"I congratulate Firstlinks on reaching 400 editions, and I look forward to many more years of investing insights."

- Anton Tagliaferro, Investors Mutual

To mark the 400th edition of our weekly newsletter, 45 of Australia's leading investors and market experts have exclusively answered our question about the best investment opportunities for the next few years. Our thanks to them all, there are many great insights in here.

To manage the overall length, each person was given only 200 words but with a high degree of subject freedom. Some offered themes, others stock ideas, with a sprinkling of portfolio construction and sector views thrown in. They include many people who have never written for Firstlinks as we cast our net wide (articles are published in the order they were received).

We have also produced a free ebook with these insights, which we encourage you to forward to a friend or colleague and suggest they register for the free weekly newsletter.

In the 400 editions, we have published thousands of articles which remain permanently on our website. There is a button on the menu bar to find all the previous editions, as well as a list of the hundreds of writers. The search box is a great tool for researching subjects in our archives.

Firstlinks reaches about 80,000 readers a month who take two million pageviews a year. Thanks to our sponsors for supporting investor education, and to Assistant Editor, Leisa Bell, for coordinating the responses into the ebook and website.

Graham Hand, Managing Editor

What is the best opportunity for investors over the next few years?

|

Warren Bird, Uniting Financial Services

|

Miles Staude, Staude Capital

|

|

Roger Montgomery, Montgomery Investment Management

|

Gemma Dale, nabtrade

|

|

Andrew Lockhart, Metrics Credit Partners

|

David Harrison, Charter Hall

|

|

Jonathan Rochford, Narrow Road Capital

|

Hugh Dive, Atlas Funds Management

|

|

Jordan Eliseo, The Perth Mint

|

Marcus Padley, Marcus Today

|

|

Shane Woldendorp, Orbis Investments

|

Reece Birtles, Martin Currie Australia

|

|

Noel Whittaker AM

|

Shane Miller, Chi-X Australia

|

|

Don Stammer

|

Ilan Israelstam, BetaShares

|

|

Alex Pollak, Loftus Peak

|

Chris Stott, 1851 Capital

|

|

Sarah Shaw, 4D Infrastructure

|

Bill Pridham, Ellerston Capital

|

|

Beatrice Yeo, Vanguard

|

Ama Seery, Janus Henderson Investors

|

|

Marian Poirier, MFS Investment Management

|

Nandita D’Souza, Citi Australia

|

|

Phil Ruthven, Ruthven Institute

|

John M Malloy, Jr., RWC Partners

|

|

Bei Bei Hu, Maple-Brown Abbott

|

Chris Cuffe, Third Link Growth Fund

|

|

Kate Samranvedhya, Jamieson Coote Bonds

|

Anton Tagliaferro, Investors Mutual

|

|

Patricia Ribeiro, American Century

|

Mike Murray, Australian Ethical

|

|

James Maydew, AMP Capital

|

Daryl Wilson, Affluence Funds Management

|

|

Claire Smith, Schroders

|

Oliver Hextall, Fidelity International

|

|

Jun Bei Liu, Tribeca Investment Partners

|

Kej Somaia, First Sentier Investors

|

|

Lawrence Lam, Lumenary Investment Management

|

Dr. Stephen Nash, BondIncome

|

|

Nicholas Ali, SuperConcepts

|

Vince Pezzullo, Perpetual Investment Management

|

|

Ashley Owen, Stanford Brown

|

Hamish Douglass, Magellan Asset Management

|

|

Matt Reynolds, Capital Group

|

|

*****

Warren Bird, Uniting Financial Services

Executive Director

Achieving real diversification

The best opportunity in the future is the same opportunity as we’ve always had – to build a growing base of wealth and income through a diversified portfolio of financial assets. Diversification is the key to ensuring that when something goes wrong, it doesn’t blow up your portfolio, remaining only a small blip within a solid overall outcome. It's the opportunity to have no regrets.

There are plenty of opportunities to do this properly. You don’t need a special insight or a slice of luck.

I don’t mean that you need to hold a few shares plus a property or two and some fixed income. Asset class ‘diversification’ is not the main story. The individual investments you own need to be an appropriately small portion of your total holdings that, if they fail, they won’t bring you unstuck. Lots of individual assets, spread across many industries and countries, is critical. Local share portfolios need at least 30-40 stocks, but you also need some well diversified exposure to global markets. Credit portfolios need at least 100 (more if you have high yield bonds) and not just A$ holdings. Properties need diversified tenant bases (or at least the potential to replace a tenant from one industry with someone in a different field altogether).

Roger Montgomery, Montgomery Investment Management

Chief Investment Officer

Macquarie Telecom is building a quality business

In a world of AI, fintech, autonomy, broadband, electric vehicles and platform revenue models, a steady reliable income stream seems like a boring prospect, but we believe attractive investment returns will be born from pursuing such income streams.

In the absence of rapidly rising interest rates, inflation or central banks losing control of the bond yield curve, interest rates on cash will remain punitive and we believe income-producing assets that can be acquired at attractive yields will attract eager buyers later.

Consider a data centre company like Macquarie Telecom or a telecommunications business like Uniti Wireless. These businesses are managed by highly-regarded founders with a reputation for delivering value as well as a strongly-aligned ownership incentive. And while they aren’t generating those steady, boring annuity style income streams just yet, they are growing rapidly towards that endgame.

Cloud, data centre, government cyber security and telecom company Macquarie Telecom is majority owned and managed by David Tudehope. He has systematically converted a carpark in Sydney’s north to a multibillion-dollar data centre with regulators, government departments and major corporates as tenants. When complete, and fully tenanted, a steady, reliable and boring annuity stream will emerge.

Such income streams will be attractive to large super and pension funds willing to capitalise such assets on much lower rates than individual investors and so a steep premium could transpire, providing another avenue for capital gains for investors with patience.

Andrew Lockhart, Metrics Credit Partners

Managing Partner

Position for rising rates with an investment in corporate loans

When interest rates hover near historic lows for long periods, it is easy to forget that they will inevitably go up. The recent spike in US Treasury bond rates is a warning that investors are starting to worry about inflation again. Unprepared investors in fixed-rate bonds risk substantial potential loss of capital and also risk missing out on the income boost as the global economy recovers and interest rates rise. Equity markets can also be more volatile during inflationary periods, with growth stocks retreating.

One asset class worth considering in this environment is private debt. Australian corporate loans earn their returns from lending fees and interest that is generally charged over a floating base rate, ensuring their returns increase as the RBA raises its cash rate. While rates are low, and income is hard to come by, a well-managed corporate loan fund can be a rare source of reliable monthly income and provide attractive returns compared to equities and traditional fixed income with less volatility than fixed rate bonds and equity markets.

And when rates do start to rise, you’ll be protected against inflation and able to capitalise on rising rates, without the risk of capital loss.

Jonathan Rochford, Narrow Road Capital

Portfolio Manager

Australian private credit has a role in most portfolios

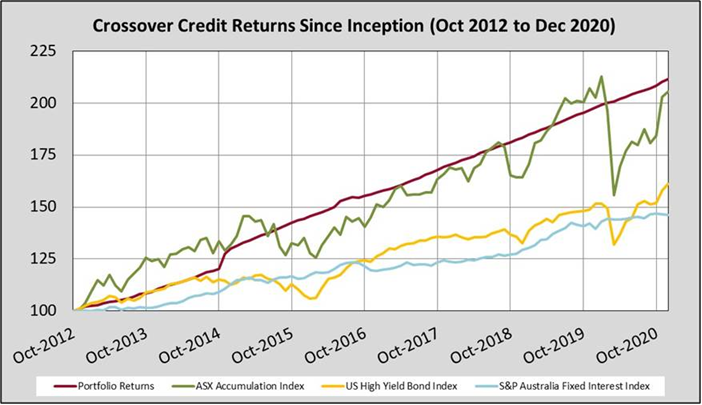

At a time when the valuations of many asset classes including equities, property and long bonds seem stretched, Australian private credit offers several attractive features. Whilst private credit is a broad church ranging from low risk loans against completed residential property through to higher risk, mezzanine loans on construction and private equity transactions, two common features standout.

