As the Australian and global economies stare down the barrel of recovery from a COVID-19 world, many predictions have been made about which businesses will survive beyond the recovery phase. One area of concern has been the severe impact this downturn will have on the Small to Mid-market (SME) business sector.

These borrowers typically have less access to capital than the big end of town and while they may be a focus of government stimulus (such as JobKeeper), it is hard to command the attention or intervention of governments in the same way that Virgin Australia did many weeks ago. Additionally, the prevalence of cheap money due to low rates and low-to-no covenant loans has created concerns that there are many ‘zombie companies’ operating across Australia whose existence are only propped up by such loans.

These are valid concerns and there will likely be some pain across many sectors of the economy over the coming months as conditions lay bare some of these structural deficiencies. At the same time, many attractive risk-adjusted lending opportunities will become available as markets and economies re-balance.

Critical considerations for lenders

Many of these predictions, while valid, short-change the opportunity in the SME sector to lend to the many well-run, well-capitalised cash generating businesses across Australia. Although smaller than their large-cap peers, that does not preclude the existence of robust businesses in the SME sector backed by good governance, strong management teams, operational integrity, strong margins and a sound balance sheet.

The key to any good business loan is these key criteria:

- Cash flow: the business has the cash flow required to service any loan undertaken, while still able to invest in the operational and capital expenditures required for the business.

- Character: the business is a well-run organisation with a quality and engaged management team with skin in the game and strong governance systems in place.

- Collateral: the business is backed by a sound balance sheet with the appropriate business assets to securitise the loan in the case of required recovery action.

What does the data tell us about lending to this sector?

Based on historical default data, what default risk might be expected in the SME debt markets in general over the period ahead? To work that out, we look at:

- The SBDFI: while not an Australian indicator (there is no such equivalent publicly available), the Small Business Default Index (SBDFI) in the United States is a good leading indicator of the US economy and marker of historical and current default rates for small businesses.

- ASIC’s Australian insolvency statistics: which provide monthly data on the number of Australian companies which have entered a form of administration for the first time each month.

- Historical default rates on corporate bonds: while corporate bonds reflect mostly large cap companies (as opposed to SMEs), they give a good proxy and overview of how the credit markets have behaved at particular points in time.

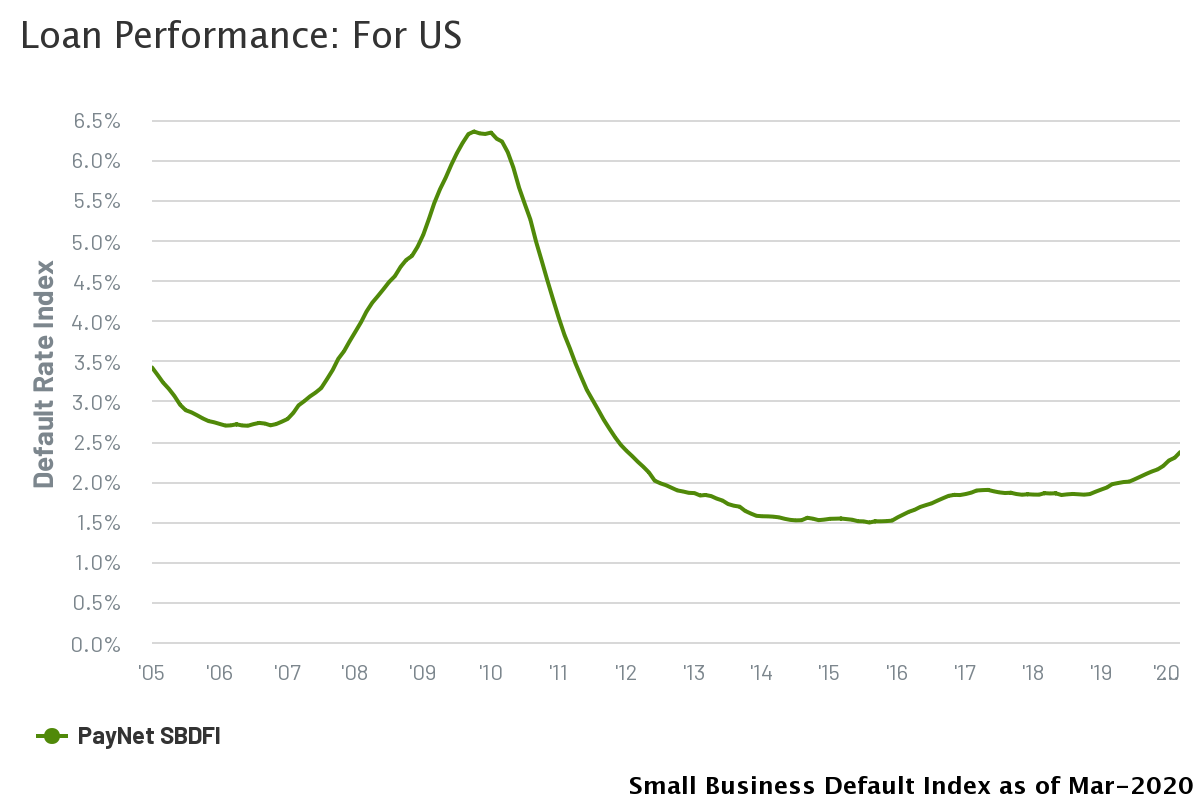

SBDFI

The chart below shows the annualised rate of small business defaults in the US since 2005.

