As we look across businesses exposed both negatively and positively to longer-term energy prices, we believe the risk of a prolonged energy shortage is not truly appreciated by markets. And this dislocation offers significant opportunities to investors willing to look at the whole picture.

Traditionally, high energy prices would trigger new investment in the sector creating increased supply that would bring prices back down. This conventional capital cycle in the energy sector typically takes five to 10 years to play out in full.

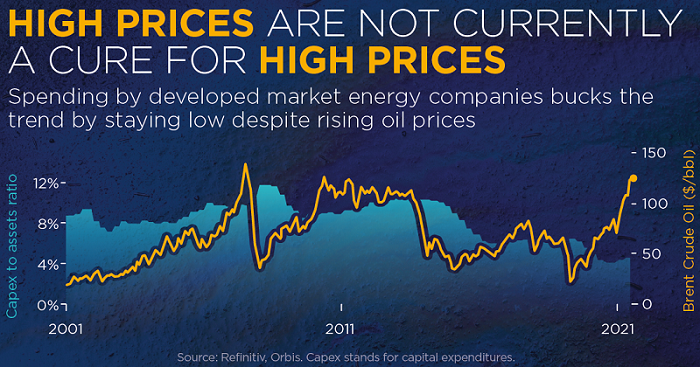

An extended cycle

Over the past six to eight years, however, there has been a noticeable lack of investment in the sector, as companies have either cut or not increased their capital expenditure.

The current underinvestment is the result of a number of factors.

1. In recent years investors have been more attracted to high growth companies, and as a result are valuing the future promise of cash as highly as having cash in their pocket today. This means they’ve tended to pour investment into startups that burn money to grow quickly, and drained capital from ‘old economy’ businesses – such as traditional oil and gas - that already make money but grow more slowly.

2. Increasingly urgent climate concerns have also been a headwind to traditional energy companies. The growing recognition that a clean energy transition is critical to our survival has clouded the demand outlook for new projects and the capital required to build them has become far less abundant and far more costly.

Together, these factors have created a longer and less efficient capital cycle in the energy sector that not only heightens the possibility of longer-lasting volatility and energy shortages but also presents opportunities to contrarian investors with a truly long-term mindset.

For while the fundamentals of these energy companies look better than they have in years, in our view they remain cheap. At current oil and gas prices, the sector offers an average free cash flow yield of around 20%. The challenge, however, is distinguishing the deservedly cheap from the attractively undervalued. A 20% free cash flow yield doesn’t count for much if a company has no future, and some energy companies probably don’t. But we believe some producers, like Shell, Inpex, and Chesapeake, as well as infrastructure companies like pipeline operator Kinder Morgan, will have a role to play for years to come.

Shell – relic or future leader?

Let’s take Shell as an example.

Most people see it as a fossil fuel company, but we see it more as a diversified energy business that is well-positioned to aid the energy transition. Shell has already committed to net-zero emissions by 2050 - a target that includes not only its own emissions but also the impact of the energy products it sells to customers.

A key part of this is Shell’s exposure to natural gas—a fuel that we see as key to facilitating the energy transition— but also through its renewables, its infrastructure and its petrol stations. In addition, it has a trading arm that matches energy supply and demand around the world, which could be increasingly valuable in a volatile and energy scarce environment.

On top of this, not only is it highly cash generative, but the nature of its business means it offers longer-term inflation protection and resilience against energy shocks.

Given all this, you might expect Shell to trade at a premium, especially in light of the concerns around energy security that are beginning to emerge in all corners of the global economy.

However, the market currently seems to be disregarding these issues. Shell, for example, is one of those with a double-digit free cash flow yield – a measure of how financially stable a company is – which is clearly attractive. This is demonstrated by the fact it is returning money to shareholders through share buybacks and a divided yield of around 4%, as well as earnings growth.

A bumpy ride?

Of course, there are always potential headwinds that we would be foolish not to consider. When investing in energy companies today, we are mindful about the risk of stranded assets. Particularly if the demand for oil declines sharply through recession, or from the world transitioning away from fossil fuels faster than we are expecting.

This would create uncertainty about the future and deliver a bumpy ride for investors.

The environmental, social and governance (ESG) risks associated with energy companies are also something that cannot be overlooked. While we believe Shell is responsibly running down its oil business, harvesting existing assets and investing in its transition and growth groups, which have much longer lives ahead of them, others may disagree and question our approach to responsible investing principles.

For the first time, the world is trying to optimise the global economy not just for efficiency, but also for emissions, and our challenge as responsible stewards of our clients’ capital is to understand how much of this energy transition is priced into current valuations.

Thinking differently

There are no easy answers to these issues, but ultimately, we would prefer to be an engaged shareholder of a company like Shell – holding them to account on their commitments – rather than divesting. If Shell, for example, disappeared tomorrow, demand for its products would remain and would be filled by a different producer. Potentially one that is a private or state-owned entity that is less transparent regarding ESG and climate issues such as emission reporting and targets.

Equally, there are potential economic and political headwinds that could affect some parts of the energy sector. High energy prices have resulted in bumper profits for many energy companies – Shell included – that have caught the eye of governments looking to introduce so-called ‘windfall taxes’.

The impact of these policies is still uncertain, as different jurisdictions have different approaches, but with the cost-of-living crisis unlikely to abate any time soon, this is not an area that should be ignored.

That said, even after considering these potential risks we think certain critical energy infrastructure holdings such as Shell, Sunrun (solar), Vestas Wind Systems (wind), Constellation Energy (nuclear) and Kinder Morgan (gas pipelines), among others, are in a good position - with higher margins, better capital discipline and lower debt. They are also in a cycle of harvesting healthy oil/gas prices while returning capital to investors.

We believe that is a recipe for attractive potential returns, and a good example of how our contrarian bottom-up approach can identify inefficiencies and dislocations in the market to spot interesting opportunities.

Shane Woldendorp, Investment Specialist, Orbis Investments, a sponsor of Firstlinks. This report contains general information only and not personal financial or investment advice. It does not take into account the specific investment objectives, financial situation or individual needs of any particular person.

For more articles and papers from Orbis, please click here.