Global economic growth is coming under pressure due to the Iran war, rising oil prices and ongoing trade disputes. But one powerful engine is more than making up for it: AI-related investment spending.

My colleague, economist Darrell Spence believes the artificial intelligence boom is so massive that even if activity in all other sectors contracted, overall economic growth could remain in positive territory, especially in the United States.

We have been on the cautious side when it comes to the outlook for US growth, but it is still possible that GDP could be significantly higher than expected — in the range of 2.5% or more. That is how much the AI arms race is contributing to overall economic growth.

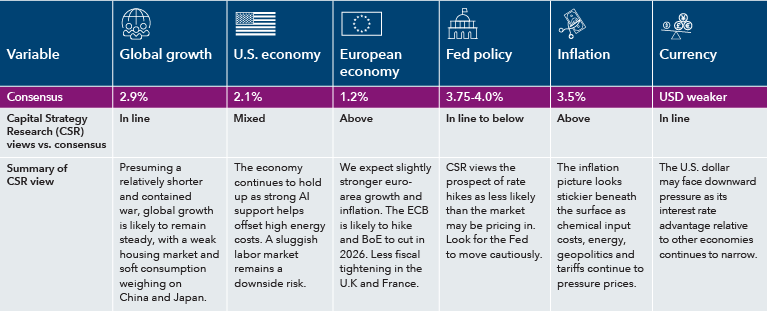

Iran war and AI are pulling the global economy in opposite directions

Sources: Capital Group, Bloomberg. As of 31 May 2026. Consensus figures are based on mean Bloomberg consensus estimates for US CPI change in 2026 (“US inflation”) and 2026 year-over-year GDP growth for the world (“global growth”), the United States (“US economy”) and the European Union (“European economy”). Consensus figures for “Fed policy” are based on the implied federal funds target range based on futures pricing for December 2026. Consensus “currency” figure is based on DXY futures pricing through December 2026. The views of individual portfolio managers and analysts may differ from Capital Strategy Research (CSR) views. Stagflationary: economic environment categorised by high inflation coinciding with slow economic growth (GDP) and high unemployment. ECB: European Central Bank. BoE: Bank of England. DXY: US Dollar Index.

For the US and the rest of the world, much depends on the duration and severity of the Iran war, mounting inflationary pressures, weakening consumer fundamentals, and whether the AI boom marches on or fizzles out.

There is a tug of war between these global economic forces, and it could be a while before a clear winner emerges. In the meantime, economic growth driven solely by one sub-sector of the economy may not necessarily be healthy growth.

Likewise, my colleague Beth Beckett says Europe is facing a stagflationary shock before year-end, as higher energy prices weigh on activity. She expects a much smaller shock than we saw in 2022, thanks in part to stronger manufacturing activity and looser fiscal policy in Germany.

Higher defence spending in Europe has already provided a significant boost to the region’s aerospace and defence companies, and that is expected to continue as geopolitical conflicts increasingly shape the global landscape.

In Asia, look for a weak housing market and slowing global trade to weigh on China’s economy while Japan remains sluggish as the conflict in the Middle East impairs export activity. Both countries are dealing with an energy crunch due to the Iran war. As long as the Strait of Hormuz remains closed or partially blocked, restricted oil supplies could further constrain economic growth, particularly once strategic reserves are depleted. Prior to the war, China was by far the largest buyer of Iranian oil.

