This article asks three questions. Is Australian housing overpriced? If so, why? And, what can the Government and the RBA do to prevent a bubble from forming?

Is Australian housing overpriced?

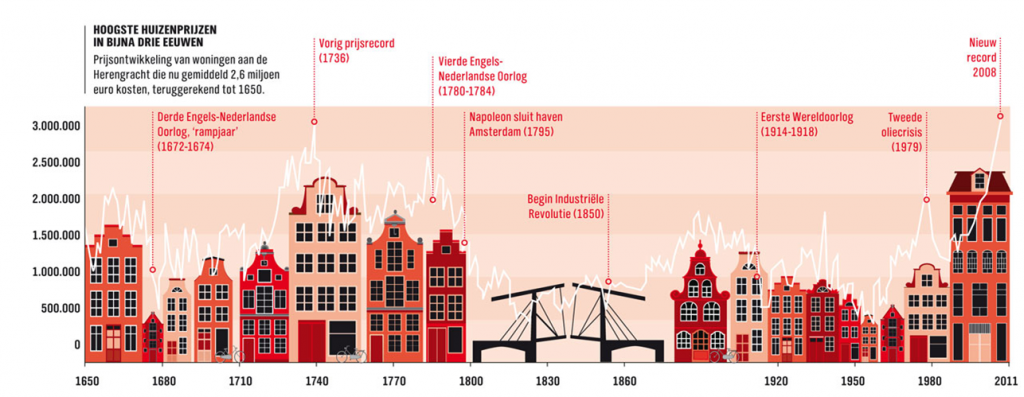

In short, yes. We believe that in the long run valuations of all asset classes mean revert. House price data exists in Holland dating back to 1650 (see chart below), demonstrating this mean reversion of residential house prices. It also shows that property bull and bear cycles can last an awful long time. For example, the market peaked in 1740 and didn’t start rising again until long after Napoleon had abandoned his attempts at world domination. A hundred year bear market? Ouch. The most recent housing bull market began in earnest in the 1960s and is now at stratospheric levels compared to the past. What goes up …

Source: Loanz of The Netherlands.

What about Australian residential property today? There are three good guides to understanding whether houses are cheap or expensive: how prices have changed over time relative to inflation; relative to wages; and relative to rents.

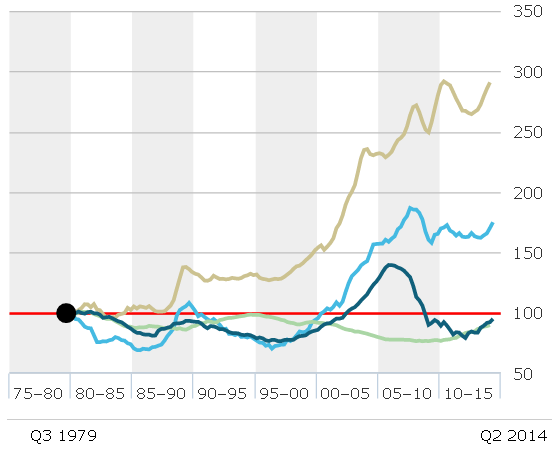

Here we review Australian home values (olive line) going back to 1979 against all three measures, and compare them to prices in the UK (light blue), the USA (dark blue) and Germany (green). The data is collected from The Economist’s excellent global house price online tool (Sources: Australian Bureau of Statistics; BIS; Bundesbank; FHFA; Nationwide; OECD; Office for National Statistics; Standard & Poor's; Thomson Reuters; vdpResearch).

i) First, how have prices changed relative to inflation?

Whilst houses in the US and Germany are cheaper than in 1979, Australian homes are almost three times as expensive when adjusted for inflation. Most of the price rise happened between 1995 and 2005.

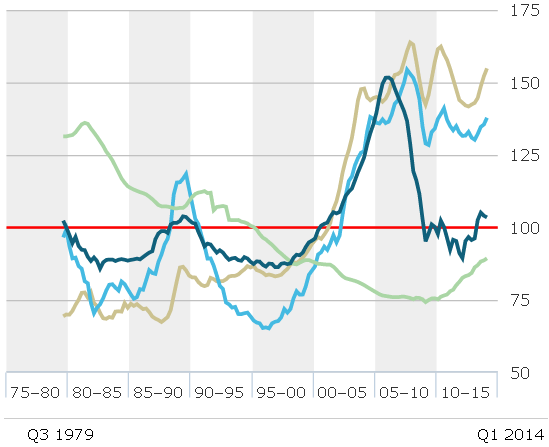

ii) What about house prices relative to the rents they produce?