First, private debt is typically floating rate or short duration fixed rate debt, so it has good upside when interest rates rise. Second, Australian private credit offers an attractive risk/return trade-off which can deliver equity-equivalent returns but with lower volatility. The graph below shows historical returns on the crossover credit portfolios (credit ratings around BBB and BB) against the ASX accumulation index, US high yield bonds and an Australian fixed interest index over eight years.

The trade-off for this strong relative performance is illiquidity, with private debt typically bought on a ‘hold to maturity’ basis. For those with an investment horizon of at least three years, typically super funds both large and small, private credit can assist by boosting returns compared to other low to medium risk assets and by reducing the fluctuations in the portfolio value.

Jordan Eliseo, The Perth Mint

Manager, Listed Products and Investment Research

Set realistic expectations

Investors may be well served watching a replay of the 1,000m short track speed skating final at the 2002 Winter Olympics, when Australian Steven Bradbury won the gold medal. While everyone else was trying to go as fast as possible (maximise returns) he stayed on his feet when they crashed.

Sometimes that’s the key to winning in investment markets.

In the 10 years to end-2020, diversified growth funds returned 9% per annum, while the S&P 500 price index essentially tripled. That is an extraordinary result given the unresolved economic imbalances that date back to the GFC era, all of which were exacerbated by the unprecedented collapse in activity caused by COVID-19, and the policy response to the pandemic.

Given where bond yields and valuations for equity markets (especially in the United States) currently sit, it’s not unrealistic to expect that markets as a whole will deliver nothing in real terms during the decade ahead, with a swathe of blue-chip fund managers advising investors that they have materially downgraded projected asset class returns.

That may not sound optimistic but forewarned is forearmed. Investors should prepare accordingly.

Shane Woldendorp, Orbis Investments

Investment Specialist

Bayerische Motoren Werke AG (ETR:BMW) and Naspers (JSE:NPN)

For more than a decade, we have witnessed Growth shares outperforming their Value counterparts. It has been gratifying to see the unusually wide premium given to Growth shares recently begin to contract. This has been driven by a vaccine-led economic recovery that has benefited the more cyclical shares, which also tend to be Value-oriented at present. In addition, small increases in 10-year bond yields have taken some of the gloss off of the high price-to-earnings (PE) multiples that the market had been ascribing to technology-oriented shares.

Despite this recent outperformance, we believe Value shares still look cheap relative to the broader stockmarket as indicated by unusually wide PE differences between the average company in the stockmarket and the more Growth-oriented companies. The same conclusion can be reached when looking across a wide range of other valuation metrics. Historically, one of the best times to own Value shares has been in a post-recession recovery period, so Value investors now have both timing and valuation on their side.

A good example of this opportunity is BMW. While the pandemic has understandably put pressure on luxury car sales in many markets, people can’t put off buying a replacement car forever. With what we view to be a robust balance sheet and a compelling selection of new electric and hybrid models in the pipeline, we are excited about BMW’s ability to capitalise on the opportunities a recovering economy presents. Its shares are available at around six times our conservative assessment of ‘normal’ earnings and a 20% discount to the book value of its tangible assets.

While investors often lean heavily on generalisations, you should not let these force you to overlook opportunities. So while on average Value shares look more attractive than Growth shares, you can still find opportunities in Growth-oriented companies, particularly outside of the favoured the US technology sector. One such example is Naspers, a South African-listed holding company whose largest underlying asset is a 31% stake in Chinese internet giant, Tencent. As a result of Naspers’ unusually large holding company discount, investors have an opportunity to access one of the best and most dominant companies in the world, Tencent, at around a 50% discount.

Noel Whittaker AM

Author, Executive in Residence and Adjunct Professor, QUT Business School

Cracking the demand for aged care

We live in a dynamic world, with new product breakthroughs being released continually. But to get an idea of where the action will be happening in say five years’ time, we need to contemplate what the world may look like then. In Australia, the facts are clear. Over 65s are the fastest-growing demographic in the country, and thanks to advances in lifestyle education and medical breakthroughs, their life expectancies are increasing.

The success of my new bestseller, ‘Retirement Made Simple’, is proof that these people have a thirst for knowledge but most of them have a strong view that they want to age at home. This may be a wonderful ideal, but there are practical problems. It’s common in a couple for one partner to need care while the other one stays in good health. On top of that, there are a growing number of single older people, often due to the death of a partner, that while they stay at home, still need assistance for going to the shops, attending doctors’ appointments and the like.

There will be two basic solutions. One will be for the providers of retirement living to produce attractive and affordable accommodation. The main challenge here is both finding an appropriate site and then staffing it at a cost which is in line with their budget. The other solution is to provide care in the home on an effective and regular basis at an affordable cost. Right now, the unsatisfied demand for aged care places is huge and getting worse.

The person or corporation who can solve these problems will have a gold-plated future.

Don Stammer

Former Director of Deutsche Bank, columnist for The Australian

Watch a few key influences

The last 12 months show that a global recession and panic in financial markets provide opportunities to buy quality shares cheaply. But framing an investment strategy for the next couple of years needs consider these key influences:

- With average share prices 80% higher than a year ago, most shares are no longer cheap.

- Global growth has quickened and should pick up further unless mutations of the virus undermine the benefits of mass vaccination.

- Forecasts of aggregate profits will also be raised but unevenly by country, industry and company.

- Easy money and abundant liquidity have boosted the appeal of shares.

- Bond investors had largely ignored inflation until recently but are now exaggerating the risk of its early return and under-playing prospects for inflation on the medium-term.

- Keen environmentalists say renewable energy is now cheaper, cleaner and profitable but the substantial subsidies from government are a reminder it’s still not easy being a green investor.

- ‘Rotation’ has short-term appeal, but my preference is to focus mainly on companies able to generate strong cash flows, whether retained to grow the business (CSL or Microsoft) or paid as dividends (Australian banks).

Alex Pollak, Loftus Peak

Chief Investment Officer

How to play 5G

An obvious answer to the question of coming investment opportunities is the roll-out of 5G telephone services globally. But the obvious way to play it (Telstra and other phone companies, Ericsson, Nokia and even Apple) in our view is not where optimal returns will be had.

We view 5G predominantly as a data play. 5G not only dramatically increases the speed that data travels a wireless network data pipe but also significantly decreases latency, a measure of the network’s responsiveness.

Reduced latency is critical in many future applications such as remotely automated vehicle guidance (the brakes need to go on now!) or in health care, such as remote heart rate monitoring.

Underpinning this move to 5G are data tools, hardware and processes which we believe will offer the best opportunities. Is there enough digital infrastructure in the right places to allow this to happen? Not yet, but there will need to be.

And once the capacity is there, expect to see a raft of new applications enabled on 5G which were not possible before, in much the same way as 4G was a major catalyst to growth of Netflix, Uber and indeed Amazon’s data business.

Sarah Shaw, 4D Infrastructure

Chief Investment Officer

Global infrastructure has a multi-decade runway

The opportunity for global listed infrastructure investment over coming decades is huge. An aging existing infrastructure inventory, a growing global population and evolving thematics such as the growth of the middle class, especially in emerging economies across Asia and Latin America. Global decarbonisation goals demand a huge amount of infrastructure spending.

At the same time, infrastructure’s unique characteristics offer investors defensive earnings with economic diversity. It can be actively positioned for all points of an economic cycle and whatever cyclical events the future throws at us, whether economic, political, environmental or health.

This investment thematic has been enhanced by the COVID-19 pandemic. Huge COVID-19 government stimulus programmes are fast-tracking infrastructure investment (in particular the energy transition). Increasingly stretched government balance sheets will see a greater reliance on private sector capital to build much needed infrastructure, and a ‘lower for longer’ interest rate environment is supportive of infrastructure investment and valuations. This leads to enormous opportunity for private sector infrastructure investment. We can think of no more compelling or enduring global investment thematic for the coming 50 years.

