The current geopolitical tensions across the globe including Brexit, trade war fears, changing global allegiances driven by the Trump administration, and the recent US government shutdown, have caused a new level of disruption and noise. However, it is not all bad news as we begin to see pockets of improvement in the world economy.

Growth in the US is helping to sustain the global economy. Meanwhile, closer to home, Australians have been fortunate to experience stable employment growth and in general, corporate balance sheets are in good shape.

Investors face a challenging time when it comes to portfolio construction. After years of slow economic growth and low interest rates post-GFC, we have recently seen rates rise in the US, but investors should pay close attention to the risks taken in their portfolios to obtain the necessary income. Given the RBA cash rates is just 1.5%, sitting on cash is not a long-term solution for real sustainable income.

We believe fixed income can provide a more stable source of income given mandatory coupons, and global high yield corporate bonds represent an attractive asset class for investors searching for a diversified source of income.

As an asset class, global high yield bonds have historically been mired in confusion, so let's explore why it is worth considering them.

1. Global high yield bonds have evolved

Mention ‘high yield bonds’ and some investors will label them as ‘junk bonds’. This was an apt description in the 1980s, when small and speculative companies dominated the sector, but the market has matured dramatically since then.

The high yield market has now evolved into a financing mechanism widely used by companies with sound fundamentals looking to diversify their funding mix away from pure bank debt or shareholder equity. There are now more than 2,000 companies in the market, which has grown from less than US$200 billion in the 1980s to approximately US$2.8 trillion today. These include household names such as Netflix, Hertz, Fiat and Mattel, as well as numerous important players in the telecom and internet industries. All these companies have significant revenue and profit streams to service their high yield debt, and the label of 'junk bond' is no longer suitable for many of them.

2. Bond allocations need to be diversified

There are important fundamental principles in building an allocation to bonds. The allocation should lower risk and stabilise returns, offsetting the more volatile performance of equities and creating a steady income stream within the overall portfolio.

While traditional bonds provide diversification, they are more susceptible to interest rate fluctuations than global high yield bonds, which tend to be linked to corporate credit fundamentals. High yield bonds provide attractive returns and a lower risk profile than equities, making them an intermediary diversification tool within a traditional portfolio.

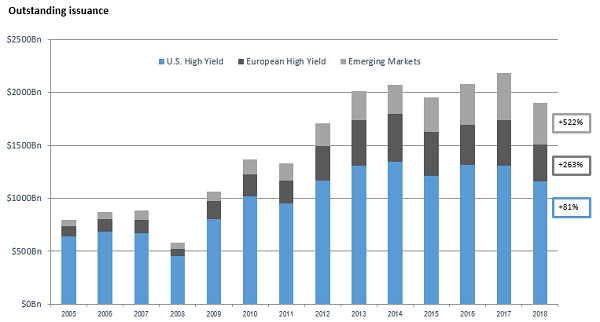

Global high yield bonds also offer geographic and sector diversification. While the US still dominates this market, companies from Europe and emerging markets across a wide array of industries issue high yield bonds. The market offers meaningful global exposure for investors looking for diversification, as shown in Figure 1.

Figure 1: European and Emerging Market high yield bond issues are growing fast

Click to enlarge. Source: Bank of America Merrill Lynch. Universe represented by the Bank of America Merrill Lynch Global High Yield Index. Emerging markets defined as issuers with a country of risk other than an FX-G10 member, a Western European nation, or a territory of the US or a Western European nation. US High Yield represents non-EM USD HY bonds. European High Yield represents European currency HY bonds. Data as of December 31, 2018.