Whilst your friendly local real estate agent might try to convince you that ‘there has never been a better time to buy’, he is not strictly correct. The olive line above supports the case that ‘there has never been a better time to rent!’ Houses in the UK, the US and Australia rose rapidly compared to rents between the period 1995-2005. American home prices then crashed and rental yields have since returned to their long term average. However, rental yields are more than 50% lower than their long term average in Australia. In contrast, German rental yields rose for 30 years (prices fell relative to rents) and only started to decline in 2010.

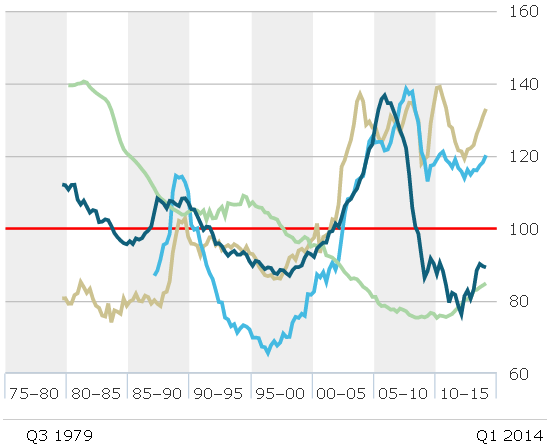

iii) And house prices relative to wages?

As the graph above shows, Australian house prices are about 30% above their long term average when compared to median wage income. This is our favoured long term measure of housing prices and the most significant of the three metrics.

So, yes, we can state the Australian residential home prices are high.

Why is housing so expensive?

In the long run, house values rise in line with incomes and standard of living (GDP). However, in the short term, there are two principal drivers of house prices; the availability of land, and the availability and price of credit.

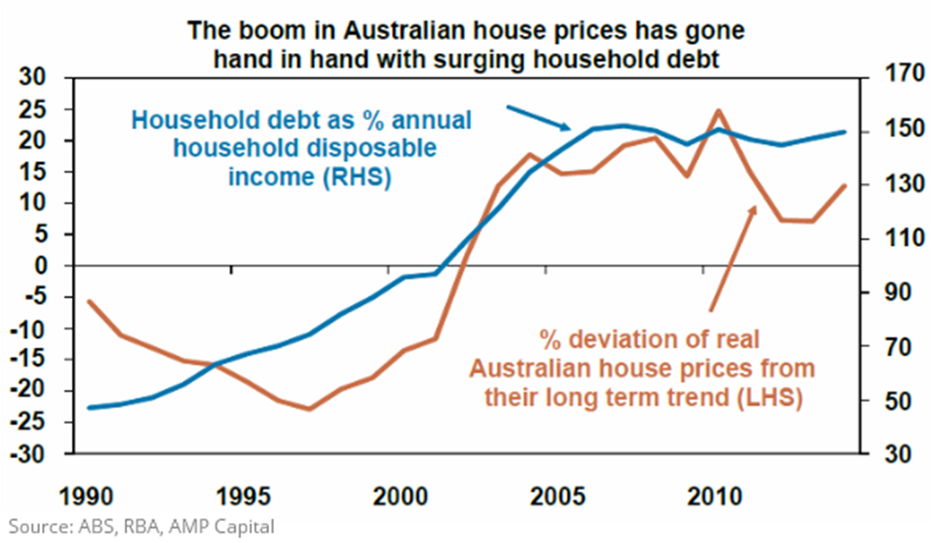

Lower mortgage rates enable Australians to borrow more for a given level of income. The shift to lower rates in the mid-1990s has exactly coincided with the sharp rise in prices and also with a massive increase in household debt (see below).

