The holy grail of investing is what legendary US fund manager Peter Lynch dubbed ‘multi-baggers’: stocks that return many multiples on your money. For companies to achieve this, they need turbocharged earnings growth, and that kind of growth is mostly found at the smaller cap end of the market.

When investors investigate small cap companies, many look at numbers: margins, sales, and earnings growth, return on capital, and so on. These are all important. They tell investors the result of hundreds, perhaps thousands, of business decisions and actions.

What’s often overlooked are the business models or strategies that drive these decisions and the final numbers that end up in the profit and loss, and balance sheet statements.

If you go back and analyse some of the biggest ASX small cap success stories of the past decade or two – JB Hi-Fi, Lovisa, Domino’s Pizza, AUB, and others - many fall into one of two camps: they’ve either expanded a single store format nationwide or consolidated a fragmented industry.

In this article, we’re going to deep dive into these two strategies, why they’ve been successful, and pointers to where the next multi-bagger might lay.

Expanding single store formats nationwide

One of the most common business strategies is to take a proven store format and expand it statewide, or nationwide.

JB Hi-Fi (ASX:JBH) is one of the best examples of this strategy in action. The company was set up in 1974 by entrepreneur John Barbuto (hence the ‘JB’ in JB Hi Fi) with a single store in East Keilor in Victoria. Barbuto wanted to deliver a specialist range of Hi-Fi and recorded music at low prices. He sold the business in 1983 and by 1999, it had been under various owners and another nine stores had been opened.

Enter Richard Uechtritz and Terry Smart. Both these men were running Kodak’s operations in Australia at that time. Prior to that, Uechtritz had built and sold the Rabbit Photo chain. Uechtritz and Smart, along with Macquarie and others, bought into the company in 2000.

When they bought it, JB Hi-Fi had 10 stores with revenue of $135 million. In the next three years, they opened 16 new stores along the Eastern seaboard and turnover increased to $355 million. That’s when they decided to IPO the company.

On October 24, 2003, JB Hi-Fi debuted on the ASX at an IPO price of $1.55. The shares jumped 42% on the first day. It turns out many investors liked the JB Hi-Fi story.

It’s fascinating to read the company’s IPO prospectus. Management was clear in its aims and what made JB-FI distinctive.

On the company’s competitive advantages, the prospectus had this to say:

“ - low cost and large scale operations that are driven, in large measure, by sales per square metre of selling space of around $25,000;

- discount positioning which the Directors believe provides protection from the retail economic cycle;

- ability to offer leading brands in each product category through strong relationships;

- specialist image through carefully targeted focus on home entertainment products; and

- distinctive branding and prominent retail locations.”

In other words, JB Hi-Fi sold discounted home entertainment products, in smaller than normal selling spaces though good locations, with colourful branding, and knowledgeable staff.

The prospectus mentioned the extensive retail experience of management and the goals of the company, including opening at least five new stores in 2004, and accelerating the store rollout in Sydney, Adelaide, and Perth over the following three years.

In interviews in subsequent years, Uechtritz acknowledged that JB Hi-Fi was a category killer. At the time, Harvey Norman was in computers and Bunnings was in hardware, and it was his company in home entertainment.

Fast forward to today, and the company has more than 200 JB Hi-Fi stores in Australia and New Zealand with revenue of close to $6.45 billion and group sales (included The Good Guys) of $9.63 billion. And Terry Smart is Group CEO.

Source: Morningstar

Another example of a company that successfully rollout out a store format nationwide, and in this case overseas, is Domino’s Pizza (ASX:DMP). Until recently, it was a market darling.

The first Domino’s store in Australia was opened in Queensland 40 years ago. It offered home delivery about two years after the concept was first introduced in the country. The Australian and New Zealand Master Franchise was bought by Silvio’s Dial-a-Pizza in 1993, and two years later, and the two brands merged and were rebranded as Domino’s Pizza.

Funnily enough, a young man by the name of Don Meij worked as a delivery driver for Silvio’s in 1987 and when Silvio’s merged with Domino’s, Meij became General Manager. Meij became a Domino’s franchisee in 1996, expanding to own 17 stores. He sold these stores to the company for a 12.5% equity stake in Domino’s in 2001.

Meij became CEO of Domino’s in 2002 and the company became Australia’s first publicly listed pizza chain on the ASX in 2005.