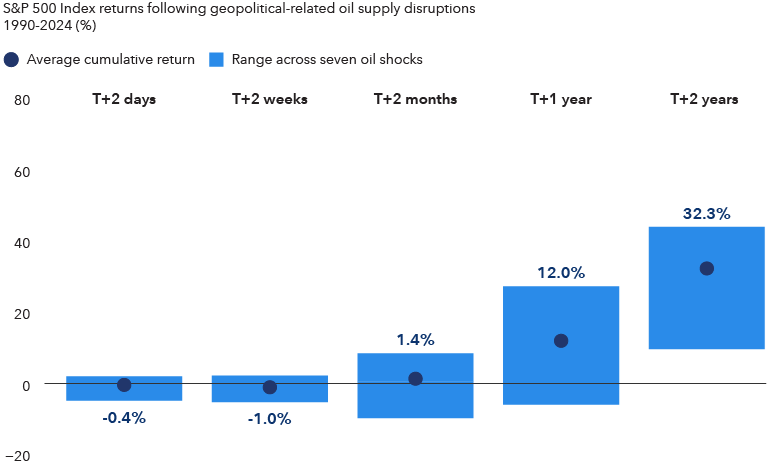

Oil shock is a risk, but we have been here before

The Iran war is a stark reminder that the world still runs on oil. When supply is threatened, the impact of higher oil prices spreads quickly to businesses, consumers and global markets.

About one-fifth of the world’s oil supply moves through the Strait of Hormuz, off the coast of Iran, so any disruption there is almost immediately reflected in fuel prices. Even in the United States, the world’s largest oil producer, the price of gasoline at the pump has jumped nearly 53% since the war started.

My equity portfolio manager colleague Paul Benajmin recently said that there are very real economic risks, and the costs would only compound as the war drags on. He believes a persistent conflict could trigger weaker equities, a stronger US dollar and widening credit spreads.

The good news is, over the past two decades, stock markets have generally bounced back from geopolitical shocks because they have not resulted in prolonged physical supply outages. Across seven oil supply shocks since the First Gulf War in the 1990s to Russia’s invasion of Ukraine in 2022, equities fell on average by 1% two weeks following the disruption, then rose 1.4% a month later, 12% a year later and 32.3% over the next two years. It’s a helpful reminder that markets are forward-looking and may already be anticipating a resolution to the present crisis.

Wars have pushed oil prices higher, but stocks have recovered relatively fast

Sources: Capital Group, Bloomberg, S&P Global. Geopolitical shocks include: Gulf War (8/1990), Second Gulf War (3/2003), Niger Delta supply disruptions (2/2006), Arab Spring, Libya Civil War (2/2011), Hormuz closure risk, Iran sanctions (12/2011), drone attack on Saudi installations (9/2019), Russian invasion of Ukraine (2/2022). Event dates are aligned to the nearest observable market price (“T”). If a shock occurs on a non-trading day, the prior trading day is used as the start date. Horizon returns are measured using the first available trading day on or after the stated calendar horizon (e.g., “T+2 days”). Figures reflect total returns. As of 31 May 2026.

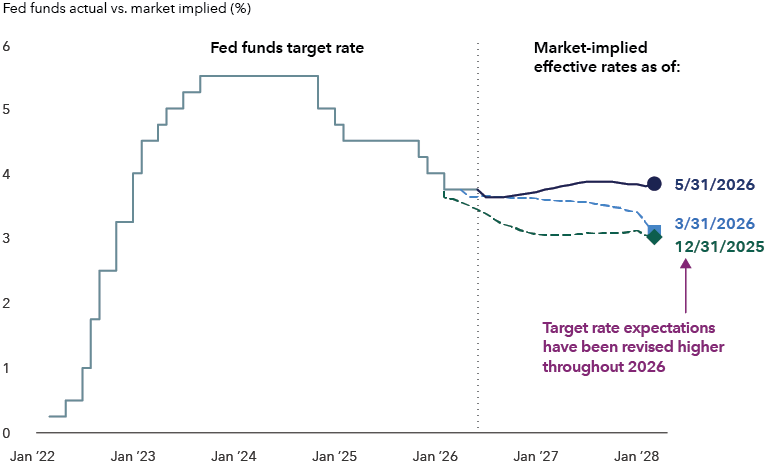

Interest rate outlook is murky at best

While the recent Federal Reserve (Fed) meeting kept rates unchanged, Chair Kevin Warsh signaled a more hawkish tone with inflation concerns indicating a potential tightening bias at the Fed.

Indeed, US employment data may hold the key to the Fed’s next move, even as war-driven inflation intensifies. Fed officials have indicated in recent months that supporting the labour market may have to take precedence over the fight against inflation.

Inflation has moved sharply higher. The US Consumer Price Index climbed 4.2% in May, the largest jump since April 2023. The increase was primarily driven by higher energy costs, which rose 23.5% compared to a year ago.

