Europe has been propelled into a profound transformation. Ongoing security threats and pressure from the US administration have prompted greater resolve from EU (European Union) member states to take more control over their future. This is a transformational change for Europe and forms part of a larger trend we refer to as the Great Global Restructuring.

The steps being taken are EU-wide as well as at a country level.

The emerging picture of Europe is one of a continent moving away from the constraints of past austerity and towards a more proactive strategy grounded in investment, industrial renewal and enhanced economic security.

This ‘pivot’ from austerity to expansion is evident in EU-wide initiatives such as the Clean Industrial Deal and fiscal flexibility measures, alongside country-level programs like Germany’s trillion-euro investment plan. These changes aim to enhance competitiveness, energy security, and resilience amid geopolitical uncertainty.

While execution risks remain, some estimates suggest the combined effect of these measures could add between 0.25% to 1% p.a. to EU GDP (gross domestic product) over the medium term.

EU-wide initiatives and structural shifts

The European Commission’s transition from the Green Deal to a Clean Industrial Deal signals a pragmatic shift toward competitiveness and energy security. This evolution reflects Europe’s entry into an era of geoeconomics, where trade, defence and energy policies are deeply interconnected.

The Commission’s proposal to integrate international carbon credits under Article 6 of the Paris Agreement could reduce decarbonisation costs for heavy industry. With CO2 prices projected to rise from €70/t today to €100 – €130/t by 2030[1], incentives for green capital expenditure are strengthening, particularly in carbon capture and hydrogen technologies. These changes could mean climate policy becomes a central growth driver.

Fiscal governance has also adapted. While the NextGenerationEU (NGEU) Recovery Fund (launched in 2020 to repair the damage from the COVID pandemic) remains a cornerstone, new fiscal flexibility rules allow member states to increase defence spending and strategic investments without triggering excessive deficit procedures. Examples include carve-outs that permit defence spending of up to 1.5% of GDP over four years starting in 2025[2]. This structural shift underscores the EU’s commitment to balancing fiscal prudence with strategic imperatives.

Next year, Spain and Italy are likely to see expenditure under the NGEU Recovery Fund rise to its highest level since 2021. Current plans suggest spending will rise to 1.5% to 2% of GDP. In fact, looser fiscal policy (example measures include lowering interest rates and purchasing securities to boost the economy) across EU member states is expected to support higher growth in 2026.

Country-level reforms and stimulus

While fifteen countries submitted draft budgets in October 2025 that indicated a net loosening of policy, Germany accounts for the bulk of the fiscal expansion.

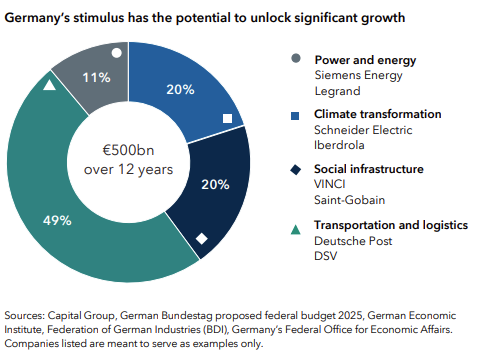

Germany’s pivot is the most striking example of this new paradigm. Abandoning its traditional austerity stance, Germany’s €900 billion to €1 trillion investment program[3] marks a strategic effort to reshape its economic foundations and boost long-term competitiveness.

Among the investment areas earmarked are €107 billion to rail and €52 billion to roads to address critical infrastructure bottlenecks that have constrained productivity and trade efficiency. The €38 billion allocated to digitalisation signals a push to modernise industry and accelerate technological adoption, while the €100 billion climate and transformation fund underscores Germany’s commitment to sustainability and energy transition.[4]

Complementary measures such as corporate tax breaks worth €48 billion (2025– 2029) and annual energy price reductions of €14 billion aim to bolster household consumption and industrial margins.[5] The anticipated impact is significant. Together, these investments are likely to generate significant multiplier effects, stimulating domestic demand, attracting private capital and reinforcing Germany’s role as a growth engine with spillover effects across the EU.

However, execution risks, including inflationary pressures and political hurdles, must be monitored closely.

