If market declines make you nervous, then you’re not alone. Especially now, when COVID-19 and its economic impact are fuelling feelings of uncertainty around the world.

But while bear markets can be extraordinarily difficult, they also can be moments of great opportunity. Investors who find the courage and conviction to stick to their long-term plans are often rewarded as markets bounce back. To help put recent markets into perspective, we outline three facts about market recoveries and three mistakes that investors should avoid.

Three facts about market recoveries

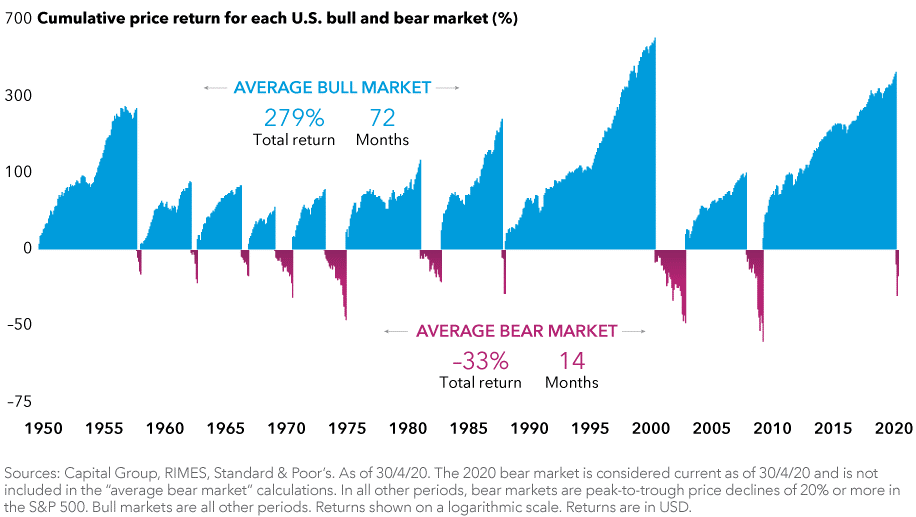

Fact #1: Recoveries have been much longer and stronger than downturns

The good news is bear markets have been relatively short compared with recoveries. They can feel like they last forever when we’re in them but in reality, they are much less impactful compared to the long-term power of bull markets.

Although every market decline is unique, in the US, the average bear market since 1950 has lasted 14 months. The average bull market has been more than five times longer.

The difference in returns has been just as dramatic. Even though the average bull has averaged a 279% gain, recoveries are rarely a smooth ride. Investors must often withstand scary headlines, significant market volatility and additional equity declines along the way. But investors who remain focused on the long term are often better equipped to look past the noise and stick to their plan.