My fixed income colleague Chitrang Purani notes that labour markets are weaker than they were a few years ago but remain steady overall. He says the war is keeping inflation above the Fed’s 2% target and may weigh on non-AI business investment as well as consumer demand. That combination increases the risk of a more pronounced slowdown in growth.

Policymakers will remain patient: the labour market has been stable, with slower job growth offset by slower labour force expansion, but if this balance were to shift toward a rising unemployment rate the Fed will likely look past near-term inflation risks.

With the U.S. job market softening, the Fed has room to cut rates

Sources: Capital Group, Bloomberg, US Federal Reserve. Fed funds target rate reflects the upper bound of the Federal Open Markets Committee’s (FOMC) target range for overnight lending among US banks. As of 31 May 2026.

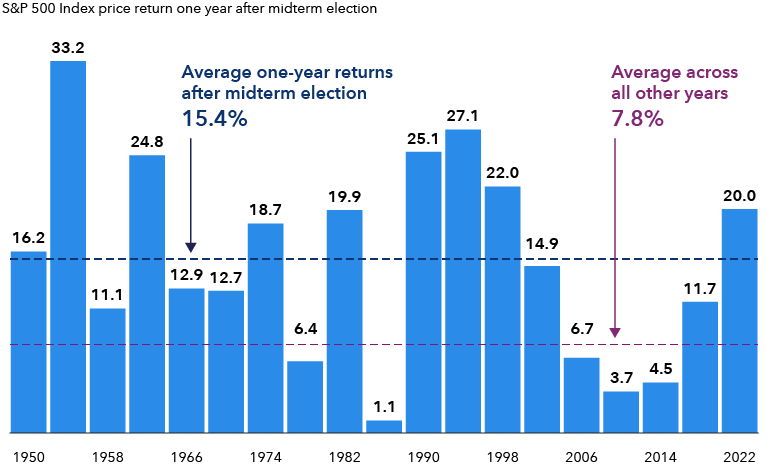

US midterm elections: Volatility, then stocks have rallied

With everything else happening in the world, investors may not be focused on the US midterm elections yet. But this pivotal contest is just a few months away, and it could have a noticeable effect on the stock market, if history is any guide.

To gauge the impact, Capital Group examined more than 90 years of S&P 500 Index data, and it turns out that stocks do exhibit some unique characteristics during midterm years. Market volatility tends to rise, returns tend to be muted and, once the outcome is known, stocks tend to rally.

So far, the competing forces of rising corporate earnings, the Iran war and a powerful rally in AI stocks are driving market activity but that could change as investors turn their attention to what is likely to be a rancorous election season.

US stocks have generally rallied after midterm-election volatility

Sources: Capital Group, S&P Global, RIMES. Calculations use Election Day as the starting date in all election years, and 5 November as a proxy for the starting date in other years. Only midterm election years are shown in the chart. Price returns exclude the reinvestment of dividends and capital distributions. As of 31 December 2025.

The silver lining is that returns have tended to be strong during the full year following midterms elections, averaging 15.4% since 1950. Still, for long-term investors, these short-term moves do not normally mean much. My colleague Chris Buchbinder believes there may be bumps in the road, and investors should brace for short-term volatility, but don’t expect election results to be a huge driver of investment outcomes one way or the other.

Plus, at this point, it is just too close to call.

Capital Group’s political economist Matt Miller sums this up well, in saying that historically speaking, the party in power tends to face setbacks in the midterms, and so history favours the Democrats. But remember, the US is still far from Election Day. Five months is a lifetime in politics. He believes we will see an enormous amount of energy and well-funded advertising campaigns that could make this election closer than people expect. It might just give Republicans a chance to eke out what today would be considered a surprise win.

Matt Reynolds is an Investment Director for Capital Group Australia, a sponsor of Firstlinks. Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This article contains general information only and does not consider the circumstances of any investor. Please seek financial advice before acting on any investment as market circumstances can change.

This content is issued by Capital Group Investment Management Limited (ACN 164 174 501 AFSL No. 443 118), a member of Capital Group.

© 2026 Capital Group. All rights reserved.

For more articles and papers from Capital Group, click here.