For large superannuation funds and other investors with institutional-sized portfolios, a common practice is to spread the allocation to a particular asset class among a number of managers within a ‘multi-manager’ structure. This provides the well-known benefits of diversification not only across asset classes, but within key allocations like Australian equities and global equities. The aim of good manager selection is to construct an optimal style blend and beat the index, noting that no one style is likely to perform well in all market conditions.

Vital information missing when selecting managers

Manager research and selection is a specialist skill which requires a comparison of alternative managers across an array of attributes, especially performance ‘track record’. It is recognised that ‘past performance is no predictor of future performance’, so other attributes considered typically include each manager’s credentials and experience, fees, structures offered, technology, research pedigree, operational support and trading efficiency. Large superannuation funds will typically engage an asset consulting firm to assist them with manager research and may also subscribe to surveys and publications which report and rank manager performance.

But much attention is paid to performance track record, and the way that performance is measured and compared by funds and advisers is very important. Yet there is a vital piece of the picture missing. Superannuation funds, like most investors, are subject to tax on investment performance and what really matters is ‘what members and investors eat’ in the form of after-tax returns. In the ideal world, it would be reasonable to assume that manager performance is, as standard practice, measured and compared on an after-tax basis. Unfortunately, this assumption is wrong.

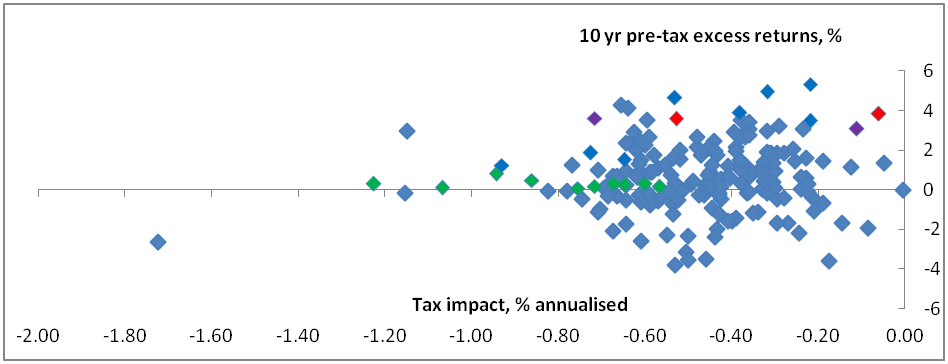

How does this misdirect superannuation funds and other investors? Let’s take a look at the 10 year excess returns (‘alpha’) of 198 U.S. mutual fund managers ending 31 December 2013 from the perspective of an Australian complying superannuation fund. We will explain the coloured data points later.

Source: Parametric (2015). Analysis is of Morningstar database of 198 mutual funds’ month end performance over the period 1 January 2004 – 31 December 2013. Benchmark return is iShares MSCI EAFE ETF month end performance over same period, unhedged. Performance is gross fees. Tax impact is calculated using the tax rates and rules applicable to Australian complying superannuation funds.

Any data points above 0% on the y-axis (plotted between -6% and 6%) denote funds which appear to have outperformed by generating returns in excess of the 4.84% per annum benchmark return we have used over a 10 year period. The data points high on the y-axis indicate the most outstanding strategies based on performance track record. The y-axis is typically the only kind of performance information considered when evaluating strategies and choosing between alternative managers.

Missing the tax impact

That approach misses a significant point. What is important to also consider is the x-axis which shows the tax cost of achieving the managers’ pre-tax excess returns. It is concerning to think that many institutional investors and advisors take a ‘one-dimensional view’. By fixating on the y-axis which focuses only on pre-tax performance, they do not consider the important dimension of tax (the x-axis) which can give these decision-makers a much more complete picture of each manager’s performance after taxes. A few forward-thinking institutions have the ability to focus solely on pre-tax manager returns, because they employ a sophisticated overlay approach to tax management (Centralised Portfolio Management), but most do not have that luxury.

Without using the ‘two-dimensional’ after-tax view of manager performance, it is hard to see that:

- strategies and managers that look very similar pre-tax can look very different on an after-tax basis – this is illustrated by comparing the two funds highlighted in red in the above chart

- strategies and managers that look like they are adding value can actually erode wealth on an after-tax basis – this is illustrated by the funds highlighted in green in the above chart

- a strategy or manager that looks superior to another strategy pre-tax can actually be inferior when compared after-tax – this is illustrated by comparing the two funds highlighted in purple in the above chart. The fund which generated an annual pre-tax excess return of 3.60% (compared to its competitor who returned 3.09%) in fact returned only 2.88% after-tax, less than the 2.98% after-tax return of its competitor.

The simplistic one-dimensional analysis of the performance histories of the complete set of funds shows that 132 of the 198 funds outperformed the broader market; that is, generated positive pre-tax ‘alpha’. This looks like good news. However, the two-dimensional analysis, factoring in tax, shows that only 99 (about half of the funds) actually added value above market. So, in fact, the news is not quite so good, and is certainly not good for a superannuation fund invested in one or more of the 33 managers whose performance looked healthy pre-tax but who did no better or actually worse than the market on an after-tax basis.

Analyse with tax profile in mind

This analysis should act as a cautionary message for superannuation funds and advisors engaging in the important task of choosing investment managers to achieve the right multi-manager and strategy mix. The message is to always check that performance is evaluated with the investor’s tax profile in mind and beware of traditional pre-tax analyses and their potential to mislead.

Raewyn Williams is Director of Research & After-Tax Solutions at Parametric, a US-based investment advisor. Parametric is exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 (Cth) (the “Act”) in respect of the provision of financial services to wholesale clients as defined in the Act and is regulated by the SEC under US laws, which may differ from Australian laws. This information is not intended for retail clients, as defined in the Act. Parametric is not a licensed tax agent or advisor in Australia and this does not represent tax advice. Additional information is available at www.parametricportfolio.com/au.