(Editor's introduction: Peter Thornhill is well-known to many of our readers, mainly for advocating a multi-decade investment strategy based on the long-term merits of industrial companies for income versus nearly every other asset class. For example, to show his consistency, some of his previous articles in Firstlinks are here and here and here. In this new piece, he again checks what he calls his 'mothership' chart, which shows the long-term return from industrial shares versus term deposits. It's his way of arguing that for investors with the right risk capacity and investment horizon, there's only one place to invest).

***

Well, it’s the time of year that I look forward to the most, the new year and the updates to my presentation material. It is also a welcome distraction from the mind-numbing boredom of lockdowns, travel bans, etc.

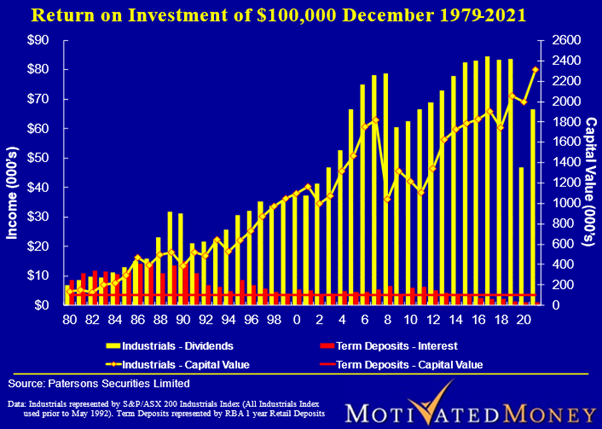

Below is my ‘Mothership’ comparison of industrial shares compared to cash over 40-odd years. The inevitable reduction in dividends in 2020 no doubt caused some concern but, as far as I’m concerned, it has been ‘same old - same old’. The chart below spells out the reduction in dividends, a slip in share prices and the inevitable recovery of both as life goes on.

I've always said ... history repeats

Although this chart covers a narrow timeframe, it provides a glimpse of history repeating itself. The 1987 correction stands out clearly and the reduction in dividends is similar in quantum to 2020. This is followed by the dotcom debacle in 2001-02, though whilst share prices fell dividends were not affected as much of the dotcom trash was never going to be dividend paying.

Next came the GFC in 2008-09 when indices halved. Our dividends were less affected as the problem was largely a US invention. I have included below an excerpt from an earlier newsletter as the situation today is eerily reminiscent.

“It will be apparent to most observers that during the last 30 years, any sign of a ‘crack’ in share markets has been met with a barrage of money from central banks. This behaviour became known as the ‘Greenspan Put’. The aim was to ensure that the delicate flower of capitalism known as ‘consumer confidence’ was never allowed to wilt.

As the public and institutions used more and more of this cheap money to fund property and other speculations, the government’s efforts were gradually perverted to ensure that property prices remained propped up; in fact, continued to rise. Rising property prices had become the sole support for consumer confidence and had to be fed at all costs.

This has naturally led to a global bubble in property followed by the inevitable faux handwringing by politicians claiming they are concerned about the housing affordability crisis. The bar to entry for ‘wannabee’ property owners was lowered to ground level; tax breaks were offered to property speculators (negative gearing) and cash incentives were offered by some governments to potential owners. The irony is that ‘dumb policy’ has exacerbated the very problem afflicting their constituents.

The seeds for the current debacle were sown some years ago but naturally no one paid any attention. Allow me to quote from an article written on 30 September 1999 (yes, 1999). Space precludes quoting the whole article.

“In a move that could help increase home ownership rates among minorities and low-income consumers, the Fannie Mae Corporation is easing credit requirements on loans that it will purchase from banks and other lenders. The action which will begin as a pilot program involving 24 banks in 15 markets- including the New York metropolitan region- will encourage those banks to extend home mortgages to those individuals whose credit is generally not good enough to qualify for conventional loans. Fannie Mae officials say they hope to make it a nationwide program by next spring”.

The rest is, as they say, history. Every opportunist opened a mortgage broking centre flogging loans to those who could not afford them and, eventually, some of them committed fraud.

Major Wall Street financial institutions created toxic derivatives and exported them around the world ensuring that the GFC, when it arose was truly global. With a guaranteed buyer of your toxic waste why wouldn’t you?”

Propping up residential property always backfires

I say reminiscent as an article in The Sydney Morning Herald on 12 February 2022 reports on the Government’s desire to help home buyers by taking a stake in the property with the would-be owners. This is in addition to grants, deposits of 2% and ludicrously low interest rates.

