Negative gearing did not die on Budget night. It was placed in quarantine, which sounds gentler, right up until the arithmetic is done. Since 12 May, commentary has split into two camps: one declaring residential property investment dead, the other insisting nothing has changed because existing holdings are grandfathered and new builds are exempt. Both camps are wrong, for the same reason. Neither has calculated what quarantining a loss costs. This article does the sums, and the answer for a typical investor is roughly a quarter of the tax benefit.

A caveat first: none of this is law yet. The measures were announced in the 2026-27 Budget to start on 1 July 2027, and bills change between announcement and assent. But the grandfathering line was drawn at 7:30pm on Budget night, so anyone buying today is already living under the proposed rules.

What 'quarantined' actually means

From 1 July 2027, negative gearing for residential property will be limited to new builds. Investors who buy a newly constructed dwelling can keep deducting net rental losses against salary, exactly as now. Investors who buy an established dwelling after Budget night cannot.

Here is the part the headlines skipped: those losses are not denied. The ATO's summary confirms they can still be offset against other residential property income, including capital gains, with any excess carried forward indefinitely. Interest, rates, insurance and agent fees all remain deductible. What changes is when the deduction arrives and what it lands against. The deduction is deferred, not denied: the tax equivalent of 'the cheque is in the mail', except this mail can take a decade.

The change applies to individuals, companies and most trusts, but not superannuation funds (including SMSFs) or widely held trusts. Commercial property and geared share portfolios are untouched.

The $9,000 haircut: a worked example

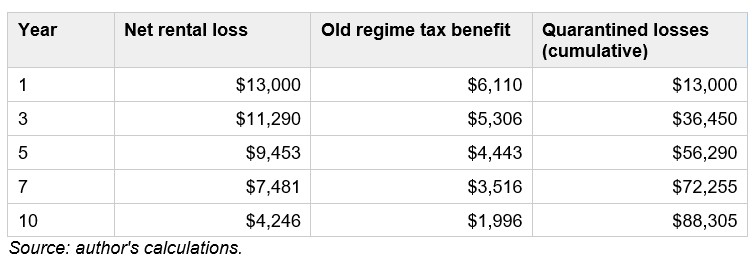

Consider an investor on the top marginal rate (47% including Medicare levy) who buys an established unit for $750,000 with a $600,000 interest-only loan at 6%. Rent starts at $30,000, a 4% gross yield, growing at 3.5% a year. Cash expenses of $7,000 grow at 3%. The hold is 10 years.

Year one produces a $13,000 net rental loss. Under the old rules, that returns $6,110 in tax immediately. Under the new rules, it returns nothing. Yet.

Notice what the 'nothing has changed' camp misses. On an ordinary interest-only structure at current rates, this property never turns cash-positive within the decade. All $88,305 of losses ride along to the sale, where they offset the capital gain. Under the new CGT settings, that gain is taxed at the investor's marginal rate; the headline 30% is a floor, not the rate, and it bites only when that marginal rate would fall below it. For a top-rate investor the gain is taxed at 47%, so the loss bank returns roughly $41,500. Once. In year 10.

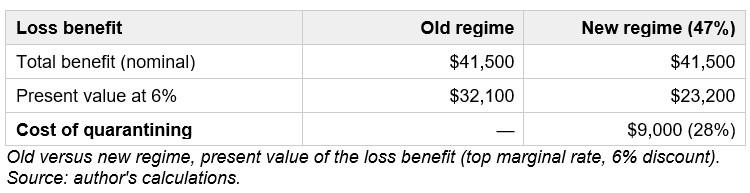

Discounting both streams at 6%, the old regime's annual refunds are worth about $32,100 today, while the new regime's single deferred offset is worth about $23,200. The cost of quarantining is roughly $9,000, or 28% of the tax benefit, even though no deduction was ever formally denied. The ATO is not confiscating deductions; it is running a cloakroom with no fixed closing time.

The damage is almost entirely time value. The same $41,500 of relief eventually arrives, but a lump in year 10 is worth far less than refunds collected along the way, and the investor funds the shortfall from after-tax salary in the meantime. Note what does not change: because the gain is taxed at the same 47% the losses would have been deducted at, there is no rate penalty here, only a timing one. A rate penalty appears only for an investor who sells on a lower marginal rate than they earned while holding, the retiree who disposes after their income has fallen, where the 30% floor could come into play. Under the old regime, maximum leverage maximised the tax benefit. Under the new one, heavy leverage on a low-yield established dwelling maximises the deferral penalty.

The carve-outs do the steering

This is less a revenue measure than a traffic system, and every exemption points capital somewhere. New builds keep full gearing, and their buyers can even choose at sale between the old 50% discount and the new indexation, a rare case of the tax system offering a genuine choice that does not require a private ruling. Commercial property and shares keep immediate deductibility, improving their relative appeal. And SMSFs sit outside the quarantine entirely, which mechanically improves residential property's standing inside super. Steering geared property into super was presumably not the plan, but tax incentives are like water: they find the cracks.

Lessons from 1985 (and Wellington)

Australia quarantined negative gearing once before, between July 1985 and September 1987. Folklore blames the experiment for Sydney rent spikes; the data is murkier, with rents rising in some cities, falling in others, and interest rates in the teens muddying everything. Both sides have now been citing the same two years of data for four decades, which must be some kind of productivity record. New Zealand offers a cleaner test: it ring-fenced rental losses in 2019 and the ring-fence survives today, through a change of government. Property investment across the Tasman did not end; it repriced. Grattan Institute modelling suggests prices 1% to 2% lower than they would otherwise be, while industry modelling warns of materially fewer housing starts. Hold all of these numbers loosely.

What investors should do now

Existing holders are grandfathered, and their main risk is legislative drift while the bill passes. Selling and rebuying now carries a hidden cost, because the replacement asset enters the new regime. Prospective buyers face a sharper fork: a new build keeps immediate deductibility, while an established dwelling carries the quarantine cost above, which belongs in the offer price. SMSF trustees should re-run their comparisons rather than rush, since a tax wedge is a poor sole basis for an asset allocation. And anyone with a negatively geared plan needs fresh cash flow modelling, because the refund that used to co-fund the shortfall now arrives at the end, not along the way.

Quarantining changes the timing and destination of tax benefits. In leveraged investing, timing and destination are most of the game. The example investor loses no deduction on paper and roughly a quarter of its value in practice. It is a repricing of property investment, and the best-placed investors will be the ones who did the present-value arithmetic before the market did.

Trevor Schmid has more than 20 years’ experience across superannuation, financial advice and member education. This article is general information only and does not consider any individual’s objectives, financial situation or needs.