Beatrice Yeo, Vanguard

Economist

Goals met by total return approach

Vanguard’s outlook for global asset returns is guarded for 2021 and beyond. In our view, the solution to this challenge for investors is not aggressive tactical shifts but rather a well-diversified, balanced portfolio with an appropriate mix of equities and bonds.

While high valuations have created investor concerns about holding equity, historically low yields suggest that those who remain in shares can expect a modest increase in compensation for taking on this additional risk in the coming years. Notably, equities are likely to continue outperforming most other investments and the rate of inflation, with annualised returns expected to be 5% to 8% versus 0.5% to 2.0% for traditional bond instruments over the next decade.

That said, high-quality bonds continue to play an important role as a diversifier in a portfolio, especially with a large degree of economic uncertainty still looming in the horizon. While recent increases in the bond/equity correlation limits the role of bonds as a perfect hedge, the less than perfect correlation and low beta to equities still reaffirms the diversification properties of fixed income. As such, rather than replacing bonds with higher-yielding assets, we encourage investors to maintain a broadly diversified portfolio and adopt a total return approach to investing, drawing down on both capital and income streams to meet their goals.

Marian Poirier, MFS Investment Management

Senior Managing Director, Australia

Active management taps into ESG opportunity

After an unpredictable 12 months, it’s hard to think about what may lay around the corner. However, at this point in the cycle, we urge investors to consider a strong focus on risk management and mitigating downside risk in investment markets.

Looking through an ESG lens, we believe the pandemic will have long lasting impacts on governments, consumers, companies and industries. The move toward sustainability is a disruptive force and will define society and the investment landscape for decades.

Active risk management is essential in accurately assessing risks in this uncertain environment, as well as avoiding entities that may stumble or fail. No one knows with certainty if we have entered a prolonged economic downturn or if economies will bounce back once reopened. However, three things seem clear to us:

- the low-volatility environment of the past 10 years has ended

- capital market returns will be low over the next 10 years

- finding alpha during difficult markets will become increasingly important for driving long-term results.

The opportunity for alpha generation and above-average returns for active managers that invest over a complete market cycle could be powerful. Moreover, in a more volatile environment that has investors waiting for the other shoe to drop, active management will play a critical role in helping to create value by allocating capital responsibly.

Phil Ruthven, Ruthven Institute

Founder and CEO

Over time, shares likely best bet

In a world going through one challenge after another, how do we choose performance and safety together for investing into the middle of this decade?

If it’s not a pandemic, there are: record low interest rates; gold prices going one way while some other metal prices go in the opposite direction; record peace-time deficit spending; new financial intermediation including cryptocurrencies and block chain; traditional ICE car manufacturers challenged by Tesla’s EVs, trade wars, and heaps of other distractions.

We have a choice between passive asset classes and active asset classes. The passive ones (bonds, cash, property and collectables) look like staying lowish or requiring special skills as in the case of collectables. The active and semi-active ones (shares, both local and international, and infrastructure products) may be the best bet.

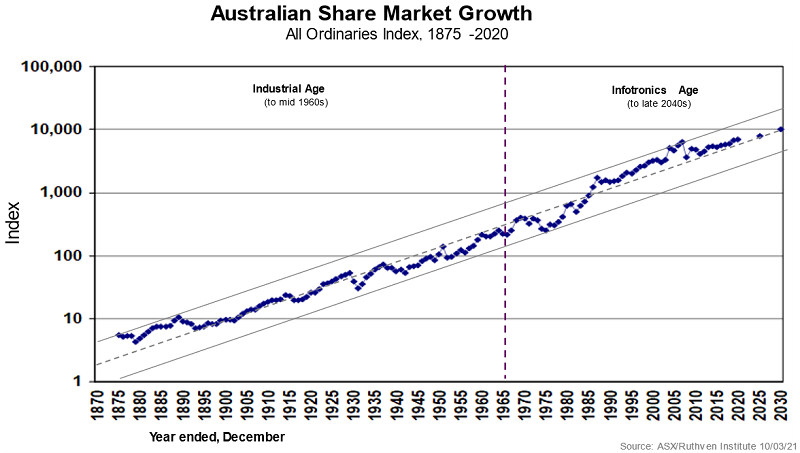

Australia’s share market over the past century and a half offers some promise of safety and performance. The chart below suggests our All Ordinaries Index is bang on trend in 2021, with prospects of it trending to 8,000 in 2025 and 10,000 in 2030; ups and downs notwithstanding.

And as Martin Zweig said decades ago: the trend is your friend!

Bei Bei Hu, Maple-Brown Abbott

Investment Analyst, Asian Equities

Value and fundamentals to come to the fore

A major trend in recent years has been the unjustifiable de-coupling between the strong underlying fundamentals of many companies and their prevailing share prices. We believe this will be an area of opportunity for savvy investors over the next few years.

Stimulus measures around the world, coupled with the increase in bond yields, have underpinned a sharp market rotation towards value – which has long been out of favour. During 2021 and into 2022, we expect greater interest in cyclical sectors such as financials, commodities and some industrials that in many instances were trading at record discounts. On top of this, climate change, healthcare, and continued digital disruption are multi-year themes which will reshape the way we live, work, commute, socialise and of course invest. We continue to favour companies with strong balance sheet, good execution and trustworthy management teams in their respective fields.

Despite the early value rotation, the weight of money remains herded toward a narrow group of very large and richly-priced stocks suggesting the rotation remains in its infancy. From this perspective, we believe that there will be an increased focus on underlying value rather than a continuation of the growth story of the past decade, which will provide good opportunities for investors.

Kate Samranvedhya, Jamieson Coote Bonds

Deputy Chief Investment Officer

Duration back in favour for bonds

It is easy to vilify duration lately. The trade to hedge reflation has been to sell duration (ie sell long bonds or move to shorter terms). I argue that we are near the turning point. This healthy upward adjustment in yields resets a new level to invest in duration for three reasons.

Firstly, US inflation is rebounding from the base effect and should peak around 3% in April or May, then it should fall back towards 2%. This is the transient part. The more difficult part to forecast is how elastic supply will be when pent-up demand shows up later, to really print sustainable inflation above 2%. In short, the easy part of bond sell-off is nearly over.

Secondly, the 10-year US Treasury yield has risen to surpass S&P 500’s dividend yield, which the market has not seen since pre-COVID.

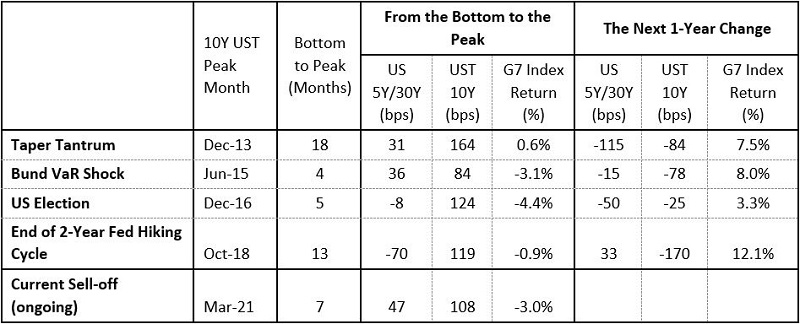

Thirdly, if the peak in bond yields materialises over the next few weeks or months, bond returns afterwards are often hefty. In this table, the previous episodes of bond sell-off showed that we can be only 15-50 basis points away from the peak yield this year. The bulk of the damage to bond returns has already been done. The average G7 government bond return after the previous four major selloffs is 7.7%.

Past Bond Sell-Offs – Bottom to Peak

Source: Bloomberg and Jamieson Coote Bonds.

10-year US Treasury yield now surpasses S&P 500 dividend yield, not seen since pre-COVID

Source: Bloomberg and Jamieson Coote Bonds.

