Something has been bothering me.

The recent budget has produced its usual flurry of commentary (and rightfully so). However, one thing that has stood out over the last month or so, is a pervasive sense of uncertainty. Perhaps not only a product of the measures themselves, but the contradictory explanations offered by those responsible for them.

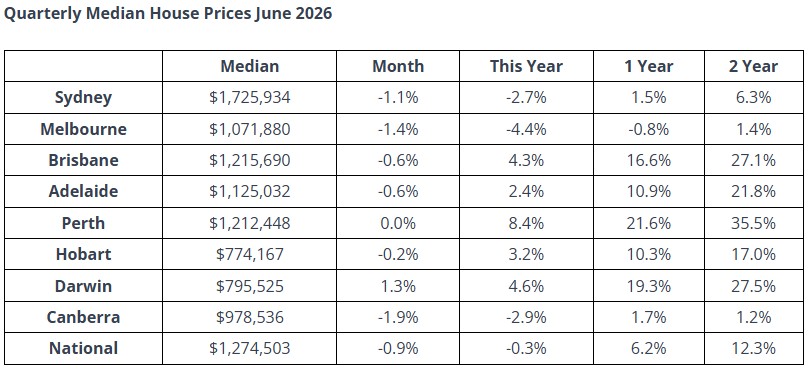

June housing market

Residential real estate underpins Australia’s wealth landscape. Whether this continues to be the most productive destination for capital is a question worth debating, and one I’m keen to hear readers’ views on. Either way, it’s no surprise that many eyes have been cast on property valuations since May 12th. Findings from Property Update show that house prices in capital cities have continued to fall over June with the monthly rate of decline now accelerating.

Source: Property Update. “Falling home prices accelerate over June”. 29 June 2026.

Trouble in paradise

Naturally, these headline figures have elicited fears of a housing-induced economic downturn.

When recently questioned about dwindling dwelling values and lower auction clearance rates, Housing Minister Clare O’Neil stated that "We see periods of very significant house price growth and then we see the market make a correction, and that's what we're seeing at the moment."

Indeed, O’Neil is partially correct about the cyclical nature of the Aussie housing market. But as AMP reports, the down-cycles tend to be short-lived and prices generally fall ~5%, which they view as modest. However, the point of contention here was the technical definition of "correction", which generally implies a drop of 10% in equity market terms.

Source: AMP.

Jim Chalmers recently walked back O’Neil’s comments about a “correction”:

“We have seen a softening in house prices in recent months even before the Budget, and that’s a reflection of a whole range of factors including changes in interest rates, softness in the broader global and domestic economies, as well as any other influences from the Budget and the like.”

This diverges from the view at the beginning of this budget cycle, where it was asserted that the government were “taking pressure off the housing market, by taking a serious approach to housing…”. It would be intellectually dishonest to infer that easing some of this pressure (as described) wouldn’t reveal itself in the eventual cooling of prices.

The result of this back and forth between O’Neil and Chalmers is a muddled message that has satisfied very few. A far cry from any unilateral agreement on the future of residential property prices. But this isn’t a discussion about semantics. Importantly, I think it raises a simpler question: if affordability was the stated objective of budget measures, is a moderation in prices not a foreseeable (perhaps even necessary) outcome? And if that is not the objective, then what is?

Shadow Treasurer Tim Wilson described the situation as “complete disarray,” arguing the Government did not appear to know its own policy aim. Whether or not one agrees with that assessment, the contradiction is undeniable. It is difficult to present a policy as ambitious while simultaneously assuring other constituencies that nothing fundamental will change. In attempting to offend no one, the Government has managed to confuse everyone.

A broader note on the budget blame game

One thing the budget coverage has made painfully clear is how quickly parts of the media will reach for a generational-war narrative. Older Australians have been cast as beneficiaries of an inflated market and younger Australians as victims of it. This budget has sought to reverse this "intergenerational inequity", with the changes being framed as dramatic win for young Aussies at the expense of older investors. As though assigning fault to one age group will improve affordability for another.

As someone in the younger cohort, I understand the appeal of that storyline, but it does little to improve my own prospects or those of my peers. Vilifying predecessors who were simply beneficiaries of the economic circumstances of their time, does nothing to address the structural forces shaping today’s market. It does the opposite. It reduces a complex, long-term issue to a simplistic morality play.

Housing affordability has always been a structural issue shaped by planning constraints, construction capacity, migration flows, tax settings and decades of bipartisan decisions. It is not the product of personal virtue or personal failure. The danger in this framing is that it obscures the real issues and encourages resentment rather than understanding. Playing the generational blame game is a poor substitute for serious policy introspection.