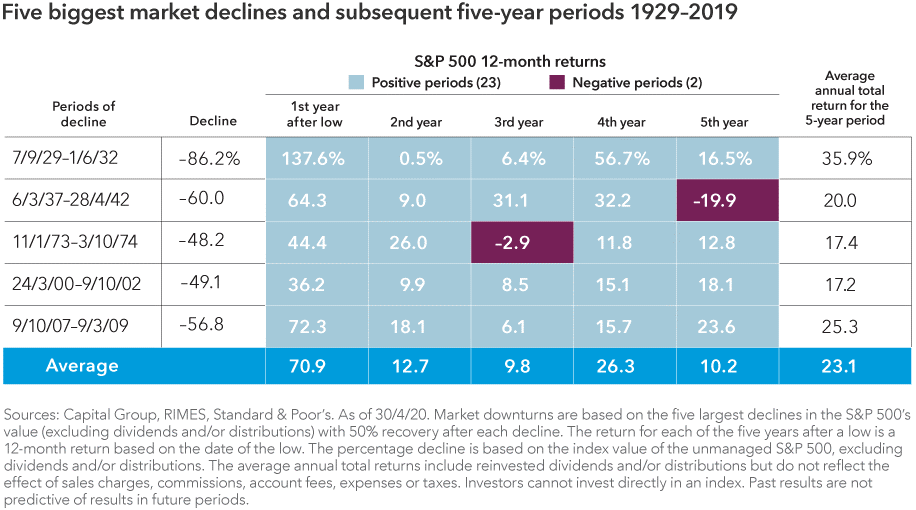

Fact #2: After large declines, markets have recovered quickly

Of course, we don’t know exactly what the next recovery will look like, but history shows us that stocks have often recovered sharply following steep downturns. We tracked the 18 biggest US market declines since the Great Depression, and in each case the S&P 500 was higher five years later. Returns over those five-year periods averaged more than 18% per year.

Returns have often been strongest after the steepest declines, bouncing back quickly from market bottoms. The first year following the five biggest bear markets over the last 90 years averaged 71%, underscoring the importance of staying invested and avoiding the urge to abandon stocks during market volatility.

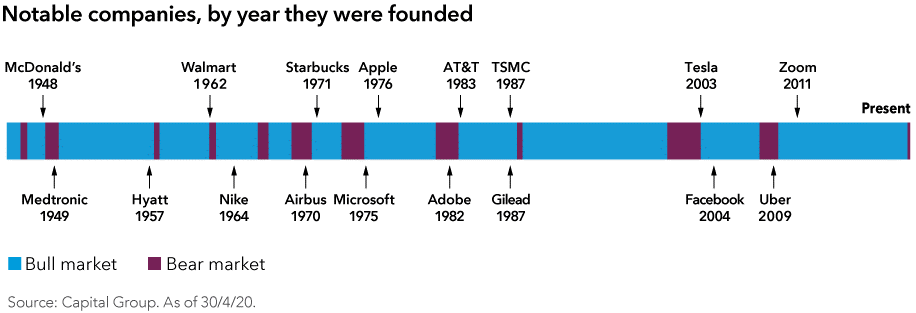

Fact #3: Some of the world’s most influential companies were born during market recoveries

Many companies started during tough economic periods and have gone on to become household names.

To highlight just a few in the US market:

- McDonald’s emerged in 1948 following a downturn caused by the US government’s demobilisation from a wartime economy.

- Walmart came along 14 years later, around the time of the ‘Flash Crash of 1962’, a period when the S&P 500 index declined more than 22%.

- Airbus, Microsoft and Starbucks were founded during the stagflation era of the 1970s, a decade marked by two recessions and one of the worst bear markets in US history.

- Not long after that, Steve Jobs walked into his garage and started a computer company called Apple.

History has shown that strong businesses find a way to survive and even thrive when times are tough. Those that can adapt to difficult conditions and become stronger often make attractive long-term investments.

Bottom-up, fundamental research is key to separating which companies may help lead a market recovery, and which are more likely to be left behind.