When it IPO’ed, Domino’s had 375 stores in Australia and New Zealand and sold 700,000 pizzas a week. The shares listed at $2.20.

From the start, Meij stuck primarily to a franchise model to roll out stores aggressively and used technology effectively to drive online sales and delivery. Over the past decade, the growth story accelerated through the acquisition of European and Japanese Master Franchise agreements.

Today, Meij is still CEO and Domino’s has 3,800 stores across the world, including around 730 in Australia. Here, Domino’s has crushed competitors such as Pizza Hut. Pizza Hut concentrated more on dine-in style stores. Domino’s now has 50% market share in Australia versus Pizza Hut’s just 10%.

Source: Morningstar

Hindsight’s tricks

It’s easy to look at these kinds of stocks and think their successes were inevitable. But they weren’t. That’s a trick of hindsight.

To expand from one store to thousands requires an immense amount of work and a bit of luck. JB Hi-Fi and Domino’s had to nail the concepts for their first stores, and as they expanded, they needed to get store locations right, manage inventories, supply chains, hire staff, managers, manage finances, legal issues and it goes on.

What they both got right from the start though was that their formats were replicable and could be rolled out quickly if they executed right.

The strategy of rolling out store formats nationwide isn’t a new one, of course. Many retailers and restaurants in Australia have taken their inspiration from the US. From older companies like McDonalds, Walmart, and Costco, and newer companies like Chipotle and Chick-fil-A.

Unlike America, Australia is small and that means there are limits to how much a company can grow here. That’s why many businesses head overseas, though that increases risks.

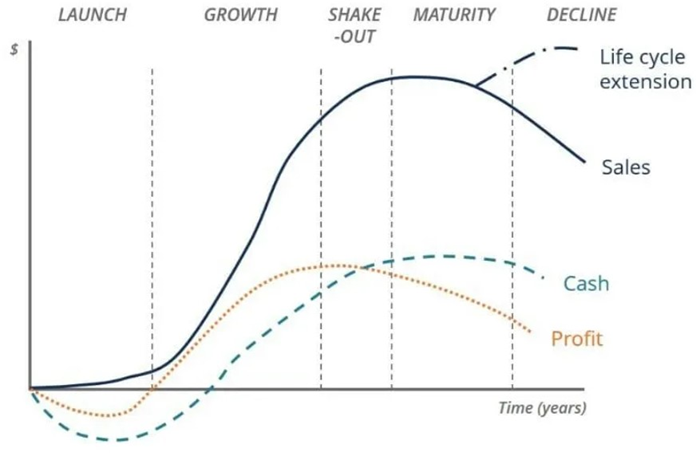

The lifecycle of companies

One way of looking at companies looking to aggressively expand store rollouts is by thinking about the lifecycle of businesses. The theory goes that businesses progress through five stages: launch, growth, shake-out, maturity, and decline.

When JB Hi-Fi and Domino’s IPO’ed, they were at the beginning of their growth phase. As a general rule, investors in search of small cap multi-baggers should look to buy companies either in the launch or first half of the growth phases.

When these types of companies start expanding overseas, they are probably hitting the maturity or even decline stages of the lifecycle. I’d suggest Harvey Norman is in one of these two stages. The jury is out on Domino’s Pizza too, though they do seem to have a decent shot at the overseas ventures.

Source: Corporate Finance Institute

Consolidating fragmented industries

Another business model that’s proven successful on the ASX is that of consolidators of fragmented markets. Say 50 companies have 2% each of an industry, and two of those companies gobble up the others and get to 30% market share each. That can prove enormously profitable for both companies and their shareholders.

As with the first business model, it isn’t easy to execute. Ideally, consolidators don’t want to pay too much for companies that they acquire, don’t want to take on too much debt with the purchases, want to get cost synergies from their acquisitions, and integrate companies into the culture of their own businesses.

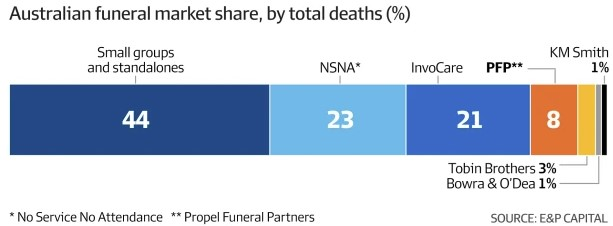

A good example in recent decades is the funeral industry in Australia. Traditionally, this industry has been dominated by family-owned funeral homes. InvoCare (taken over by private equity) saw the opportunity and acquired many of these mum and dad owned homes.