Source: PayNet

Unsurprisingly, the chart peaked in late 2009 at just under 6.5% during the height of the GFC. This represented an almost 2.5x increase in defaults on mid-2006 of just 2.69%. The default rate has been steadily increasing since 2016 with the beginnings of a potential rise into early 2020. The latest figures from March 2020 shows a 2.36% default rate which is up about 0.50% on March 2019. It is likely that this will continue to grow as the economic impacts of COVID-19 mount in the coming months.

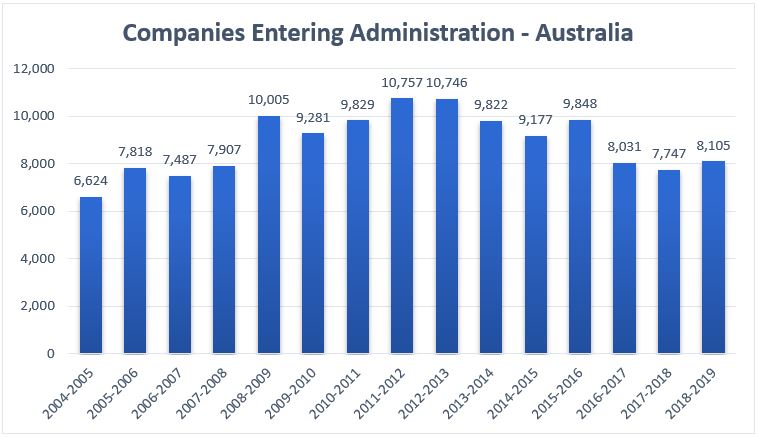

Australian insolvency statistics

The chart below shows the number of companies in Australia that have entered external administration since FY 04-05.

Source: ASIC

Looking back to the GFC, around 2008, there was a significant jump in companies entering administration from the previous year (about a 27% increase). These numbers then fell in the subsequent two years (however were still above the pre-GFC high) as some were able to keep afloat due to Government and monetary policy stimuli.

It wasn’t until FY12/13 and FY13/14 that the number of administrations peaked as businesses that likely benefited from significant stimulus packages began to struggle as fiscal and monetary policy tightened exposing some ‘zombie’ businesses propped up by those policies.

The takeaway here is that with significant government spending and quantitative easing from the RBA occurring during the COVID-19 crisis, the actual effects may not be felt for months or years down the track by zombie businesses protected by these policies. The default data is therefore a lagging indicator of economic activity.

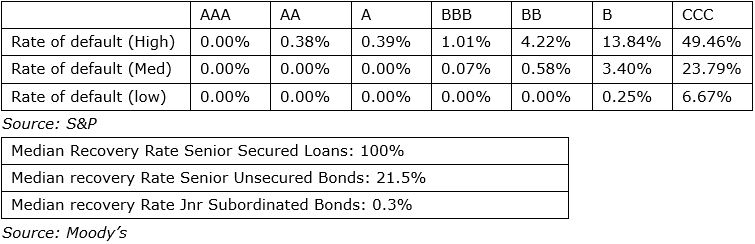

Default Rates

The tables above outline the rates of default by investment rating over the last 40 years and the median recovery rate of loans (regardless of rating) by where they sit in the capital structure.

For AAA to A rated loans, there is a relatively small difference between annual rates of default in their best years versus worst. Once entering the sub-investment grade level, the differences become higher, however, BBB and BB rated bonds still had a maximum default rate of 4.22% in their worst performing year (1982). Once entering junk bond territory (CCC), default rates are far more volatile reaching as high as 49.46% during the GFC.

Of these loans that did default, those which were senior secured experienced a median recovery rate of 100%.

As soon as an investor moves down the capital security stack, this rate decreases significantly to 21.5% for a senior unsecured bond.

These statistics highlight the importance of senior security status for capital preservation with any debt instruments (to larger or SME borrowers) and the ability to achieve an appropriate risk adjusted return on such investment.

The key takeaways

To summarise, some key takeaways are:

- It is vital that any lender fully understands the core cashflow, character and collateral characteristics of the business, how they are equipped to handle the current operating environment and their capacity to keep trading as government and monetary stimulus abates.

- While unsecured and subordinated debt can provide enticing returns for investors seeking yield, they come with significant risk. Senior security and strong cashflow foundations historically have provided investors with both income and protection of their capital. If any such debt does become impaired, having the proper security and legal structure in place gives secured lenders several alternative recovery options, where equity and subordinated debt is burned first in any recovery scenario.

- Strict investment filters, patience and deep due diligence is required to both steer through and take advantage of the opportunities that the current environment might present to senior secured lenders. This means that in this area of private debt markets, investors must be prepared to invest for a medium- to long-term horizon (i.e. 2+ years) to achieve attractive risk adjusted returns from lending to this sector in excess of 8% p.a. Additionally, managers need to have the experience and be prepared to roll up their sleeves and undertake the work required to protect an investors capital at all times.

A private debt strategy built around the three core principals of character (strong management team and businesses fundamentals), collateral (senior secured position against business assets) and cash flow (ability to service the loan and strong covenants in place to keep the borrower accountable) will provide investors with attractive risk adjusted income returns from lending to the SME/mid-market sector.

David Zipparo and Tim Davis are members of Causeway Asset Management's credit and investment team. This article is for general information only and does not take into account the circumstances of individual investors. Investors should seek financial advice before considering private debt opportunities as many structures are more suitable for sophisticated investors.