Three mistakes investors should avoid

Mistake #1: Trying to time markets

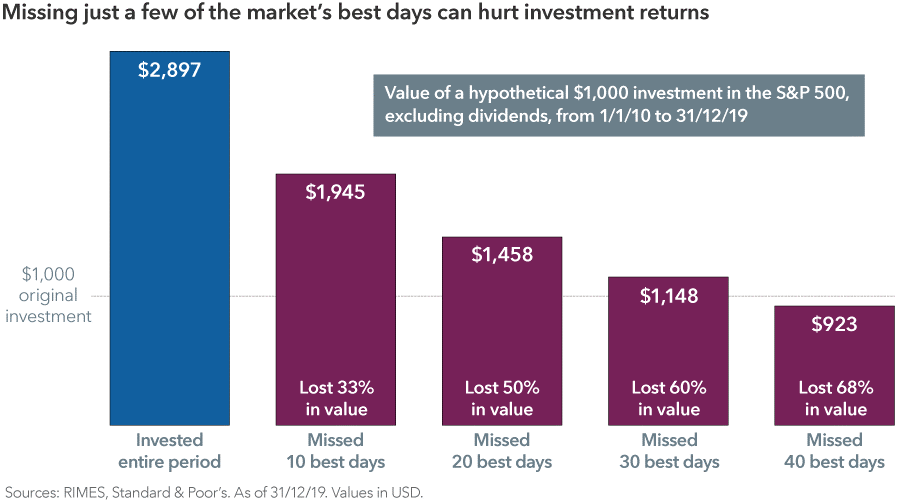

It’s time, not timing, that matters in investing. Taking your money out of the market on the way down means that if you don’t get back in at exactly the right time, you can’t capture the full benefit of a recovery.

Consider an example of a hypothetical investor who sold stocks during the US market downturn of 2008–2009, and then tried to time the market, jumping back in when it showed signs of improvement. Missing even the 10 best days of the recovery would have significantly hurt that investor’s long-term results. The more of the 'good' days were missed, the steeper the loss.

Investors who are more hesitant to put all their excess capital to work at once may want to consider dollar cost averaging, which often provides stability in volatile markets.

Mistake #2: Assuming today’s negative headlines make it a bad time to invest

Today’s economic and geopolitical challenges may seem unprecedented, but a look through history shows that there have always been reasons not to invest. Despite negative headlines, the market’s long-term trend has always been higher.

Consider an investment in the S&P 500 on the day Pearl Harbour was bombed in 1941. Someone who stayed invested for the next 10 years would have averaged a 16% annual return. Likewise, a $10,000 investment in the S&P 500 Index on the day Lehman Brothers declared bankruptcy in 2008 would have grown to over $30,000 10 years later. History has provided numerous examples of this.

Great investment opportunities often emerge when investors are feeling most pessimistic. The coronavirus outbreak may be unlike anything we have faced before but uncertainty is nothing new to the market, which continues to be resilient over time.

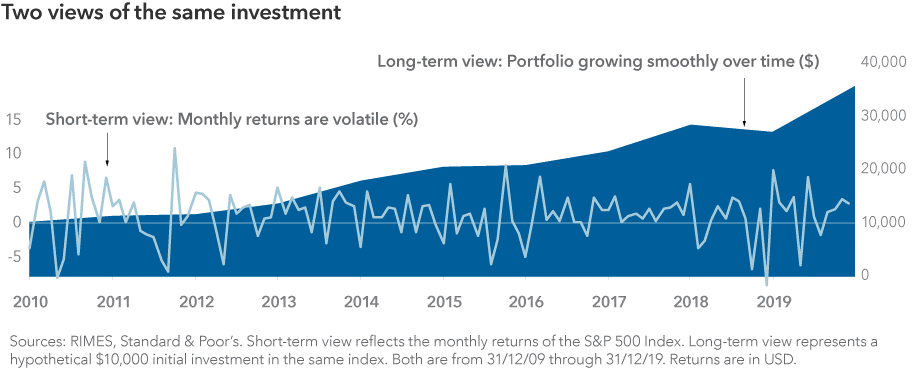

Mistake #3: Focusing too much on the short term

Market volatility is especially uncomfortable when you focus on short-term ups and downs. Instead, extend your time horizon to focus on the long-term growth of your investments and the progress you’ve made toward your goals.

Consider the chart below that shows contrasting perspectives of the same hypothetical investment. The short-term view is one that many investors have of their portfolios, tracing returns over short periods of time.

The long-term view plots the same investment over the same period, but shows annual change in the portfolio value invested instead. With this perspective, the short-term fluctuations have smoothed out over time, and the picture of a growing portfolio becomes clearer.

Bear markets don’t last forever. Maintaining a long-term perspective can help investors to focus on the goals that matter most.

Matt Reynolds is an Investment Director at Capital Group, a sponsor of Firstlinks. This article is general information and does not consider the circumstances of any investor. Please seek financial advice before acting on any investment as market circumstances can change.

For more articles and papers from Capital Group, click here.