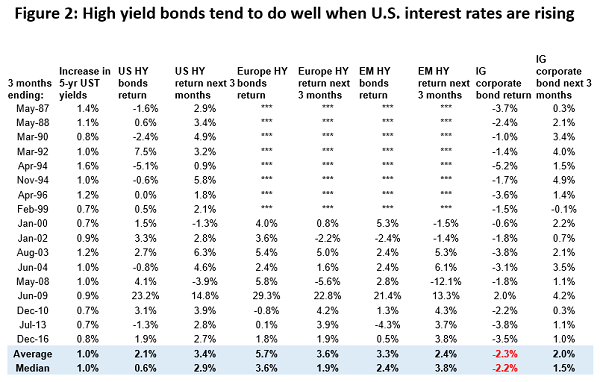

3. Global high yield bonds generally perform strongly during periods of rising interest rates

While it is true that rising interest rates can cause falls in the value of bonds, the global high yield market has different characteristics to traditional long-dated government bonds and investment grade debt, with which investors are more familiar.

Historically, high yield bonds have performed well in rising interest rate environments, when the economy is doing well. There is usually growth in company earnings and overall improvement in corporate fundamentals. Consequently, credit risk for companies decreases, resulting in lower default rates.

High yield bonds performance in rising rate environment

Click to enlarge. Source: Bank of America Merill Lynch. BofAML US High Yield Master II Index; BofAML European Currency High Yield Index; BofAML High Yield Emerging Market Corporates Plus Index; BofAML US Corp & Govt Master Index. The table presented above represents performance when 5-Year Treasury yields rose 70 basis points (or more) during a 3-month period. The periods are the three months ending in Jan 2000, Jan 2002, Aug 2003, Jun 2004, May 2008, Jun 2009, Dec 2010, Jul 2013 and Dec 2016. IG=Investment Grade.

For the past few years, central banks have set interest rates at historically low levels, but they have started to move back to what is considered normal or ‘neutral' settings. This recent trend is in stark contrast to the days when central banks were regularly hiking rates aggressively to slow economic growth and cap inflation. For corporates with fundamentally good balance sheets and trading prospects, the return to neutral interest rates has been a positive change.

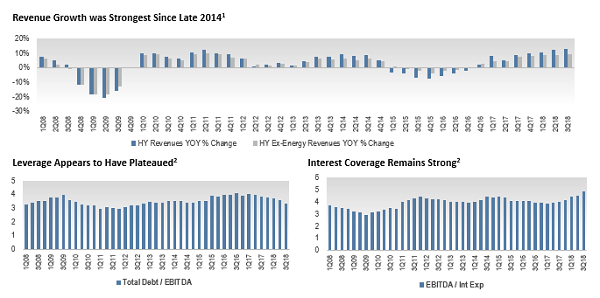

High yield market fundamentals

We believe the probability of a near-term recession is low and while volatility is likely to persist, valuations for high yield bonds compensate investors for the modest default risk. The operating performance of underlying issuers has been stable; revenue and EBITDA growth have improved as leverage has plateaued, and refinancing activity has significantly reduced the number of bonds maturing in the near term.

However, global high yield bond markets are susceptible to a variety of factors, including uncertainty around government disruptions such as aggressive rhetoric, trade policy and the overall regulatory environment. Below-average new issue supply of high yield bonds continues to be supportive, and we expect issuance to remain flat year-on-year during 2019.

Figure 3: High yield market’s credit quality improvements

Click to enlarge. Source: Bank of America Merrill Lynch. Data as of September 30, 2018. Adjusted metrics are calculated using Adjusted EBITDA which removes the impact of unusual items from earnings including but not limited to non-recurring items, impairments, goodwill etc.

An under-recognised asset class

In Australia, global high yield has traditionally been an under-represented asset class, and not one easily accessible to investors or SMSFs. By providing exposure to global credit markets, an allocation to global high yield bonds can provide diversification benefits to a domestically-biased portfolio and improve the overall risk profile.

Vivek Bommi is a Senior Portfolio Manager at Neuberger Berman, a sponsor of Cuffelinks. This material is provided for information purposes only and does not constitute investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. It does not consider the circumstances of any investor.

For more information on Neuberger Berman, please click here.