Patricia Ribeiro, American Century

Senior Portfolio Manager

Tech companies meeting changing consumer needs

The COVID-19 pandemic has created long-term structural changes in consumer behaviour beyond e-commerce, including remote working, distance learning and virtual health care.

The pandemic’s impact on e-commerce is evident but its effect will reach well beyond online shopping. The need to bank, learn, work, play and even communicate remotely as result of lockdowns has hastened the use of digital technologies.

In fact, consumers’ attitudes on work, transportation, health and hygiene, education and entertainment have shifted, perhaps permanently. The use of online platforms has expanded dramatically, requiring increased development of sophisticated internet infrastructure, including 5G networks.

The pace of digital adoption should quicken even further as remote working, online learning and e-commerce penetration continue to rise.

These trends are particularly prevalent in emerging economies, where approximately 75-80% of the world’s consumers will soon reside, according to the Brookings Institute. We expect the pattern of faster digitalisation in China, which has continued after the loosening of virus mitigation measures, to develop across emerging markets.

This transformation should create investment opportunities with tech companies whose products and services address the needs created by these trends likely beneficiaries.

James Maydew, AMP Capital

Head of Global Listed Real Estate

Listed real estate is a reopening trade

In our view, the best opportunities are not in one region or sector but global listed real estate in its entirety. We believe it is currently heading into a Goldilocks scenario based upon the following five preconditions:

- Interest rates are being kept low by central banks, a clear and well communicated strategy. The asset class is capital intensive and therefore thrives on a lower interest rate environment.

- Stimulus relative to GDP is extraordinary and will find its way into all financial assets. A rising tide lifts all boats.

- Inflation expectations have been on the rise, and the asset class is an inflation hedge and performs well in and inflationary environment.

- There is an increasing number of deal opportunities for true active managers to capitalise on given the extraordinary valuation discrepancies that have occurred due because of COVID-19.

- The short-term cashflow challenges created by COVID-19 in real estate have opened up extraordinary valuation opportunities. Since the Pfizer vaccine news in November 2020, equity investors have been searching for sectors that will benefit from a return to normal in a post-COVID world (‘the reopening trade’). The sector is one of those key beneficiaries from the cyclical recovery to normal and remains fundamentally cheap relative to all others asset classes.

Claire Smith, Schroders

Alternatives Director

Private equity still offers value

With historically low interest rates, and polarising equity valuations, investors are looking for new ways to earn returns. Private equity has a role to play.

Private equity has historically been difficult for retail investors to access, however product innovation has reduced the barriers to entry, presenting opportunities for investors to diversify their portfolios and access significant growth potential over the next few years.

Private equity offers access to companies that are diverse in their stage of maturity and in their size. Investors can access venture capital, small to mid-sized companies in mature regions, or growth companies in growing regions like Asia through the private equity market.

The number of unlisted companies compared to listed companies has grown strongly over the past 20 years, particularly in regions like tech and healthcare, providing a wider set of investment opportunities in the private space. The larger investment universe, combined with access to non-public research insights, gives private equity fund managers an advantage in portfolio construction.

We believe the outlook for private equity is positive. As private equity transactions price off fundamentals, we’re currently seeing very well priced opportunities.

Jun Bei Liu, Tribeca Investment Partners

Lead Portfolio Manager

Connected care and wearables changing healthcare for the better

The intersection of technology and big data in healthcare has resulted in medical advances that also deliver investment opportunities. A good example is wearable devices that maintain the continual monitoring of biomedical signals for those wearing them. When this medical technology is married with algorithms and artificial intelligence it has the potential to transform healthcare.

These technologies can deliver early diagnosis with patients and their physician alerted when a visit to the clinic is required. Monitoring also boosts compliance with health treatments and has ability to reduce unnecessary doctor visits. Medical research can also benefit from cheaper more accurate medical trials.

While the technology already exists and, in some cases, has been rolling out for years, its functionality goes well beyond the fitness trackers we have all become familiar with. Many know the Apple watch and its use to identify cardiac arrhythmias. However, less well known is ResMed’s position as a leading provider of connected care with its CPAP devices. With more than 13 million cloud-connected devices, ResMed has a near unassailable lead over rivals with a database containing billions of nights of sleep data. It is seeking to further expand its connected health offering into Asthma and COPD – two large and expensive respiratory conditions.

This is just one example of a company that is making great strides in healthcare technology, and further developments in this space is a trend we believe will gain momentum in coming years.

Lawrence Lam, Lumenary Investment Management

Managing Director and Founder

Clipping every ticket

We’re seeing a group of emerging companies capitalising from the global shift towards channel unification. I’ll illustrate this through the bets our fund has made in unified global payments processing, and unified communications.

The habits of future generations are evolving rapidly. There’s a plethora of channels which customers can use to pay, presenting an issue for companies with global customers. How can they cater for this wide range of payment methods? This task is impossible to manage internally so they require access to systems that unify these payment channels into one easy-to-manage platform. Our fund has invested in one such founder-led payment unification company: Adyen is a Dutch company taking a slice of every transaction that is processed on its global platform.

A similar evolution is happening in communications. Think about how many communications channels there are, such as messaging platforms, emails, SMSs and phone calls. These require aggregation so companies can keep track of and target their desired audiences. Our investments generate revenue from every message, SMS, email or phone call made globally and we see rapid growth over the coming years.

Nicholas Ali, SuperConcepts

Executive Manager, SMSF Technical Support

Think long-term, diversify and seek advice

If I knew the answer to this ‘best opportunity’ question, I’d be on my private Caribbean island rather than typing away in my home office.

For me, the best strategies for investors over the next few years are twofold. Firstly, diversify across multiple asset classes. Secondly, seek professional advice, especially in areas where you don’t have sufficient knowledge.

Diversification – get rich slowly

Diversification won’t bring you quick riches, but smart portfolio diversification is key to steadily building wealth over time. Whilst it does not guarantee against loss, diversification is the most important component of reaching long-range financial goals while minimising risk.

Some important points to remember about diversification:

- It reduces risk by investing in vehicles that span different financial instruments, industries, and other categories.

- Unsystematic risk (such as that associated with a specific company shares) can be mitigated through diversification, while systemic or market risk is generally unavoidable.

- No matter how diversified your portfolio is, risk can never be eliminated completely.

Professional advice – seek and you shall find

Professional advice includes investing, insurance and estate planning. It should be personalised to your individual situation and based on your needs and goals. Sound strategic advice can present opportunities to minimise tax, boost retirement savings, as well as retirement income and ensure your loved ones are catered for upon your demise.

These two simple yet effective approaches to investing will go a long way to giving you the best opportunities to build wealth over the next few years.

Ashley Owen, Stanford Brown

Chief Investment Officer

The lucky country but continue learning

For long-term investors, living in a country that has been blessed with uninterrupted growth and progressive, growth-oriented governments has meant that a ‘buy & hold’, ‘set & forget’ strategy has been reasonably successful, as long as they got the timing right.

Step outside this lucky country club into any of the 200 other countries on earth and people laugh at you if you suggest ‘buy & hold’ as a serious investment strategy. Other countries don’t offer the same protection of property rights, rule of law, consumer and investor protection, freedom of speech and dissent, and relatively stable political, administrative, regulatory and judicial systems.

We are lucky to have been born in (or allowed into) a favourable country for investors.

But investors should still never simply ‘buy & hold’ or ‘set & forget’ their investments. Take company shares for example. There have been about 37,000 companies that have raised money from investors and listed on one or more of Australia’s numerous stock exchanges at some time or another since the early 1800s. There are just 2,300 of them left on the ASX, and only around 500 of these make any money (and that was in 2019, before Covid!). For every winner there were hundreds of total losses.

There are no such things as safe, reliable ‘blue chip’ companies that can be relied upon to survive and prosper for long. Even the oldest and largest companies like the Bank of NSW (Westpac) and BHP have suffered several multi-decade periods of chronic under-performance, plus a number of ‘near-death’ experiences along the way. As investors, we need to be active, never take company accounts and audit reports at face value, and do our own research, learn to ignore the daily market ‘noise’, media sensationalist headlines, and gratuitous ‘advice’ from friends, neighbours and websites, all spruiking the latest ‘hot stock’ or ‘hot fund’.

