Australia’s commercial real estate sector exhibited a recovery through 2025, with property values stabilising and returns moving into positive territory. As we enter 2026, this momentum is expected to continue, supported by strong fundamentals across all core commercial real estate sectors.

Commercial real estate continues to demonstrate compelling risk-adjusted returns, underpinned by a combination of resilient tenant demand, a constrained forward-looking supply pipeline, accelerating rental growth, and high-quality cashflows at property yields that are generally higher than historical averages.

This recovery follows the largest repricing in the Australian commercial real estate sector in approximately 35 years, providing an attractive entry point for investors. Current valuations and earnings multiples for high-quality institutional assets are favourable relative to other asset classes that are now trading at multi-decade highs.

Market conditions and positioning for investors

The comparative outlook for commercial real estate against other investment classes will likely support increased investor demand and capital allocations towards the sector. The pricing of all global financial asset classes have faced increased scrutiny, most recently Software as a Service (SaaS) entities, amid continued volatility and speculation on future interest rate movements and the impact of AI. As markets reassess the investment outlook and challenge traditional certainties, conditions across Australia’s commercial real estate sector have continued to strengthen, offering protection from periodic volatility.

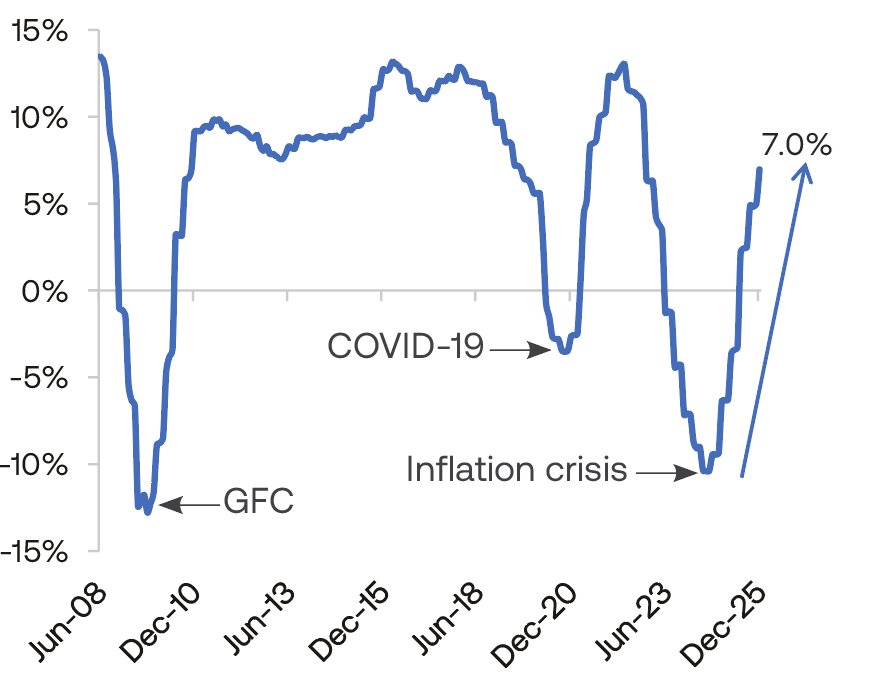

In this environment, the sector is positioned to benefit from defensive and resilient income streams supported by embedded rental escalations. Following a period of valuation adjustment, the forward-looking return profile for commercial real estate has become more compelling when compared with previous cycles (see Figure 1). The current entry point is more affordable when compared to valuations for listed equities (both domestic and international), infrastructure and many renewable strategies. This landscape is conducive to the relative outperformance of commercial real estate and has supported an increase in capital inflows during calendar year 2025.

Figure 1: Annual returns (%)1 (MSCI Core Wholesale Funds)

Supportive economic conditions

The commercial real estate sector has continued to benefit from a strengthening economic backdrop and renewed confidence in underlying real estate fundamentals. The unwinding of restrictive policy, despite the recent RBA cash rate increase, has strengthened household and corporate balance sheets. Economic growth and household consumption activity have reached their fastest pace since 2023. Given this momentum, Australia’s economic growth projection for 2026 leads advanced economies globally. Importantly, Australia’s economic GDP, population and employment forecasts are between two to four times higher than the G12 average.2

Beyond cyclical recovery, the sector is entering a structural undersupply phase. Development feasibility remains constrained by elevated construction costs and planning delays, supporting expectations for above-trend rental growth over a prolonged period.