This Budget (just like every other one before it) deserves scrutiny. Investors across all generations alike make long-term decisions based on the signals they receive. What concerns me is the mixed signalling. If the Government intends to reshape the price landscape, it should say so plainly. If it intends to preserve the status quo, then it should say that plainly. What it cannot do, is attempt both simultaneously and then expect the public to interpret the ambiguity in a constructive way.

Simonelle Mody

Also in this week's edition...

After the recent changes on SMSFs using LBRAs to purchase new residential properties, Meg Heffron explores how wide the ban really is.

It's been a tough time for Aussie equities after a long record of outperformance. Mark LaMonica examines whether the lag is a temporary setback or whether there are structural forces at play.

Tony Dillion models the 30% minimum tax on capital gains to reveal anomalies that introduce unexpected distortions.

Sam Heithersay from Fidelity discusses why the next generation of Australian equity leadership may not be found in familiar sectors.

Global growth is facing mounting pressure from all angles. Matt Reynolds from Capital Group believes AI-related investment may prove enough to reshape the outlook for markets.

Many retirees pass away with their wealth intact. Joseph Darby looks at a case study from New Zealand to help determine what drives the cautionary spending behaviour.

IPO frenzy has fizzled but is yet to disappear. Director of Retirement Planning, Christine Benz shares her own investment philosophy and how a set of core beliefs can tune out distractions.

Curated by Simonelle Mody and Leisa Bell

***

Weekend market update

From Shane Oliver, AMP

Global shares saw strong gains over the last week as the oil price remained down, inflation fears subsided and slower US payrolls removed some pressure for a US rate hike. The positive global lead along with with a rebound in health care stocks saw Australian shares rise around 0.9% with gains in health, mining, IT and financial shares more than offsetting weakness in utilities and property shares. Another rotation in US shares. While the US share market remains below its recent record high this partly reflects another healthy rotation from tech to non-tech shares with the equal weighted S&P 500 reaching new highs.

Despite reduced inflation fears, bond yields actually rose slightly in the last week. Prices for metals and iron ore fell but gold and Bitcoin rose as the $US fell which also helped the $A get rise above $US0.69. So far Bitcoin appears to be holding technical support around $US60,000 following a roughly 53% fall from its October high. If it’s able to bottom here it may be seen as very positive potentially breaking out of the four year cycle of 80% falls as it matures.

Despite a rocky ride the interim US/Iran peace deal appears to be holding together with the flow of ships through the Strait of Hormuz remaining up from lows through the March-June period, despite a setback a week ago as the conflict appeared to be briefly flaring up again.

This in turn has seen oil prices fall to slightly above where they were before the War. However, scope for a further fall in the near term may be limited with the risk of some rise as the flow of ships through the Strait remains depressed and the peace deal still looks fragile with difficult to resolve issues around Iran’s desire to control the Strait, its nuclear program and the Israel/Hezbollah conflict all posing a threat with the risk it could all flare up again.

The last financial year saw another year of solid returns despite a long worry list including last year’s US tariffs and this year’s US war with Iran – but can it continue? Sure Australian shares lagged with just a 6.1% return but that was still above inflation and most bank account rates. But global shares returned around 23% in local currency terms with Japanese and emerging market shares being the star performers. Can it continue? Our assessment is that shares will continue to provide reasonable returns over the year ahead, albeit with significant bouts of volatility. The combination of sticky inflation, an upwards drift in central bank interest rates, worries about an AI bubble, huge US IPOs, political uncertainty around the US mid-terms and high risks around the Iran peace deal are likely to continue to result in a volatile ride with a high risk of yet another correction. But the absence of a recession, solid profit growth, Trump likely to pivot to more consumer-friendly policies ahead of the mid-terms and the Fed and RBA likely to cut rates next year should result in okay overall returns.