We need to recognise changing conditions, make adjustments, never panic buy in booms (or at least don’t gear up), never panic sell in busts, and be prepared to go against the crowd. Investing is a never-ending learning experience.

Matt Reynolds, Capital Group

Investment Director

Health care and renewables for the next decade

Many investors are today wondering – and perhaps already acting on – the question of, “what is the best investment opportunity over the next few years?”

At Capital Group, our approach is a little different to most because we don’t shape our thinking around the next few years. We believe the right time horizon to frame this type of thinking around is at least 10 years. As our Vice Chairman, Rob Lovelace has noted before, “Imagining life in 2030 is not a hypothetical for me. In the portfolios that I manage, my average holding period is about eight years, so I’m living that approach to investing.”

For example, 10 years from now we may look back on COVID-19 as our generation’s “Pearl Harbor moment” — a period when extreme adversity spurred incredible rates of innovation and behavioural changes to help address some of the era’s biggest problems. When Pearl Harbor happened, the US artillery was 75% horse drawn. Yet by the end of the war they had entered the atomic age. That incredible transformation sparked a period of innovation and growth in the US economy that lasted for decades.

Innovation in health care is accelerating at warp speed. Renewable energy is starting to power the world and may well be the predominant energy source come 2030, while electric and autonomous vehicles are hitting the fast lane. With such monumental structural change before us, it’s only natural to want to understand, to know of, and to invest in the companies that will be at the apex of such change.

But if time has taught us anything, it is that long-term wealth is created by taking a long-term perspective. Big market and economic changes happen periodically and while the COVID-19 pandemic still swirls around us, history will mark it down as yet another market event.

So perhaps the best answer to the question of “what is the best opportunity for investors over the next few years” is this: take a long-term perspective and invest in the companies and ideas that will endure beyond the next few years. And that is totally where our focus is.

Miles Staude, Staude Capital

Portfolio Manager

Bet on an unprecedented recovery, the sharemarket is the place to be

There has been a seismic shift in thinking by both policymakers and society at large since the 2008 financial crisis. A decade ago, the mantra of austerity dominated the debate about government finances. It also heavily influenced the shape of the economic recovery that followed. Furthermore, a large constituent believed that the birth of new ‘unconventional’ tools, such as quantitative easing, were both morally wrong and a harbinger for 1970’s inflation.

Fast forward to today and - rightly or wrongly - governments have learned that indebtedness is nothing to fear, and that austerity has become a dirty word at the ballot box. Moreover, despite a decade of central banks printing money, inflation remains too low, not too high.

Thus, facing this new crisis, governments and central bankers have now ‘gone big’ in a way we have no precedent for. With a veritable tidal wave of stimulus set to wash over the global economy, markets currently look unprepared for the huge surge in global growth that is coming this year and next. When it comes, global equities stand out as the place to be. Levered to a growth surprise in a way debt markets are not; the share market also offers the best place to hide should we finally face a real (or imagined) inflation scare.

Gemma Dale, nabtrade

Director, SMSF and Investor Behaviour

What to own over the next five years

While markets are generally forward-looking, that foresight is often limited to the next six to 12 months. Longer-term trends can often be less sexy and investors may postpone backing first movers until business models are proven. A clear example is decarbonisation, a critical global trend that receives relatively little attention from Australian investors.

While Australia has been slow to mandate emissions reduction targets and is resisting calls for carbon tariffs, the global trend towards decarbonisation is picking up pace. Joe Biden campaigned on a pro-environment platform and as President, he will usher in a wave of green technology investment in the trillions. China, the world’s largest emitter, has committed to carbon neutrality by 2060, with other developed nations pledging to achieve this target by 2050. In 2018, emissions in the US, the EU and Japan were lower than they were in the 1980s (Bloomberg). The list of vehicle manufacturers committing to electric vehicles only by 2030 now includes Volvo, Ford Europe, Audi and Bentley, while Jaguar has committed to all EVs by 2025.

So why does this matter for local investors? In 2020, the top 10 stocks bought by investors, including those on nabtrade, included carbon-intensive sectors such as materials (BHP, RIO and Fortescue Metals), and travel (Qantas and Flight Centre). Typically, the top 10 stocks for a retail investor comprise over half their total portfolio. Energy companies such as Woodside and Santos were bought on weakness.

The Australian share market offers relatively slim pickings for investors who wish to invest in the global decarbonisation trend; additionally, overweight positions in emissions-intensive sectors may prove a drag on portfolios as the decarbonisation trend accelerates.

When domestic investors invest in global stocks, their appetite for stocks aligned to this trend is much greater. Tesla remains by far the most popular international stock on nabtrade, and Nio (the Chinese EV manufacturer) is often in the top 5. Investors have a modest appetite for lithium producers on the ASX, particularly Lynas Corp (LYC) and Piedmont Lithium.

Forward-thinking investors should consider whether their portfolio has sufficient exposure to this trend, as one thing is for sure. It isn’t going away.

David Harrison, Charter Hall

Managing Director and CEO

The security of long-term leases to quality tenants

In a lower for longer interest rate environment, investors will increasingly be looking for stable returns underpinned by high levels of income.

Charter Hall believes the best opportunity for investors who want liquidity and can tolerate volatility is to focus on listed REITs. However those that prefer limited volatility, steady yield growth and capital appreciation should focus on unlisted property funds that own quality properties offering long leases to tenants in cyclically resilient industries or tenants that are dominant in their sector, and of course government, and government back, entities. These portfolios should have a long WALE (weighted average lease expiry) and structured annual rental increases to maximise investor returns over the medium to long term.

WALE is an important metric used to measure the average expiry period of all the leases within a property or fund. A lower WALE may indicate there are vacancies or tenants are on short-term leases. Conversely, a higher WALE points to a stable tenant mix, with lower vacancies and tenants on longer-term leases which provides more certainty in future cashflows.

The ASX-listed Charter Hall Long WALE REIT (ASX:CLW) currently has an average WALE of 14.1 years with long leases to highly rated tenants such as the Australian Government, Telstra, BP, Coles and Australia Post while the unlisted Charter Hall Direct Long WALE Fund has a WALE of 7.9 years with long leases to tenants such as Bunnings, Woolworths, Toll and Shell.

Hugh Dive, Atlas Funds Management

Chief Investment Officer

Demand for medical testing can only increase

When Nobel prize-winning physicist Niels Bohr famously noted that "Prediction is very difficult, especially if it's about the future", he could well have been talking about investors making confident predictions on long term investment opportunities.

For many ASX-listed companies, it is difficult to predict that their earnings will be significantly higher in the medium to long term. This is due to inevitable changes in consumer tastes, new mines currently in development adding to supply, or simply that the company operates in a constrained domestic oligopoly.

However, there is one area where I do have confidence in making a prediction. In the future, the population will be older, sicker and have increasing health demands, which will result in more frequent trips to the doctor and increased medical testing. Additionally, medical science advances regularly expand the number of tests ordered to improve health outcomes, with genetic testing being the latest frontier. Cynics may say that malpractice lawsuits and an increasingly litigious society incentivise doctors to order additional patient testing, especially when the cost of testing is paid for by either the state, an insurance company or the patient.

One Australian company that will capitalise on these healthcare trends is global pathology company Sonic Healthcare, which is now the world's third-largest medical laboratory company. While 2020 has seen record profits for Sonic due to COVID-19 testing, but the company's share price has fallen due to concerns about COVID-19 testing falling sharply and represents an interesting investment opportunity. Elevated testing demand will continue, augmented by serology or antibody testing, as travellers apply for time-limited immunity passports. The number of tests ordered per patient is expected to rise along with the median age of the population in the company's key pathology markets of Europe, Australia and the USA.