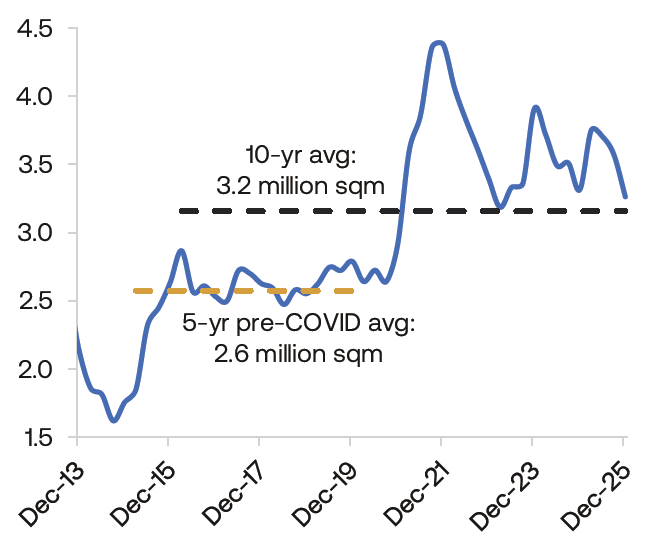

Key real estate indicators are reflecting this momentum. Prime office leasing activity and rental growth over the past year reached the highest levels since 2018. The growth in prime CBD net leased space was 47% above the 10-year average. Similarly, Industrial & Logistics (I&L) leasing volumes are trending at a rate 27% higher compared to pre-COVID levels (see Figure 2) with momentum across the economy and retail spending continuing to support demand. Retail vacancy rates have continued their downward trajectory since peaking in June 2022, with Neighbourhood and CBD prime retail now at their lowest vacancy levels since the onset of the pandemic.

Figure 2: Industrial & Logistics - Gross leasing volumes (12-month rolling million sqm)3

Supply shortfall is happening across the board

Supply remains constrained across the commercial real estate sector, with fewer building completions in 2025 compared with historical averages. Higher construction costs (including labour, materials and land) together with planning approval delays continue to limit new development across all property sectors.

This supply constraint represents a clear inflection from mid-2022 conditions and underpins a market increasingly supportive of income returns. In CY25, completions across the Retail and Office sectors fell to their lowest levels since the early 1990s. Across the I&L sector, groups with scale, development capability and access to high-quality land holdings retain a competitive advantage in this environment.

Looking ahead, retail and office space is forecast to reach historically low levels of new supply in the coming years. The labour-intensive nature and long lead times of office development provide clear visibility over future supply, with pipelines indicating a meaningful decline in new property completions through to 2030. In the I&L sector, construction costs have eased from record highs due to projects requiring less labour. However, access to these reduced delivery costs varies by location, land quality, scale and development capabilities. Future I&L supply will largely depend on the availability of zoned land and supporting enabling infrastructure (water, power and roads), and the need for 10-25% rental growth nationally to encourage more construction.

Accelerated tenant demand driving rents – even in the office sector!

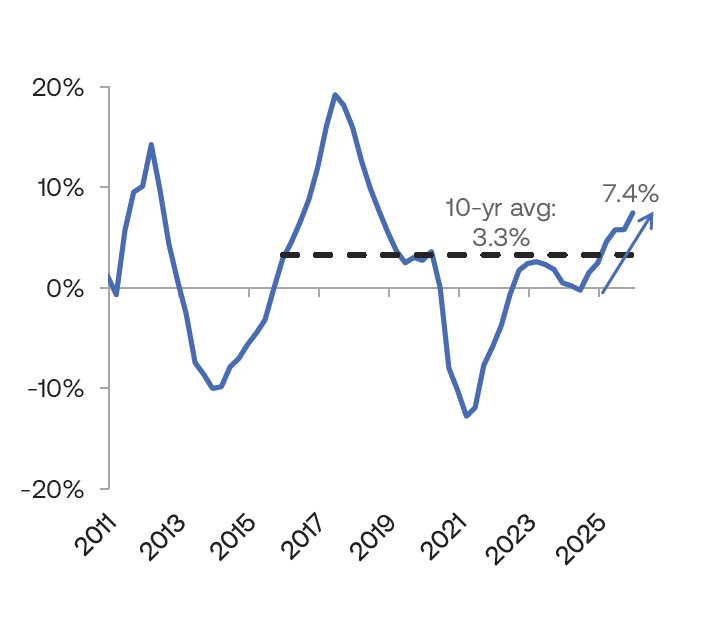

Restrictive supply and strong tenant demand have driven accelerated rental growth. Prime office rents have increased at the fastest pace since 2018, and eastern seaboard markets recorded above double-digit growth over the past year. National prime CBD office effective rents grew +7.4% over the past year, well above the 10- year annual average of 3.3%4 (see Figure 3).

