When Malcolm Turnbull addressed the National Press Club last week, I was really hoping he would announce a major policy addressing Australia’s ongoing housing affordability woes. Sadly, little was offered. He laid the blame at the states and territories which simply confirmed that little will happen to this space.

Possibility of a change in negative gearing rules

We can now expect political huffing and puffing until November 2019 when Australia must endure the next election. There is a strong possibility that we will see a changing of the guard, after which negative gearing laws will be amended, probably coinciding with a major property downturn. On that basis, the game plan for the next two and a half years is predictable. Property investors will go-hard simply because they want to get in before the negative gearing rules change.

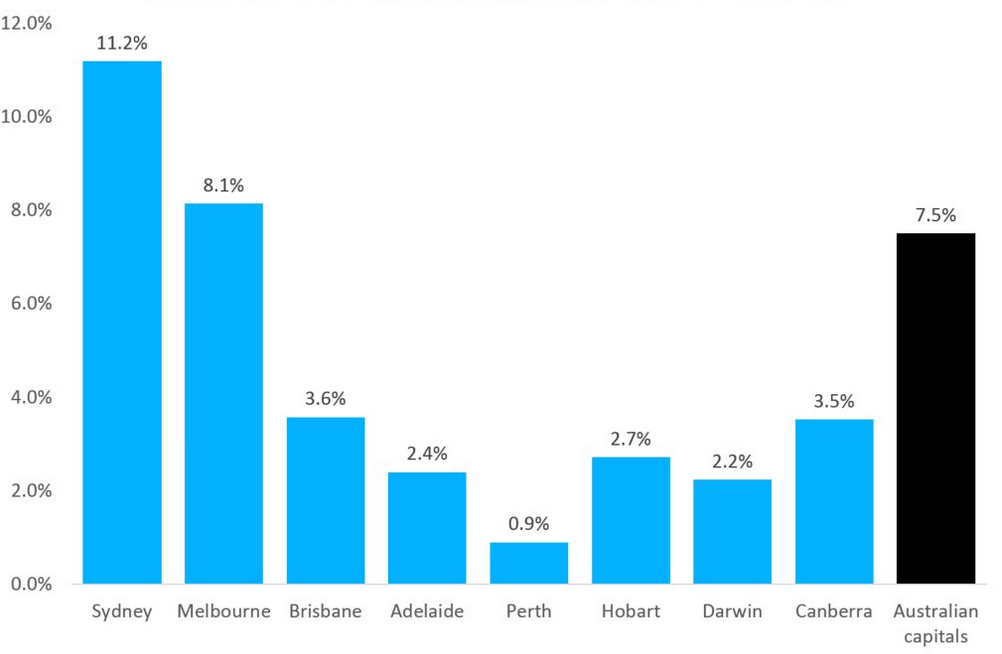

There is little doubt that property prices will continue to rise in 2017 to the extent that we may see cumulative house prices reach 100% gains over five years in some areas. The latest statistics from CoreLogic to January 2017 showed Melbourne up 11.8% in the last year and Sydney continues to run amok at 16%. Since June 2012, the cumulative increase in house prices has been 70.5%, CoreLogic reported.

Compound annual change in dwelling values, 5 years to January 2017

Source: CoreLogic

Other potential policy responses

Two announcements I was expecting were on immigration and reducing the off-the-plan ratios to overseas buyers. CBA Senior Economist Michael Workman said,

“Housing affordability is set to worsen without federal action. The Federal Government controls some of the significant demand factors for housing markets, namely population growth via migration and the spectrum of tax and foreign investment policies that significantly inflate demand for existing and new housing. Housing affordability can be improved, via stabilising growth in house prices and rents, by gradual reforms to both supply and demand issues.”

In the present property environment, there is no need for off-the-plan sales to foreign buyers to remain at 100% and this ratio is controlled by the Federal Government.