Marcus Padley, Marcus Today

Author and Portfolio Manager

Travel will benefit from a tidal wave of demand

The stock market rarely looks more than a year or two ahead and trends that last more than two years are only ever priced in incrementally. This is why BNPL has provided an extraordinary investment. It is not a fad, it is a long-term shift, a tidal wave that is washing the credit card industry away over years not months, and that’s why the opportunity has persisted for so long and can go further. Because it is long term. It persists beyond the usual two-year forecasting horizon of the stock market system. It was the same in the resources boom. BHP didn’t go from $7 to $40 in a day, it did it gradually over six years.

The stock market never prices in the long term. Some of the best opportunities for investors over the next few years aren’t necessarily going to come from some wild unimagined left field technology or trend, but, if best means the most predictable opportunity with the lowest risk, will come from long-term trends, that are already in place and will outlast the short sightedness of the typical research time frame.

So where are the long term, still exploitable, waves rolling through the stock market at the moment? I see the revival of the travel sector as a prime example and rather than kill the industry, the chances are that companies like Qantas will one day look back at the pandemic and thank their lucky stars. It obliterated the competition and ingrained their market dominance. The share prices of companies like Flight Centre, Webjet and Qantas, will, one day, recover and improve. But it will take years. That’s why nobody buys them, and that’s why you should.

Reece Birtles, Martin Currie Australia

Chief Investment Officer

Worley to benefit from decarbonising the economy

For us, decarbonisation is a huge opportunity for value investors. More and more Australian companies are now committed to net zero carbon emissions, but the investment opportunity comes from ‘how to get there’ rather than in the energy companies themselves.

In order to achieve these carbon targets, the capex required in energy transition is in the order of 10 times the amount that had been previously spent on capex for oil and gas. An attractively valued company that is well positioned to capitalise on this theme is engineering, advisory and project management services company, Worley. While Worley’s revenues and share price have historically been highly correlated to oil and gas prices and industry capex spend, they are now pivoting to providing services to renewables projects such as wind and solar. Revenue from the renewables space is expected to more than replace their traditional oil and gas work as the world transitions to a lower emission future.

Worley is also at the cutting edge of adopting new technologies to significantly bring down the carbon emissions of their clients. An interesting example is the technological breakthrough they have made to literally take carbon out of the air, which they are implementing for a large US client.

Shane Miller, Chi-X Australia

Chief Commercial Officer

Active and theme ETFs deliver advantages

The best opportunity for investors over the next few years remains the same as the best opportunity for investors over the past few years – Exchange Traded Funds (ETFs). In a single transaction on exchange, ETFs provide access to diversification, liquidity, two-day settlement, low cost and transparent passive management for a broad range of investments.

The opportunity set in ETFs will only increase over the next few years. Almost every investment theme you can think of will have its own ETF – ESG, climate change and renewable energy, cloud computing and cybersecurity, artificial intelligence and machine learning, emerging markets, small caps, high growth, low interest rates and more.

What more? Active ETFs are here, and more are coming. A large number of managed funds will soon be available on-exchange, providing access to the same investment opportunities with active management. The same advantages of passive ETFs apply - portfolio diversification, on-market liquidity and two-day settlement. Also, transparency since active managers need to disclose their full portfolio to the listing exchange (Chi-X and ASX), usually on a delayed basis. Finally, expect lower costs, as active managers compete for market share with passive ETFs.

Ilan Israelstam, BetaShares

Head of Strategy

Transformational trends as the world changes

The most popular form of passive investment funds historically has been those benchmarked to indices where stocks are weighted according to their market cap.

However, today’s investor has a far wider range of investment approaches to choose from. We believe that the best opportunities for investors over the next few years are to be found in funds that take a thematic approach.

Thematic investing involves trying to identify long-term transformational trends, and the investments that are likely to benefit if those trends play out. Such investments are typically agnostic to industry sectors, or geographical boundaries.

Thematic investing focuses on structural, rather than cyclical trends - themes that tend to be one-off shifts that irreversibly change the world, driven by powerful forces such as disruptive technologies or changing demographics and consumer behaviour.

One trend we think is likely to be durable and long term is the continued adoption of the cloud, which is arguably one of the most significant business transformations we have seen since the early days of the world wide web. Given ongoing growth in online activity, and the sizable share of the world’s digital data and software applications still maintained outside of the cloud, we expect to see demand for cloud-related services to increase for many years. Our recently launched Cloud Computing ETF (CLDD) is designed to provide exposure to this theme.

We think that a focus on themes such as cloud computing, climate change innovation, cybersecurity and robotics/artificial intelligence offers significant potential for investors taking a long-term view.

Chris Stott, 1851 Capital

Chief Investment Officer and Portfolio Manager

Flight Centre and Corporate Travel to bounce back

One of the most beaten-up sectors through the COVID-19 pandemic which we believe provides the most upside for investors in the coming years is travel. The travel sector has been the most negatively-affected across the economy but it is now positioned for one of the largest travel booms we have ever seen. For travel companies that have survived, they have significantly adjusted their cost bases lower and are positioned for enormous operating leverage as revenue recovers.

There are large levels of pent-up demand from consumers and businesses keen to get back in the air. With the acceleration of the COVID-19 vaccine roll out, particularly in offshore markets, the early signs are very positive. In markets that have re-opened earlier such as China and New Zealand, domestic travel has bounced back sharply. The recently announced $1.2 billion federal stimulus package for the travel sector will only add fuel to what we believe will be a watershed few years for the industry. We believe for Australian investors, Flight Centre (FLT.ASX) and Corporate Travel Management (CTD.ASX) are the best exposures to this thematic over the coming years.

Bill Pridham, Ellerston Capital

Portfolio Manager

PTC in a focus on recycling

We believe a nascent, yet powerful, megatrend over the coming years will be associated with companies investing in, and addressing, the use of finite resources as they shift towards a circular economy model.

Over the past several decades our society has adopted a ‘throw away’ culture where goods (primarily consumer electronics and plastics packaging) are used once and discarded into landfills. The World Economic Forum (WEF) estimates that based on our current ‘take-make-waste’ habits it requires the equivalent of 1.7 Earths to replenish the resources consumed and absorb the pollution created. This is not sustainable.

By adopting a circular economy mindset, the WEF estimates US$4.5 trillion of global growth potential could be unleashed. There is certainly an economic incentive for corporates to adopt this mantra.

To enable the circular economy, we believe a digital thread (Industry 4.0) is necessary to manage products and assets from design through to end of life. Approximately 80% of a product’s environmental impact is determined during the design process.

PTC is a global leader in CAD and PLM software (product design and life cycle management) and maintains the dominant position in Industrial IoT platforms which power many Industry 4.0 strategies across the globe. We consider PTC as a prime long-term beneficiary of this megatrend.

Ama Seery, Janus Henderson Investors

ESG Analyst

Focus on sustainable design

The best opportunity over the next few years is intentional sustainable design. In this context, I am referring to design that addresses sustainable development. This is different from environmentally sustainable design or eco-design, which have a strong focus on environmental considerations.

It is an indication that a company is intentionally addressing environmental and social issues through the design of its products and services as well as its operations. It is this intentionality that is used as part of the evidence of positive impact. I believer that R&D that is focused towards environmental and social issues is evidence of continuous improvement and an indicator for growth.

As consumers become more aware of the impact of the services and products they use on the environment and society, companies must adapt and transform their business models to cater to this demand. Sustainable design is a large investment opportunity driven by the rise in demand for sustainable goods and services.

Nandita D’Souza, Citi Australia

Head of Investment Specialists

Investors need better education on opportunities

Investor education is a huge opportunity for investors. Currently, Australian investors remain invested in only a few asset classes: typically cash, property and shares. The biggest barrier to their investing in other classes is lack of knowledge. With record low interest rates, a skyrocketing property market and volatile share market, there are compelling reasons for investors to learn how they can diversify further. This includes across geographies and currencies, by employing a hedge into their equity investments, or looking to additional asset classes like fixed income.