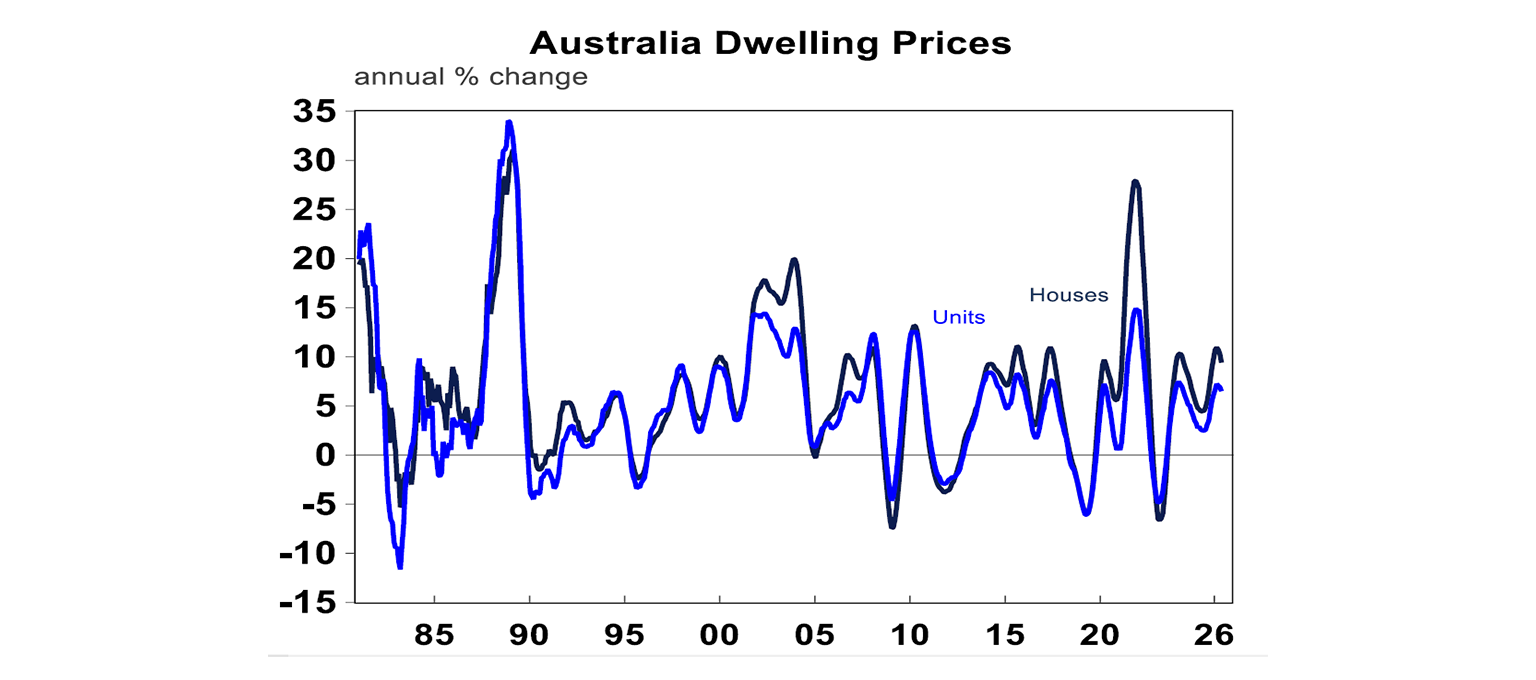

The home price downturn accelerated in June with prices falling 0.4% m-o-m and the previous two quarters revised to show declines. While the slide is being led by Sydney and Melbourne, Brisbane and Adelaide look like they will go negative soon too.

So far it’s just a flick of the top for house prices and the sort of thing you would expect when interest rates rise. National average prices are down around 1% from their high after a 26% surge over the prior three years. But the downturn likely has further to go reflecting the impact of rate hikes, low confidence, poor affordability and the move in the Budget to wind back virtually all investor property tax concessions.

Given the role the concessions had played in attracting investors into the property market over many years their removal has logically seen many investors retreat to the sidelines waiting for lower prices and higher rents before committing, but it also likely means that unaffected buyers will also hold back to see what happens. We now expect a 2% fall in property prices this calendar year and a 6% fall over the next 12 months, resulting in a top to bottom fall of around 7%. If unemployment rises substantially the fall is like it be greater. By the June quarter next year property prices are likely to bottom as the market starts to focus on RBA rate cuts in 2027.

Housing credit growth for May is showing signs of rolling over as rate hikes hit, but as it lags actual lending commitments it’s too early to see the impact of the Budget tax changes on lending to investors.

One source of support preventing a deeper slump in property prices is the housing shortfall and this is unlikely to change anytime soon. Home building approvals fell 1.1% in May with a 7.3%mom fall in volatile unit approvals. They are trending around 204,000 at an annual rate which is up from the 2023 low but still below the Housing Accord target of 240,000 a year which is necessary to meet regular annual demand and eat into the shortfall. The rise in mortgage rates risks driving a slowing in approvals from here.

Wages growth under newly approved enterprise bargaining agreements rose a notch in the March quarter but is still around 4%. However, the pick-up in inflation and minimum and award wages risks some acceleration ahead.

Latest updates

PDF version of Firstlinks Newsletter

Monthly Investment Podcast by UniSuper

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Plus updates and announcements on the Sponsor Noticeboard on our website