directly - which is more manageable with Australian shares - offers benefits over managed investments. It gives holders more control and flexibility, is closer to the source of income, and costs less. As well, pooled investments carry tax implications that are beyond the individual’s control.

The long-term view

While not seeking to downplay Australia’s recent relative underperformance, we don’t believe those advantages have gone away.

History tells us that performance trends come and go and that the smart strategy always is to focus on the long-term, while staying diversified and remaining true to the asset allocation that is best aligned with your own objectives.

Over 30 years or more, the returns from Australian versus international shares are similar. Reacting to short-term outperformance, as we saw in the late 1990s dot-com boom in the US, is usually a mistake. In that case, after the US boom ended in early 2000, Australia outperformed for the ensuing decade.

Decisions about relative domestic vs global exposure, in any case, should be driven by individual circumstance. For instance, those in retirement may benefit from a higher allocation to Australian equities given the importance of income and franking. On the other hand, those actively growing their capital, where compounding is the focus, may be justified in directing a greater weight to global equities.

Ultimately the right portfolio settings are those that are appropriate for your age, circumstances, goals and risk appetite. That doesn’t change regardless of what is happening in the outside world or what is dominating the news cycle.

And remember that systematic rebalancing offers a disciplined approach to taking profits during periods higher relative returns and topping up weaker performers.

Changing investment strategy because the grass looks greener elsewhere rarely works. Markets are cyclical, leaders are forever shifting place, and by the time you switch, the best gains may already have occurred anyway.

Before acting, we recommend asking yourself three questions:

- “Am I reacting to recent performance?”

- “Would I still do this if markets were flat?”

- “Does this fit my long-term plan?

If the answers to any of these questions is yes, the risk is you are over-reacting. Ultimately, like good gardeners, the most successful investors don’t long for their neighbour’s greener grass - they water their own lawns consistently.

Jamie Wickham, CFA is a Partner at Minchin Moore Private Wealth and former managing director, Morningstar Australia.