Since the $3 million super tax became law in March, one word has carried the industry's entire message: 'protect'. Make the cost base reset election and you 'protect' the gains your fund built before July. Miss it and decades of growth are 'exposed'. The word worked. Adviser notes spent June urging trustees to commission valuations before the deadline, and pointing out that the only way to keep an asset out of the election was to sell it first. But the arithmetic under the slogan says something quieter: for a typical affected member, 'protecting' $1 million of gains is worth about $25,000. Real money. Also two and a half cents in the dollar, arriving years from now, and only if you are still over the threshold when you finally sell.

The panic also got the calendar wrong. The date that mattered on 30 June was the valuation, not the decision. The election itself is made on an approved form any time up to the due date of the fund's 2026-27 annual return, so trustees have the better part of a year to choose, working from a number that is now fixed. The photograph has been taken. Whether to hand it to the tax office is still an open question, and this article is the arithmetic for answering it.

What Division 296 actually taxes

Division 296 took effect on 1 July. It adds 15% tax on the share of a member's super earnings attributable to the portion of their total super balance above $3 million, with a further 10% above $10 million. Three design details do all the work in what follows.

First, it taxes realised earnings only: dividends, interest, rent, and capital gains when assets are actually sold. Paper movements no longer count, which is the concession that made the final law palatable. Second, capital gains keep the one-third discount for assets held longer than 12 months, so at most two-thirds of any gain enters the calculation. Third, and least understood, only the proportion of earnings matching the proportion of the balance above the threshold is taxed. A member with $4 million has a quarter of their balance over the line, so a quarter of their earnings wear the extra 15%. Pension phase does not help; earnings that are exempt from ordinary fund tax are counted back in.

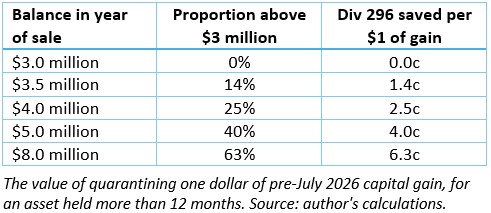

Multiply the three together and the most a dollar of capital gain can cost in Division 296 tax is 10 cents, rising to 16.7 cents only for the slice of a balance beyond $10 million; a ceiling approached only by very large balances. On the way down, the proportion shrinks it quickly.

The reset, in cents per dollar

The transitional election lets an SMSF (and other small funds) treat the market value of every asset it held directly on 30 June 2026 as a fresh cost base, for Division 296 purposes only. Ordinary capital gains tax is untouched. Gains accrued before this month then never enter Division 296 earnings; only growth from here does. The election is made at fund level, covers every asset or none, and once made cannot be unwound. So, what is a quarantined dollar of gain actually worth? The saving is 15% of two-thirds of the proportion over the threshold. In cents:

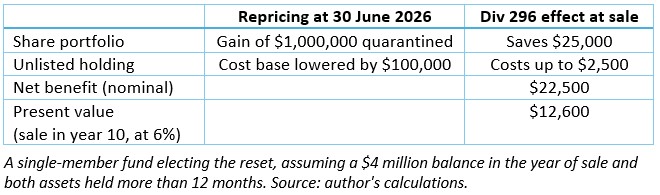

Now a worked example. A single-member fund with a $4 million balance holds a share portfolio bought for $600,000 and worth $1.6 million on 30 June: an accrued gain of $1 million. It also holds an unlisted investment bought for $500,000 and now worth $400,000. Elect, and the share gain is quarantined; at a 25% proportion that saves $25,000 of Division 296 tax in the eventual year of sale. But every asset means every asset. The loss position resets too, its cost base falling to $400,000, so if it merely climbs back to what was paid for it, $100,000 of recovery is counted as new gain, costing up to $2,500. Net benefit: about $22,500. And if the sale is a decade away, nearer $12,600 in today's dollars at a 6% discount rate.

Notice where the $1 million sits in that table: the middle column, never the last. The reset does not protect gains. It removes a slice of a tax on a discounted fraction of them.

The honest case for electing anyway

For most funds sitting on net gains, consider electing. The election costs a form, the 30 June valuation was needed for the fund's accounts regardless, and the option runs one way: fail to opt in by the return's due date and that door closes for good. A free option with an irreversible expiry should usually be taken. That asymmetry, not fee-hunting, is why the adviser notes pushed so hard: recommending against a free irrevocable option is the kind of call nobody wants to defend later. And for the funds the tax was aimed at, the cents add up. A $2 million property gain in an $8 million balance is roughly $125,000 of Division 296 tax, which pays for a great deal of paperwork. The cents-in-the-dollar framing sizes the decision. It does not dismiss it.

What it does dismiss is the gymnastics. Selling assets purely to reshape the fund before the photograph, round-trip disposals to crystallise gains (wash sales by another name, and the ATO has a long-standing dislike of those), restructures priced in the thousands to defend tax measured in the hundreds. At a $3.2 million balance, quarantining $100,000 of gain is worth $625. June offered plenty of ways to spend more than that achieving it.

Who actually needs the arithmetic

Members over $3 million should model the netting, gains against loss positions, and elect calmly inside the year they have. Members under it are being told to elect 'just in case', and the free-option logic supports that, but the trajectory deserves arithmetic rather than fear. The threshold is indexed in $150,000 steps, and a pension balance drawing 5% while earning 6% grows about 1% a year while the threshold compounds with inflation. The gap widens. Many drawdown funds will never cross the line, and their reset will simply never matter. The genuine 'just in case' cases are younger accumulators with large balances and years of contributions ahead. Members of large APRA-regulated funds have no election to make; their funds receive separate transitional treatment, and there is nothing to do. One caveat throughout: the supporting regulations were still in draft at the time of writing, so administrative details, including exactly how balances are valued, may yet move.

The election is worth making for most funds and worth panicking over for almost none. The photograph was taken on 30 June. Your fund has until its next tax return to decide whether it belongs in the frame.

Trevor Schmid has more than 20 years’ experience across superannuation, financial advice and member education. This article is general information only and does not consider any individual’s objectives, financial situation or needs.