Not only will education provide more opportunities, but it will empower investors to make smarter decisions around their investment strategies or portfolio. For example, while many may think rising yields mean fixed income investments are bad, investors in the know would be exploring shorter duration or floating rate bonds. Similarly, if an investor thinks equity valuations are too high, they don’t have to feel like their only option is to sit on the sidelines and stay in cash.

There are mechanisms like structured products that allow investors to access equities while hedging their downside. Looking at our property market, investors who are priced out, concerned about an illiquid asset or averse to REITs because of volatility can look at bonds in a company like Scentre as a way to get exposure to property in a stable and liquid investment.

For too long, Australian investors have been missing out on opportunities like these, and a key reason is lack of awareness that these options exist. While these investments may add a layer of unfamiliarity or complexity, they also have the potential to increase returns, hedge downside risks and give investors more ways to make their money work.

John M Malloy, RWC Partners

Co-Head of Emerging and Frontier Markets

USD to remain at weaker levels

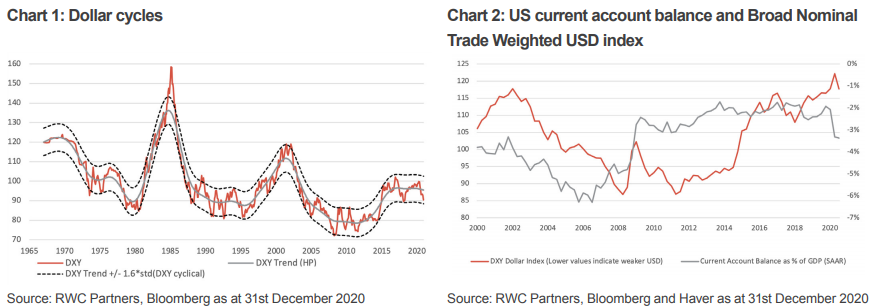

There are many supportive tailwinds for emerging markets in 2021 and beyond. A post-pandemic recovery in global demand coupled with USD weakness will likely boost emerging market assets through rising capital flows, lower global uncertainty and stronger emerging market growth.

A weaker USD strengthens balance sheets in emerging markets, particularly for those with higher external debt ratios, and further eases financial conditions. Based on our analysis, the USD may settle at a new long-run level about 12% to 15% weaker than the level at the start of the current pandemic back in April 2020. This would imply an additional 8% or so decline in DXY (USD Index) from December 2020 levels. It is difficult to predict the pace of the decline but we think that a significant part of it may take place over the next two to four quarters. This weakness is largely due to the continuation of rising US external imbalances and the normalisation of global risk premia: tariff-related uncertainty, growing concerns of deglobalisation and rising geopolitical risks.

The U.S. current account deficit will re-widen going forward as fiscal and monetary accommodation will be maintained for the foreseeable future, with the dynamics already in motion with recovery in imports outpacing exports and the current account deficit widening from 1.9% of GDP at end-2019 to 3.4% in Q3 2020 (a 71% increase in actual dollars).

Chris Cuffe, Third Link Growth Fund

Founder and Portfolio Manager

Patient investors can benefit from private debt

Private debt is a significant subset of broader credit markets, often resulting from private equity, securitisation and direct lending activities across various assets pools and corporate borrowers. Generally, private debt loans, as the name suggests, do not trade on open markets and hence are usually very illiquid (except for some asset-backed securities). Once a loan is made it is typically held to maturity, with terms generally ranging between one and five years, with varying repayment profiles.

Due to its illiquidity, private debt as an asset class will not suit all investors. But for a patient investor with a longer-term investment horizon, who is less concerned about liquidity and seeks attractive income returns, private debt funds can provide a good risk/return trade off versus high-yield bonds, for example.

Typically, private debt funds, depending on their risk profile and security exposures, may yield between 5% - 10% per annum. While 'high yield' has generally been synonymous with high risk, this is mitigated somewhat if a focus is taken on senior secured investments with strong asset or cashflow backing them. Senior secured investments rank in priority to other creditors or equity – particularly listed equity - for liquidity and payment. With a diversity of underlying collateral, private debt markets deliver opportunities for experienced credit managers.

Australian-based providers of private debt who I have invested with include Revolution Asset Management, PIMCO, Merricks Capital, Longreach Alternatives, Aquasia, Causeway Financial, Pure Asset Management, Realside Financial Group and Ventra Capital (the last two of which I am also a shareholder and director of). And there are many more in this growing market that I have not met.

Anton Tagliaferro, Investors Mutual

Investment Director, Co-Portfolio Manager of QV Equities (ASX: QVE)

Predictable and strong businesses pay off over time

The best opportunity for investors over the next few years will be to own a diversified portfolio of good quality companies in a variety of sectors and industries. It’s important to select companies at time of purchase which are underpinned by reasonable valuations. History has shown that this produces far better and more consistent returns than chasing the latest ‘hot’ stock or sector.

There are many very good quality companies in the sharemarket. We always have a preference for well-established companies that we believe have an enduring competitive advantage, are run by experienced, honest and competent management teams, which have produced a track record of recurring revenues and earnings, and which are trading at reasonable prices. These companies also tend to be the ones able to pay consistent and reliable income over time to investors.

One example is Amcor, one of the largest global packaging suppliers with diversified operations around the world. The majority of its sales are to defensive consumer goods companies such as Unilever and Pepsi, which enables Amcor to produce relatively predictable earnings even in times of economic uncertainty. Amcor also has a strong balance sheet, pays a good dividend, and is using its strong cashflows to undertake a share buyback and expand further globally.

Successful long-term investing will always be about looking beyond daily headlines, remembering the difference between speculating and investing, and recognising there can be a difference between a company’s share price and its underlying value. Time and again over my three decades in the sharemarket, focusing on the fundamental value and quality of a company has enabled our portfolios to produce reliable income and long-term capital growth while achieving returns which are more consistent and less volatile than the overall sharemarket.

Mike Murray, Australian Ethical

Head of Domestic Equities

Healius and Genworth tap into ethical themes

The pandemic and its economic and social impacts have fuelled interest in ethical investing. Companies are being held to a higher standard in a range of areas from carbon emissions to labour standards and corporate governance. We don’t see these trends changing and if anything, they have stronger political impetus with COP26 later this year and the US re-entering the Paris agreement.

Our portfolios are broadly exposed to these long-term themes which align well with our core beliefs as an ethical fund manager – as you would expect our equities funds are invested in sectors such as healthcare, technology and renewables. However even within the sectors that benefit, there will be winners and losers and so a lot of our research effort goes into bottom up analysis of companies, their management teams and whether they are trading at reasonable valuations.

One of the companies we like in healthcare is Healius which has played a major role in COVID testing but also has a very defendable core diagnostic business and the potential for higher margins through time. Another company we like currently is Genworth which provides lenders mortgage insurance. It trades at a discount to its book value and ought to be a beneficiary from the recovery in local housing markets.

Daryl Wilson, Affluence Funds Management

CEO and Portfolio Manager

Small company funds and LICs offering value

We're contrarians at heart. We love investing in things that are unloved and cheaper than average. Right now, plenty to opportunities meet that criteria. Our best idea is to invest into one particular subsector of the market where several undervalued opportunities converge. An investment allocation to Australian small and micro-cap value stocks combines three areas where we feel there is above average value.

Firstly, this idea backs Australian stocks over global stocks. The ASX has lagged US market returns substantially over the past 10 years. But with our economy much better placed than most for the medium term, it's time for the ASX to shine. Plus, if you invest locally, you get the extra benefit of franking credits.

Secondly, we much prefer value stocks over growth right now. The price gap between these two is as extreme as it's ever been, with the possible exception of the tech bubble in 2000. And we know what happened after that. We feel the turning point for value stocks has finally arrived.

Finally, we've seen a big drift towards investing in large caps in the last 10 years, helped by the popularity of passive investing. A lot of smaller companies have been left behind. There are plenty available at very attractive prices, including many on single digit earnings multiples. So it makes sense to focus on small and microcap companies.