Retail specialty rents are at their highest levels since 2010, supported by limited new supply. In the I&L sector, rents have also held firm despite higher levels of new completions in recent years. Looking ahead, the combination of declining supply forecasts, structural demand drivers, and strong leasing activity should continue to support income growth across each core property sector.

Figure 3: Office - National prime CBD effective rental growth (rolling annual)4

Investment demand is increasing

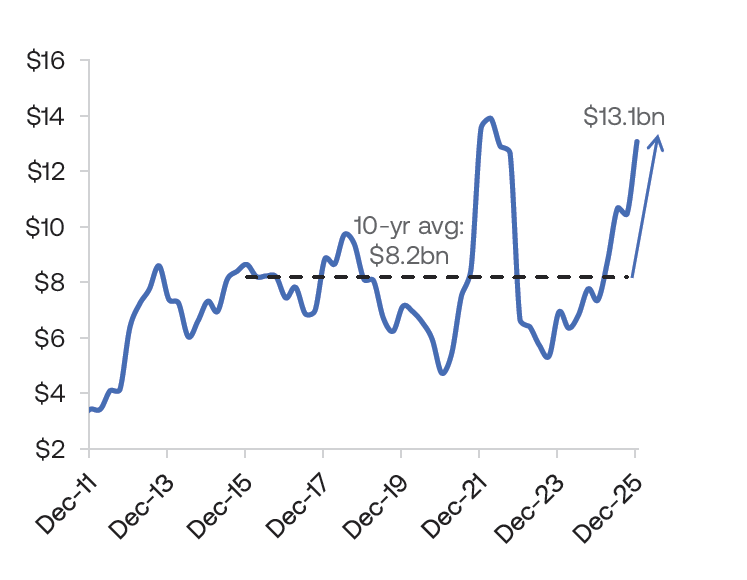

Against a backdrop of stabilising capitalisation rates and increasing market rents, indicative prime market values and returns have advanced into the next expansionary cycle. Rising transaction evidence and investor demand continue to support stabilisation, or compression, of core capitalisation rates. Quarterly investment volumes reached their highest levels since 4Q21 during 4Q25, totalling $11.7 billion across the core commercial real estate sectors. This result has been driven by investor appetite for retail property (see Figure 4) and an increase in office transactions.

The next investment paradigm is expected to be defined by income-led growth, where durable cash flows and earnings delivery, rather than multiple expansion, are the primary drivers of returns. In this context, Australian commercial real estate offers predictable income for investors.

Figure 4: Retail - Transaction volumes ($ billions, rolling annual)4

Dispersed outlook

Headline figures continue to mask the divergent nature of the property recovery. As volatility and global themes unfold, capital allocations will increasingly target assets defined by cashflow resilience and the ability to generate income growth. This has been evidenced by the investor demand and valuation premiums for these types of assets. This early stage of recovery presents opportunities for value creation that are unlikely to be available later in the property cycle.

As we enter 2026, the outlook for valuation growth has become increasingly divergent between financial and tangible asset classes. Underlying fundamentals across Australia’s commercial real estate markets remain supportive, reinforcing the expectation that the sector will continue to outperform.

The path of future interest rates, both within Australia and throughout the world's leading economies, will be debated; however, the gap between property yields (capitalisation and discount rates) and bond yields is high compared to historical averages. This is despite the recent RBA February 0.25% interest rate increase. The volatility across many ‘liquid’ asset classes highlights the appeal of risk-adjusted returns in unlisted commercial real estate.

Source: C&W Research, Charter Hall Research, Economist Consensus, JLL Research, MSCI Core Wholesale Monthly Index, Oxford Economics.

1MSCI Core Monthly Wholesale Fund Index (Dec-25).

2Oxford Economics, Nov-25.

3Source: JLL (4Q25), Charter Hall Research.

4JLL (4Q25), Charter Hall Research.

Steven Bennett is Chief Executive of Direct Property and Sasanka Liyanage is Head of Research at Charter Hall Group, a sponsor of Firstlinks. This article is for general information purposes only and does not consider the circumstances of any person, and investors should take professional investment advice before acting.

For more articles and papers from Charter Hall, please click here.