The Weekend Edition includes a market update plus Morningstar adds links to two highlights from the week.

Weekend market update

On Friday in the US, markets pulled back after a strong week with the S&P500 dropping 0.9% and the NASDAQ down 1.9%.

From AAP Netdesk: The local share market has finished a strong week on a quiet note ahead of next week's key inflation readout. The benchmark S&P/ASX200 index closed on Friday basically flat at 6,791, but thanks to strong gains on Monday and Wednesday, the index finished the week up 2.8%, its best in 19 weeks.

Tech was the best-performing sector for the week, up 7.1%, but the financial sector's 4.4% rise had a bigger impact on the index. All big four retail banks were up again on Friday, with ANZ climbing 3% to $22.59 on the back of apparent enthusiasm about its acquistion of Suncorp's banking arm. NAB added 0.7%, Westpac advanced 1.1% and CBA gained 2%. Macquarie fell 0.4%. IAG fell 1.4% after the insurance giant said old silicosis exposure claims were impacting its bottom line.

Travel companies were under pressure after US airlines United, Delta and American recently reported poorer-than-expected earnings. Qantas fell 2.0%, Flight Centre dropped 3% Corporate Travel Limited lost 4.1%. The energy sector was worst performer for a second day, falling 1.2%. In the heavyweight mining sector, BHP edged lower but Rio Tinto added 0.5%. Platypus Shoes, Hype DC and The Athlete's Foot owner Accent Group fell 11.6% after reporting sales across May and June continued to be subdued.

***

"Glory days, yeah they'll pass you by

Glory days, in the wink of a young girl's eye

Glory days, glory days

Think I'm going down to the well tonight

And I'm going to drink 'til I get my fill

And I hope when I get old I don't sit around thinking about it

But I probably will

Yeah, just sitting back trying to recapture

A little of the glory of, well time slips away

And leaves you with nothing mister but

Boring stories of glory days"

Excerpt from Glory Days, by Bruce Springsteen

Fund manager reports for last financial year are drifting into client mailboxes, and the glory days have passed by many of the portfolios. With markets taking a major downward turn in 2022, the managers who missed the change are delivering disappointing results, often worse than expected. Bond investors will be shocked to see supposedly defensive funds down 10%, while global equity index funds have lost 20% in calendar 2022. In a sector such as US small company growth funds, some losses range from 40% to as high as 70%.

Investor reaction will vary and depend on the entry point and understanding of the manager. A common feature of funds with the worst 2022 was a strong 2021. Despite believing that many of their stocks were in bubble territory, often wildly overvalued, some managers held on to their winners too long. They thought they should let their growth stocks run due to a fear of missing the last drinks at the bar, but they should have left the party earlier.

Even in passive land, the results are sobering. For example, here is the performance of two global index ETFs from Vanguard, the MSCI International (ASX:VGS) and the MSCI International Small Companies (ASX:VISM). One is down 15% and the other 20%. Some active fund managers are down 20% or more than these indexes in the latest reporting period.

Source: Morningstar

What are the explanations? Here is one of the more honest and open from Steve Johnson of Forager. In FY21, Forager's two funds returned an exceptional 79% (global) and 87% (Australian). Then in FY22, losses were 38% and 28% respectively. Over two years, most clients are probably happy, but not if success encouraged investment in June 2021. Johnson is upfront:

"In our International Fund, we took baby steps when giant steps were required ... We were aware of and vocal about a bubble in growth stocks. I wrote a CIO letter in our December 2020 Quarterly Report warning about the risks of higher inflation. We sold half our position in some stocks that were beneficiaries, three-quarters of our stakes in others ... But the returns have still been terrible. The remaining investments in the winners of 2021 tumbled, some more than 70% ... Paraphrasing Warren Buffett, predicting rain doesn’t count if you don’t build arks as well. Our portfolio changes were meaningful but they needed to be dramatic. Patience is usually a virtue but there are times when urgency is called for. The 2022 financial year was one of them."

Such actions explain many of the results. Scott Berg of T Rowe Price told a Sydney audience this week that he knew the market was in a bubble, driven by free money in 2020 and well into 2021. He made some portfolio adjustments, but in late 2021, just as conditions looked better, two events hit. One was the new Omicron variants, especially in China, and the second was the Ukraine war and its impact on commodities. And so his portfolio in 2022 gave back much of the gains made in the two prior years.

Tony Lewis of EGP Partners explained the late 2021 change this way:

"In October 2021, the fund for a period of a few days was handsomely outperforming our index for the financial year. Our largest holdings were all executing well on their strategies and the market was awarding them pricing that (especially in hindsight) placed a high valuation on these prospects. Since that point in October, despite generally continuing good fundamental performance from most of our major holdings, there has been a massive reversal in the valuation the market ascribes to their prospects."