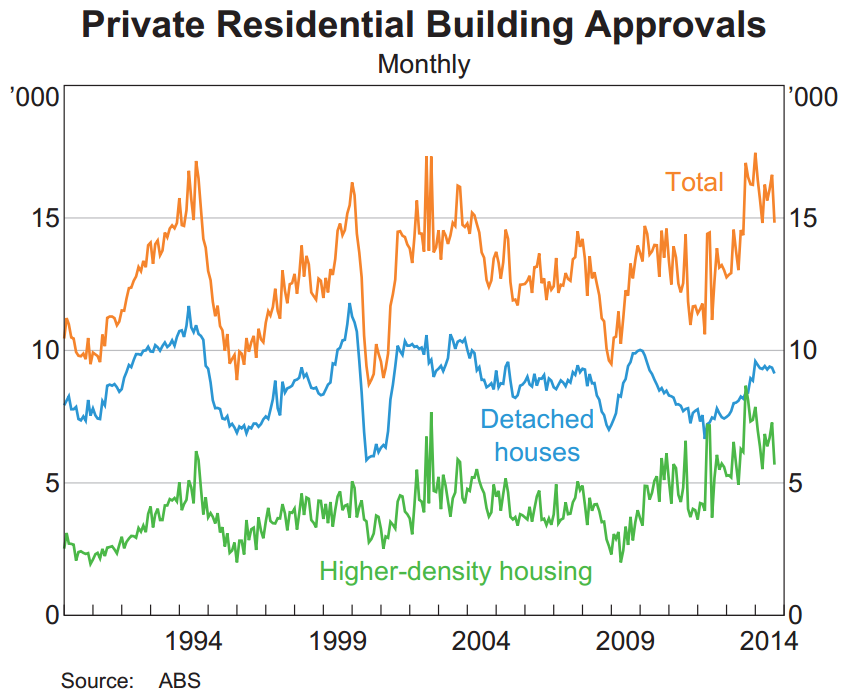

However, lower mortgage rates are only part of the story since low rates also exist in Germany and the US yet houses are much cheaper in both countries. What do the UK and Australian property markets have in common that have caused prices to remain so elevated? The answer is a lack of supply. Australia has restrictive land supply policies leading to an annual shortfall of some 200,000 houses. Very low vacancy levels and very high prices are the result.

A dearth of available housing can quickly become a glut as American homeowners in Florida and Nevada found to their horror in 2007, and Chinese apartment owners are now discovering. Here in Australia, higher home prices have resulted in a boom in building new homes. Will Melbourne be the new Las Vegas?

The media and populist politicians have also blamed Self-Managed Super Funds, negative gearing and that perennial whipping boy, foreigners. But these are mere sideshows.

What can the Government do to limit further price rises?

So far, the RBA has maintained that the residential housing market isn’t in a bubble and that house price growth has been sustainable. Significantly, the RBA has recently changed its stance stating that it is now worried about the build-up in speculative investment activity in the housing market, and that it has been in talks with the bank regulator, APRA, to introduce ‘speed limits’ on credit creation.

So what can the government and its twin regulators, the RBA and APRA do to limit house price rises? Here we examine their options, how effective they may be and whether they are likely to be introduced.

- The RBA can raise interest rates. A pre-emptive rate rise would seriously curb house price growth. But it would also damage confidence in the broader economy. We view this option as highly unlikely.

- The RBA introduces ‘macro-prudential’ measures specifically to target the housing market. For example, limits on loan-to-valuation ratios; limits on debt repayments to borrower income or loan size to income; forcing lenders to lift the interest rate buffer test they use for loan serviceability; placing high risk weights on particular types of loans in particular geographical areas; or forcing banks to reduce the number of loans to certain individuals and to certain geographical areas. This has been introduced in New Zealand with mixed results. We see this as more likely.

- APRA forces banks to lift their capital requirements – this is likely to emerge as part of the Financial System Inquiry. Given the increasing size of the banks’ residential mortgage books and their all-time low provisioning for bad and doubtful debts, they may not be adequately capitalised in a severe housing market downturn. In this instance, they will have to be bailed out by the taxpayer.

- APRA forces the banks to increase home loan risk weightings – extraordinarily, banks have been able to ‘self-assess’ the riskiness of each loan and assign to it their own risk weighting! Risk weights vary globally, but the global average is around 30% and is mandated by a regulator (ie. no self-assessment). The abolition of self-assessment will lead to lower share prices but more stable banks.

- Abolish negative gearing on property investment – and additionally remove the 50% capital gains tax discount for investment properties held longer than 12 months. Politically unpopular. Very unlikely to happen.

- Introduce a levy on foreign purchases of Australian residential property – press speculation is of a $1,500 levy on foreign buyers of Australian residential property, which would raise some $400 million. Whilst $1,500 is likely insufficient to curb foreign buying demand, a percentage levy based on the purchase price (ie. 3% or 5% of the purchase price) may do the trick whilst raising much needed funds for the Australian economy.

In conclusion

House prices are high. They are high because of a combination of low mortgage rates, a healthy banking system and a lack of supply (for now). The RBA is becoming increasingly nervous about excessive speculation and may act to limit further price rises. We expect much noise but little action.

In the long run, property has been an excellent wealth creation vehicle for Australians. Whilst returns haven’t quite matched equities (and the data is often of dubious quality as it invariably omits maintenance capex), they have been achieved with lower volatility. A diversified mix of property, bonds and shares has produced strong returns with reasonable volatility. The past, though, is no guarantee of the future. Whilst there will always be a place for property in investment portfolios, returns from this asset class are likely to be more subdued over the next 10 years.

Jonathan Hoyle is Chief Investment Officer at Stanford Brown. Any advice contained in this article is general advice only and does not take into consideration the reader’s personal circumstances.