Now a second company, Propel Funeral Partners (ASX:PFP) is pursuing a similar strategy. It’s grown from having one funeral home ten years ago to having 180 locations today. In 2015, it had 1.2% market share in funeral services. Today, it’s got 8%. Since 2015, Propel’s revenue has increased 15x and operating net profit is up 13.9x. The company’s share price listed at $2.70 in 2017 and is up 82% since then, excluding dividends.

Source: Morningstar

Yet the opportunity for Propel and InvoCare still appears compelling. Combined, they only control 29% of the industry.

It’s little wonder that Propel is also getting interest from private equity.

There are lots of other example of companies attempting to consolidate industries. Commercial insurance brokers would be one. AUB (ASX:AUB) has been central to this, and it’s managed to compound total returns at 17% per annum over the past 15 years.

Source: Morningstar

US examples

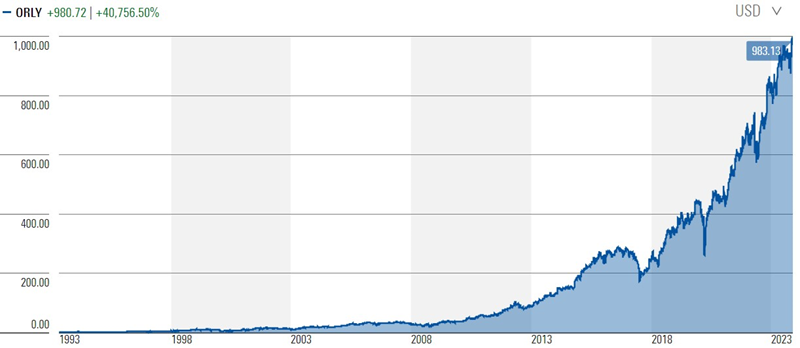

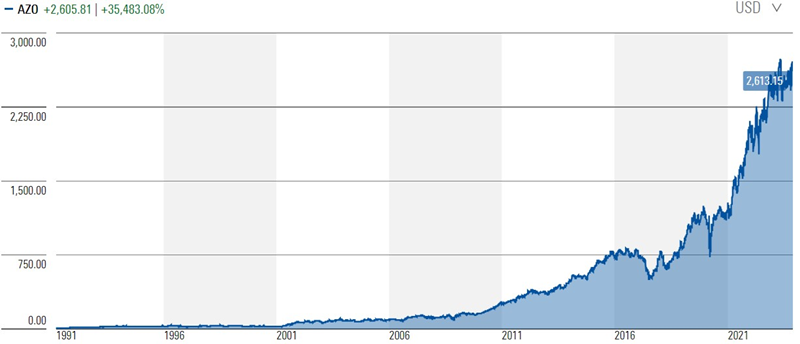

Overseas, there are also plenty of examples where this business model has been successfully applied. In the US, the auto parts industry used to be dominated by independent owners until O’Reilly Automotive (NYSE:ORLY) and AutoZone (NYSE:AZO) started buying them. They’ve both been highly effective with their strategies and their stocks have been some of the best performing in US, compounding returns at 27% and 24% respectively over the past 15 years.

Source: Morningstar

Source: Morningstar

An old example of the consolidation of an industry is in waste management in the US. The industry now has a handful of large players, compared to 30 years ago when independent owners commanded the lion's share.

The guy that led the industry transformation was an entrepreneur named Wayne Huizenga. He started with a single garbage truck in 1968 and built Waste Management (NYSE:WM) into a Fortune 500 company.

Source: Morningstar

After Waste Management, Huizenga went onto to found two other Fortune 500 companies, Blockbuster and AutoNation (NYSE:AN). Interestingly, he built these companies using the other business model mentioned in this article: expanding a store format nationwide. The details on Huizenga’s stellar career are captured in the highly recommended book, The Making of a Blockbuster.

It’s worth noting that consolidating a fragmented industry isn’t without risks. Businesses employing the strategy can expand too fast, take on too much debt, not integrate acquirees properly, or a combination of these and other factors. In this regard, a cautionary tale comes from the collapse of Australian childcare operator, ABC Learning, in 2008.

James Gruber is an assistant editor at Firstlinks and Morningstar.com.au