The most dramatic turnaround is probably in the Frazis fund, up 93% in FY21 and down 71% in FY22. Michael Frazis was interviewed by The Australian Financial Review in January 2021 after his success in 2020. The AFR said:

"He barely pays attention to traditional valuation metrics such as price-to-earnings ratios, in part because the companies he likes to buy normally don’t have any earnings."

Then Frazis is quoted directly:

“We’ll tend to be gone by the time the profits come through. We want our companies spending and growing – hiring staff, opening new locations, putting money back into the community, spending on R&D. That’s the perfect profile for me. As the companies mature, that’s when they become profitable and the growth slows down, that’s when we exit. We want companies investing heavily in doing really great things. That's how I look at profitability, which is different, right? It's different to most people."

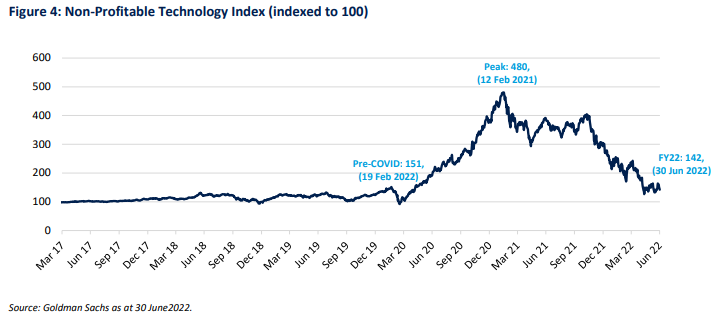

The timing of the interview must have seemed ideal in January 2021 on top of the stellar results. The Goldman Sachs' 'Non-Profitable Tech Index' peaked on 12 February 2021 at 480 and was down to 142 by 30 June 2022, off 70% in 18 months.

For anyone thinking this is all hindsight, the following was also written in January 2021, the same month as the Frazis interview, by Anthony Aboud of Perpetual, who admitted it "vents some of our frustrations" at missing the party:

“Right now, market participants are basing their investment decisions on how articulate a CEO is, whether or not a company fits the narrative of the day, the long term total addressable market (TAM) and how many times a CEO says the words AI or network effect on their conference call. At some point, the market environment will change, and focus will swing back to companies making sustainable cashflow. When that happens, we will see a lot of these hyped-up tech names fall 90+%.”

And 18 months later, that has played out. For what it's worth, on 9 December 2021, I went against my usual preference to not predict stockmarkets by saying I was reducing my personal exposure in anticipation of a decent fall.

Those who invested at the end of 2021 based on promotional material that boasted of 'protecting capital' and 'deep research' have a right to feel disheartened. Some manager reports are blaming the 'market' for misunderstanding the amazing growth opportunities, but there was too much hubris over 2021 as markets recovered from the pandemic. Was there a belief that inflation and interest rates were low forever, that central banks would come to the rescue and it did not matter if company profits were too far into the future? Risks were building at the end of 2021 and into 2022 yet too many stayed invested in companies while their circumstances changed.

Jeff Ptak, Chief Ratings Officer for Morningstar examined the performance of domestic US equity funds to the end of May 2022 and concluded:

"I would say active managers are prone to exaggerating about their prowess during down markets. It’s usually not as good as they say, not as persistent as they say, and not as important to their long-term success as they would lead you to believe.”

Amid the pessimism, we are experiencing a strong 'bear market rally' at the moment. The recent Bank of America fund manager survey showed a 'dire level of investor pessimism'. When the market capitulates, that is a signal to many that we are near the bottom. Cash allocations are at their highest for a decade, showing plenty of dry powder. Many professionals are asking if we are at the start of a new period of Glory Days.

Once again, Charlie Munger, Vice Chairman of Berkshire Hathaway, was on the money at the 2021 Annual General Meeting.

“If you are not a little confused by what's going on, you don't understand it.”

***

Has there ever been more general public interest in inflation? It's even reached the unusual point where the Prime Minister, Anthony Albanese, has warned the Reserve Bank against “overreach”. The Reserve Bank's change of tune over a few months is extreme, as the minutes of the June meeting showed this week:

“The level of interest rates was still very low for an economy with a tight labour market and facing a period of higher inflation. Members viewed it as important that inflation expectations remained well anchored and that the period of higher inflation be temporary. Members agreed that further steps would need to be taken to normalise monetary conditions in Australia over the months ahead.”

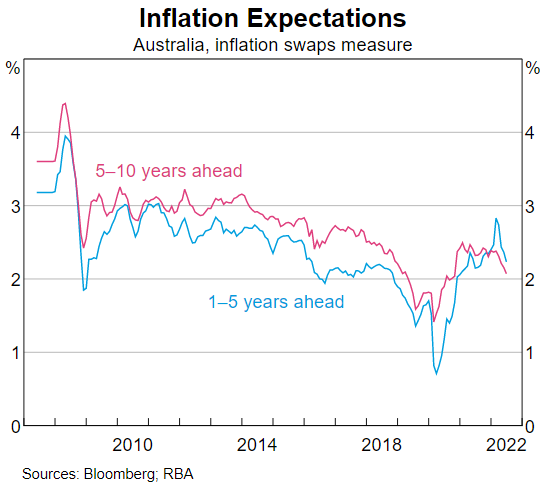

This week, we look at the for-and-against arguments whether inflation has peaked. This was among the many subjects addressed by the Reserve Bank Governor, Philip Lowe, in another speech on Wednesday that reiterated his recent views. He showed this chart as a measure that inflation expectations are tempering.