Continually throwing money at property is only going to make it worse, not solve the problem.

Anyone who has attended my presentations will be aware of my oft-repeated remark that history shows me that we never learn and just go on repeating the same dumb stunts over and over. The only saving grace is that business continues to flourish as it is core to the aspirations of the human race.

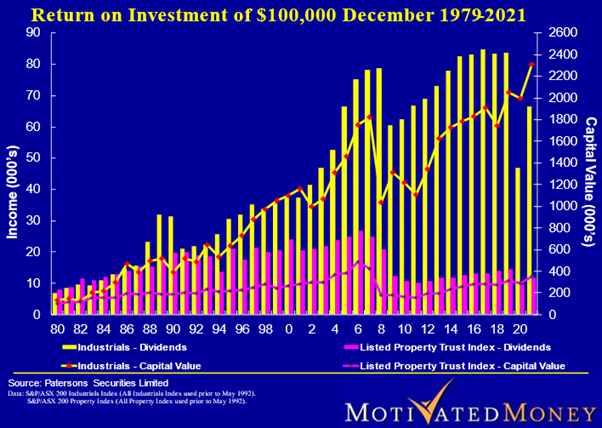

Let’s look at the property sector vs industrials. For newcomers, LPTs (Listed Property Trusts) are now called REITs or Real Estate Investment Trusts.

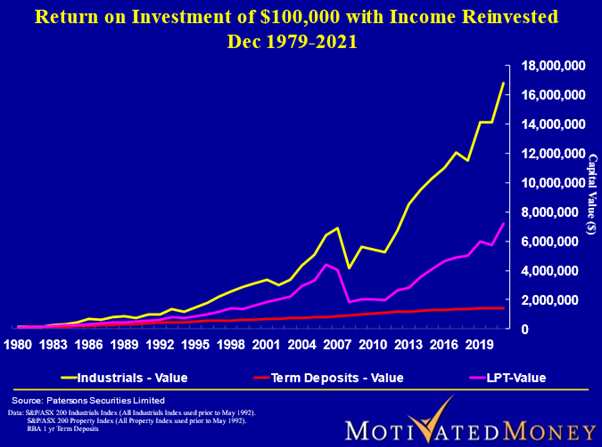

It still gives me pain to listen to the finance industry telling people to invest in ‘balanced’ portfolios to reduce risk. At no stage do they ever tell people the opportunity cost of this. I flatly refuse to add cash and property to my assets to drag the whole thing down, see the chart below.

If only we could provide education to increase financial literacy and enable people to make informed decisions regarding their financial future.

The fear associated with shares is fostered by focussing on volatility. Fear is based on ignorance and if we educate, I am confident that more people will make better quality decisions.

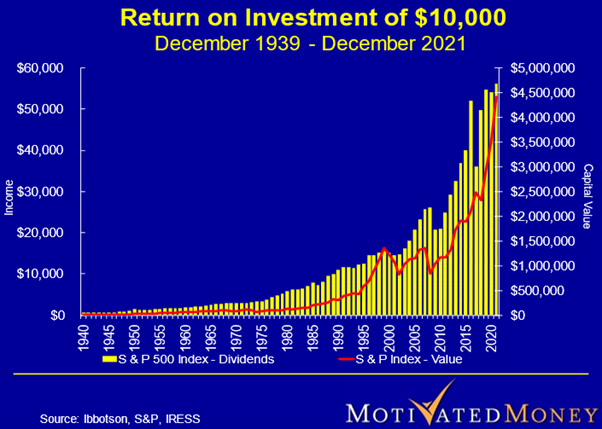

Let's go even further back

I am restricted in what I can demonstrate using Australian shares as the Industrials Index was only established in 1979. To reinforce the value of investing in the backbone of a nation - shares - consider the chart below.

This chart speaks to me: 80 years of US endeavour despite wars, pandemics of HIV aids 2005-12, flu 1968, Asian flu 1956-58 and so on to COVID-19.

I can reproduce a similar chart for virtually all the developed countries in the world. One example is a listed investment company in the UK that has flourished for over 160 years and has supported many families over that time.

Finally, I will be commencing full day courses again in the vain hope that not everyone is frozen with fear so watch this space.

Peter Thornhill is a financial commentator, author, public speaker and Principal of Motivated Money. He runs full-day courses explaining his approach to investing "in the vain hope that not everyone is frozen with fear".

This article is general in nature and does not constitute or convey specific or professional advice. Share markets can be volatile in the short term and investors holding a portfolio of shares will need to tolerate short-term losses and focus on a long-term horizon, and consider financial advice.