If you’ve walked past ABC Bullion in Sydney’s Martin Place in recent months, you may have noticed the steady queues forming outside. What’s behind the recent ‘gold rush’?

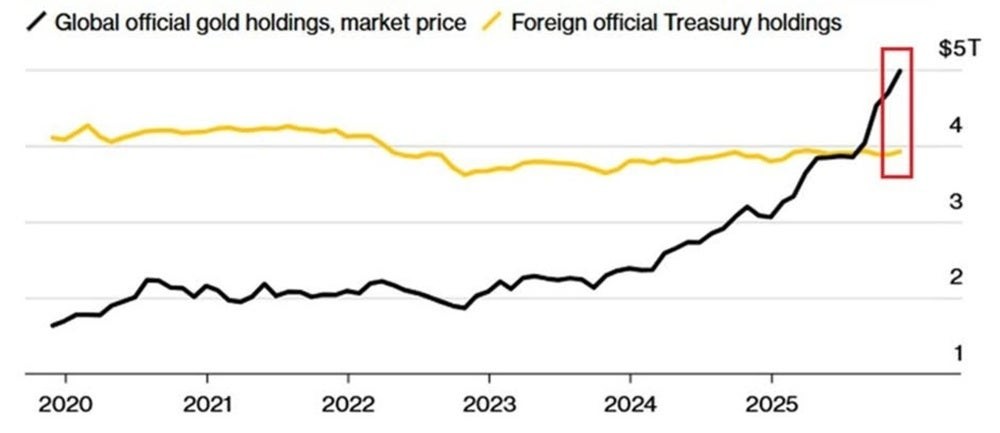

Gold recently overtook US Treasuries as the largest reserve asset held by foreign central banks. A reserve asset is a store of value that a country’s central bank keeps on hand (such as gold or foreign currency) to help steady its economy during times of uncertainty and meet international payments when needed. By early 2026, central banks were holding about US$4 trillion in gold, slightly more than the roughly US$3.9 trillion they held in US government bonds.

Gold has overtaken treasuries in central bank FX reserves

Source: IMF, Department of Treasury. Note: World gold reserves marked to market at month-end. Some countries may not declare their up-to-date gold holdings to IMF.

The shift happened for two main reasons: gold prices jumped nearly 70% last year, making existing holdings more valuable, and many countries have been steadily buying more gold to reduce their reliance on the US dollar.

This is not speculative trading. It reflects a fundamental reordering of how institutions think about money, risk, and value.

A structural shift in money, debt and reserves

Earlier in the year, the price of gold reached a record high of US$5000 per ounce. Silver also surged past US$100 per ounce before retreating sharply. At the centre of the gold and silver rally is what many market analysts describe as the debasement trade, which is the belief that fiat currencies will continue to lose purchasing power as governments rely on borrowing and monetary expansion.

Governments can print money without limits, expanding the supply of fiat currency at will. Gold supply, by contrast, is constrained by how much can be physically mined, roughly 2% per year of the total above-ground stock.

That imbalance has become more visible as US federal debt has climbed beyond US$38 trillion, while new mining projects take a decade or more to reach production. Since 2018, global gold mine supply has grown steadily, with near-zero year-on-year change, limiting the market's ability to respond to strong demand.

And leading the demand for gold are central banks, which have purchased over 1000 tonnes a year between 2022 and 2024. This is a deliberate geopolitical strategy to diversify away from dollar-denominated assets amid sanctions risk and de-dollarisation pressures.

Retail investors have also driven high demand, buying gold through physical bullion (like the one in Sydney’s Martin Place), exchange-traded funds, and digital platforms surged last year, while silver ETFs absorbed tens of millions of ounces. On Chinese social media, gold products even became a consumer trend.

Gold and silver’s appeal (and hidden risks)

Gold is widely viewed as a safe haven, but its risk profile depends on exactly how it is held.

Physical gold in a vault carries no default risk because it is not a liability of any institution. But gold held through ETFs or other paper instruments introduces a chain of counterparty dependencies: custodians, sub-custodians, clearing agents, and market-makers.

The price of silver is more volatile than gold, in part because more than half of global silver consumption now comes from industry – especially in technology and clean energy – as well as investment demand, which makes its price more sensitive to economic cycles. Silver is an essential component in solar photovoltaic panels, where its unmatched electrical conductivity makes it technically irreplaceable in current technology.

Around 70% of silver production is a by-product of other mining activity. This means silver supply is largely unresponsive to silver prices. Miners cannot simply ‘ramp up’ silver production when prices rise.

That imbalance has left the silver market in structural deficit for several consecutive years. According to Reuters, China’s decision to impose export licensing controls from January 2026 further tightened supply, contributing to silver’s volatile swings.

What investors should take from the recent surge?

Recently, gold and silver both posted their worst single-day performances in decades. It was reported that the nomination of a new US Federal Reserve Chair under Donald Trump, to replace Jerome Powell, triggered a rapid reassessment of potential rate cuts by the Federal Reserve, strengthening the US dollar and putting pressure on precious metals in the short term.

The sell-off was driven by technical deleveraging rather than any fundamental shift. The carnage was concentrated in speculative and leveraged positions – and not in fundamental demand.

Gold rebounded quickly, reinforcing its role as a defensive asset – quite literally proving its worth when markets come under pressure. In 2025, gold began its parabolic move well before equity markets showed meaningful stress. Gold began ‘sniffing out’ deteriorating conditions, including fiscal sustainability concerns, rising geopolitical tensions, and a loss of confidence in government institutions.

What this means for investors is that gold and silver are fundamentally nuanced – while they can play a role in diversification, they generate no income and can be volatile over the short term, which means they’re potentially not as safe as many make them out to be.

Gold is, in a meaningful sense, a speculative asset. Its value beyond industrial use is based on collective belief in its worth.

For investors, the question of whether now is the right time to buy gold or silver depends on their goals and risk tolerance. Precious metals can play a defensive role in a long-term portfolio, but after a sharp price rise, investors should be aware that further short-term gains are uncertain and volatility can be significant.

Professor Francisco Barillas Bedoya is the Head of the School for Banking and Finance at UNSW. This article was originally published by UNSW’s BusinessThink research platform.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results, and investors should consider their own circumstances before making investment decisions.