Lowe also seemed to go a step closer to accepting more responsibility for rising prices.

“I recognise though that while this approach meant we avoided some damaging long-term scarring, it has contributed to the inflationary pressures we are now experiencing.”

And he took some pressure off the expectation of immediate tightening, such as ANZ Bank's new forecasts of 0.5% in each of the next four months. He said of his firm intention to keep inflation in the 2-3% band:

“We don’t need to return inflation to target immediately, as we have long had, for good reasons, a flexible medium-term inflation target.”

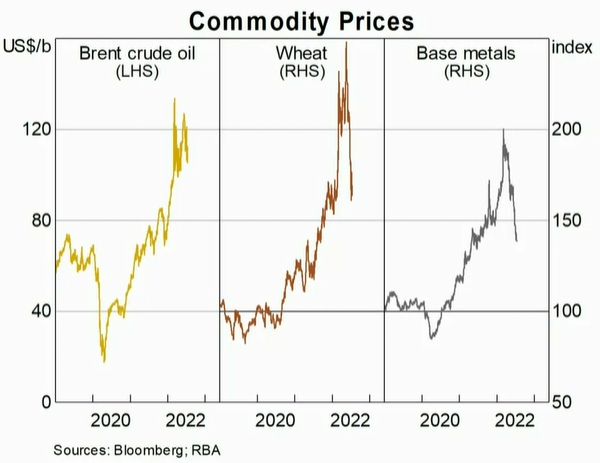

He showed this chart as evidence of lower commodity prices offering hope.

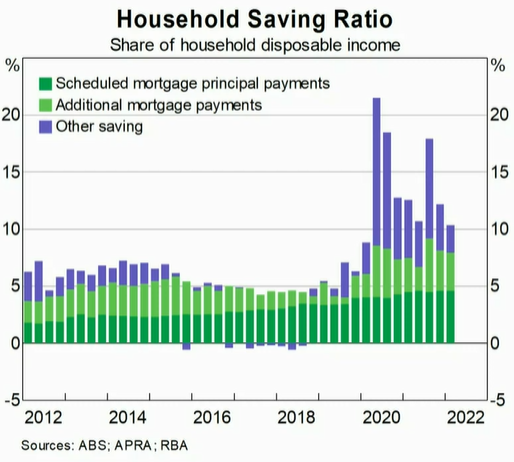

A major investment implication is the effect on the mortgage books of our banks. Lowe also used this slide to show how well positioned households are to withstand rate rises.

Australians rightly feel secure with their banks, not only supported by the Reserve Bank whenever they are in trouble, but with strong capital positions and assets heavily weighted to mortgages. But the banks time some of their capital management moves poorly. ANZ is looking to buy Suncorp by issuing $3.5 billion of new shares at $18.90, but only a few months ago, it bought $1.5 billion of ANZ shares at $27.70. As we have reported before, NAB issued $4.25 billion of new shares at $14.15 in June 2020 and is buying back over $3 billion worth at $28.63 per share. Shareholders don't seem to complain.

On the subject of banks and risk management, Tim Fuller compares the Australian and American approach to mortgages. Is there anything to learn from the land of 30-year fixed rate mortgages and its impact on borrowers and monetary policy?

Our interview this week is with Adam Grotzinger of Neuberger Berman. If there is a beneficiary of the interest rate rises, it may be new investors into bond funds who have avoided a painful adjustment phase. Adam explains how diversified global bond funds available to Australian investors are delivering around 7%. Is it time to lock some of this away, or will prices fall further?

As consumers around the world were locked up in 2020 and 2021, they turned to online stores and everything servicing that market soared. Now, even the Zooms, Amazons, Metas, Pelotons and Kogans of the world have fallen to earth, replaced by services and experiences. Aneta Wynimko looks at the 'opening trades' which are helping travel, hotels and other industries.

At turbulent times like this, it pays to check some basic principles, Shane Oliver reminds us of nine quick investing tips which stand the test of time.

Then two articles on personal tax and aged care management. Rachel Lane explores the impact on residents of aged care homes of the largest rate change in the Aged Care Interest Rate since the GFC. As tax season kicks off, Michael Brown looks at the tax advantages of ETF over managed funds.

This week, Morningstar looked at the implications of consumer spending swtiching to services with Dave Sekera looking at how to take advatanged of this trend. Nicola Chand explores the acquisition of Suncorp's banking assets by ANZ.

Graham Hand

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website