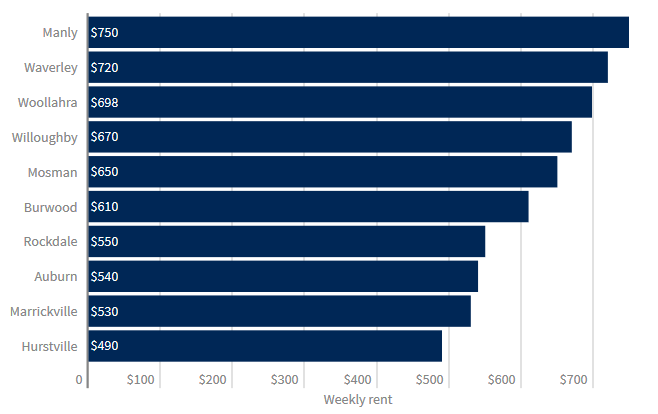

Despite the construction of thousands of new apartments, we are not seeing an easing of rents as was expected. Data analysis from the NSW Rental Bond Board identified more tenants than ever. No surprises that the most expensive five suburbs are Manly, Waverley, Woollahra, Willoughby and Mosman. We can therefore expect to see these areas hot-spotting with investors to achieve the best rental returns as well as capital appreciation. Investors will keep driving these markets simply because the Federal Government has tinkered with superannuation, and property markets are out-performing the share market.

Of course, we all know that this will change over time although the momentum is strong with our respective governments doing absolutely nothing aside from weekly lip service.

Top ten weekly rents for a median 2-bedroom flat

Source: Housing NSW, tenants.org.au/tu/rent-tracker

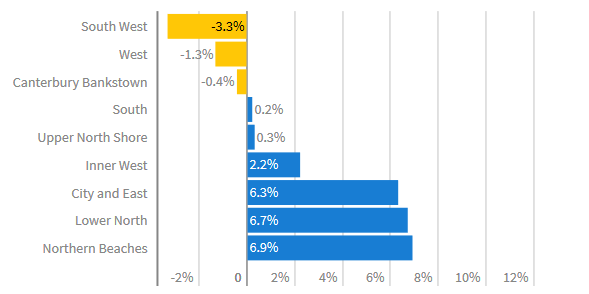

Sydney’s apartments: How prices fared over last 6 months

Source: Domain Group House Price Report, December 2016 data

AUSTRAC and ATO asking direct questions

Much has been written about money laundering within the Australian property markets. The appointed watchdog, the Australian Transaction Reports and Analysis Centre (AUSTRAC), is investigating more than $3 billion in suspicious transfers from Chinese property investors last year. This was further backed-up late last year when the major Australian lenders ceased lending to foreign buyers. I was surprised to read last week that foreign investors are again rising but this time, they are paying cash to settle the full amount of the purchase.

Many will ask the obvious questions as to where all these monies are originating, based on recent announcements that the Chinese Government had shut down money transfers from China.

Well, allow me to lay your concerns to rest. The smartest thing Joe Hockey did when he was Treasurer was to hand all data collection on every property transfer in Australia to the Australian Taxation Office (ATO). Some months later, after reviewing the data, an excited ATO announced they were expanding their forensic property investigations back to 1985.

Just last week, I received a telephone call from an ATO investigator requesting purchaser contact information for a property we sold late last year. Nothing was said to justify the request. I simply provided the relevant information.

What this clearly tells us, is that every property transaction is scrutineered by the ATO and it should not be possible to beat the system.

With so many discussions on housing affordability, this development should please all those closely following real estate movements. As each property settles, the data is then sent to the ATO for recording and investigation.

Everybody buying Australian real estate should know that each transaction is noted and investigated. And yes, they have the resources.

Robert Simeon is a Director of Richardson and Wrench in Sydney’s Mosman and Neutral Bay and has been selling residential real estate in Sydney since 1985. He has been writing the real estate blog Virtual Realty News since 2000.