So, look to add some Aussie small cap value stocks to your portfolio. What's the best way to do it? We suggest rather than go it alone, that you can execute this idea the same way we do. By investing in a number of different unlisted funds and LICs that focus on ASX small cap value stocks. By accessing more than one fund manager in this space, you're diversifying and probably lowering the risk. As some examples, unlisted small cap value funds we currently hold include Phoenix Opportunities, EGP Capital, Wentworth Williamson, Cyan Capital 3G and Terra Capital Natural Resources. Small cap value LIC's we own include Spheria Emerging Companies, Sandon Capital, NGE Capital, Ryder Capital and Thorney Opportunities. There are a range of other great small cap value managers out there to choose from.

These are far from the only investments we own but they represent one of our largest total exposures. Collectively, we think this strategy provides the potential for strong double digit returns over the next few years.

Oliver Hextall, Fidelity International

Co-Portfolio Manager, Fidelity Global Demographics Fund

The rise of automation

We spend a lot of time thinking about the major themes which will impact investors. Our whole philosophy is centred around finding companies with innovative products and services that will help address the world’s evolving demographic needs.

A theme I think that’s particularly interesting at the moment is automation. From a ‘demographic lens’ automation has a huge role to play in both the aging population and population growth, but it also has an interesting sustainability angle as we look for efficient ways to use our resources. And it’s a trend which has been accelerated by COVID-19.

The world’s population is both growing and ageing and this will pose problems in how the supply of goods and services can grow sustainably and efficiently to meet rising demand. Automation is an important part of the solution. Deploying automated technologies can reduce unit costs over time, use resources more effectively and with less wastage, and free up workers to focus on higher value activities. Currently, there’s a wide range of robot density in manufacturing across different countries and industries but we expect this gap to close over time and the industry should see good growth as penetration increases.

Automation will also benefit from key themes currently driving growth around the world. For example, electric vehicles will require additional robots for battery, inverter and motor assembly; the rollout of 5G will require greater automation in manufacturing as complexity increases; and feeding a growing population sustainably will require greater deployment of precision agriculture equipment.

As a result of COVID-19, we also expect the rise of automation to accelerate as companies increasingly look to insulate their production processes from worker sick days or enforced social distancing, and to diversify supply chains.

Kej Somaia, First Sentier Investors

Co-head of Multi-Asset Strategies

Think beyond active versus passive: why not have both?

The market has been good to passive investors in recent years, as the rising tide of performance has lifted all boats. It might be tempting to think active management is passé, but as the world reconfigures itself post-COVID, it will be awash with stimulus-driven capital looking for a home. And with interest rates so low, active management may be needed for investors to meet their income and growth goals.

You may have heard some active managers called a ‘closet indexer’, meaning their results are close to market returns (but with higher fees). But what about a ‘closet active manager’: someone who believes they are investing passively, but makes significant calls on asset allocation? Which is, after all, the dominant driver of overall portfolio outcomes.

We believe you can have both active and passive approaches in a broader portfolio. For example, our team passively replicates most of the large market exposures in a portfolio, such as global developed market equities or global government bonds.

Then, this passive exposure is buttressed with selective active sleeves in areas that have historically been much less efficient, like small cap Australian equities, or areas where high levels of diversification are desired, such as global investment grade credit.

With this ‘best of both worlds’ approach, investors can manage their investment costs without forgoing the alpha that’s needed to generate attractive returns.

Dr. Stephen Nash, BondIncome

Specialist Partner

Bond sell off opens portfolio protection

Most Australian SMSF portfolios have a problem, with too much reliance upon equity risk and a lack of diversification into long-dated fixed rate debt. Picking the next decline in equity prices is almost impossibly difficult. Investors have no alternative but to rely on better portfolio construction, not hubris and bravado. If one values a better retirement, then one needs to get serious, and think about how a major decline in equities might impact that retirement.

A decent allocation to long-dated government bonds in a crisis cushions growth asset volatility. Sure, there is a cost of having these bonds; a failure to load the portfolio with growth assets and the prospect that one might have not squeezed every cent out of the current rally in equity prices.

However, prudence, as Aristotle tells us, being the art, not the science, of making decisions in situations of imperfect information, requires that sound portfolio construction be prioritised against both the latest short-term fad and short-term greed. The recent rise in long-dated government yields represents an opportunity for diversification, not a threat.

With a very large amount of federal government stimulation rolling off at the end of March 2021, the economy faces a moment of truth. The economy should pull through, but if difficulties arise, portfolios will be desperately seeking more diversification into fixed income.

Vince Pezzullo, Perpetual Investment Management

Deputy Head of Equities and Portfolio Manager (including ASX:PIC)

Position portfolios for the reopening

The broad economic backdrop continues to be a complex mixture of opportunities and risks with the Australian and US economies recovering ahead of expectations. A dramatic steepening in the yield curve - with both Australian and US 10-year bond yields spiking but official cash rates staying near zero - has sparked a large rotation in equity markets. Expensive growth stocks have been crushed whilst value stocks, like many in the PIC portfolio, that are geared to economic re-opening have enjoyed a bounce.

However, other risks such as inflation are will also present themselves this year. COVID-19 virtually shut down global production in 2020, but demand was sustained through extraordinary stimulus measures from governments around the world. As companies ran down their spare inventories, a mixture of supply dislocations and trade tensions has led to long waits for new consumer goods. As factories struggle to get production back online and rates for transportation and logistics surge, we believe the economy will likely experience a bout of inflation.

There are also fears that the massive new US$1.9 trillion stimulus delivered by the US Congress is ‘too much, too late’ in the cycle as consumer demand roars back to life. Like the stimuli in 2020, this is not indirect monetary stimulus likely to be trapped in bank reserves but a ‘hard money’ fiscal injection, delivered directly into the hands of consumers with a high propensity to spend it.

Hamish Douglass, Magellan Asset Management

Co-Founder, Chairman and Chief Investment Officer

This is the most complex risk environment the world has seen for many years. To get a sense of what could go wrong, imagine recent times as a Netflix series.

Season 1 would be titled The Pandemic. The series would track the outbreak of the influenza pandemic that started in Wuhan in China. Season 1 made viewers edgy until the final episode when global euphoria broke out and stock markets roared after scientists defied expectations and found a powerful vaccine to defeat the virus.

Season 2 is where we are now, The Year of Living Dangerously. While the director has commenced filming Season 2, the ending is still being decided. The director has instructed two teams to write different scripts.

One option is subtitled The Awakening and it’s a celebration of the ability of the vaccines to end the virus. This series documents how society and economies recover from the pandemic but it too has two different endings. One is a relatively smooth ending with a rapid but controlled economic recovery. This would be a nirvana outcome for financial markets.

But the alternative ending is not so happy. Excessive stimulus leads to a lasting outbreak of inflation that triggers the next worldwide downturn as central banks abruptly raise interest rates. This would be a nasty shock for financial markets. The alternative script for Season 2 is subtitled The Mutant Strain. This plot is a dark tale of how a variant of the virus emerges that evades the vaccines and sets the world and financial markets back.

The plots outlined are possibilities yet there is little risk priced into markets at the moment. That makes the next 12 months a dangerous time for investors.

***

For a copy of the ebook, download here

For a copy of the ebook, download here

Disclaimer: The data, research and opinions provided here are for information purposes; are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate.

Morningstar, its affiliates, and third-party content providers are not responsible for any investment decisions, damages or losses resulting from, or related to, the data and analyses or their use. Any general advice or ‘regulated financial advice’ under New Zealand law has been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs. For more information refer to our Financial Services Guide (AU) and Financial Advice Provider Disclosure Statement (NZ). You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement before making any decision to invest. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. This content is current as at date of publication.

This document contains information and opinions provided by third parties. Inclusion of this information does not necessarily represent Morningstar’s positions, strategies or opinions and should not be considered an endorsement by Morningstar.