Geopolitics and trade dynamics

Europe’s economic strategy is unfolding against a backdrop of global fragmentation and strategic competition – key drivers of the Great Global Restructuring. The EU faces tariff uncertainty and supply chain vulnerabilities amid US-China rivalry. In response, Brussels is pursuing ‘de-risking’ strategies such as onshoring (the practice of relocating a company’s business back to its home country) and diversifying their production facilities, while negotiating trade deals to mitigate shocks. Greater strategic focus from the European region shows renewed dynamism and indicates a shift to a new growth model - one that focuses more on internal demand instead of export-led growth.

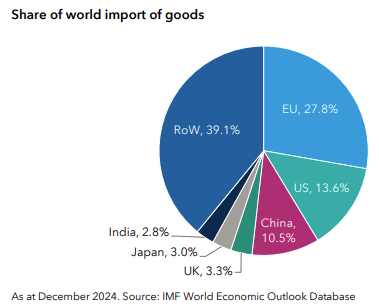

And internal demand in Europe is not insignificant. In fact, it is the largest single market importer globally, accounting for more than twice the proportion of imports as the US. This puts it in a relatively strong position to not only stimulate domestic demand and strengthen the businesses that serve it, but also to enhance its leverage in negotiating trade agreements with other countries.

RoW: rest of world

There is no doubt that tariffs imposed by the US have created a negative supply shock, however our analysis suggests the impact on the EU could be relatively modest in comparison with the effects on the US, China and their closest trading partners, e.g. Mexico and Canada.

There are three key reasons why Europe’s output may hold up even under the current tariff framework.

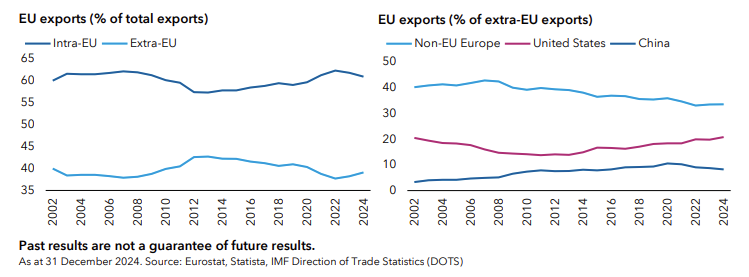

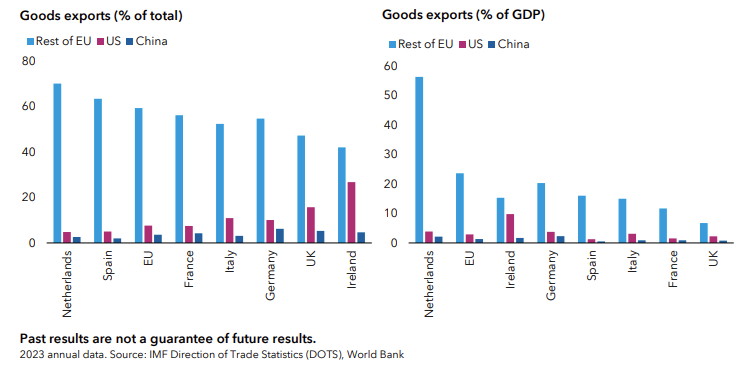

1. Goods trade with US is lower than widely assumed

A figure often cited is that the US accounts for 20% of EU goods exports. What is less publicised is that trade within the EU is substantially higher than trade flows with non-EU countries.

When total trade flows are considered, the US accounts for less than 10% of goods exports and less than 3% of GDP on average across EU countries.

Ireland is a relative outlier. However, its US exports are mostly concentrated in medical and pharmaceutical products and even this has fallen significantly since Trump’s first trade war in 2019.

2. Loss of market share could be limited

US tariff policy is yet to reach a steady state. Even so, the potential loss of EU market share may be less severe than feared.

The current tariff structure – a 15% tariff ceiling on most goods, with higher rates on steel and cars – is unlikely to prompt a large-scale reshoring of production away from Europe. Some US importers will absorb higher prices or pass them onto consumers. Some goods could be redirected to third markets, and certain lower value-added or energy-intensive industries may experience modest declines in output. But the overall impact on European producers should remain contained.

A key determinant here is how price-sensitive buyers are. There are different calculations for short-term and longer-term, with some estimates from the Federal Reserve suggesting that an effective tariff of 8.8% would decrease demand for EU goods by 1% in the short term, rising to 4% after six years. Yet even these figures could overstate the effect.

As European Central Bank Governing Council member Isabel Schnabel has noted, the bulk of EU goods imported into the US are in categories like pharmaceuticals, machinery and vehicles, which tend to be highly differentiated. This means the price sensitivity would be lower still, as buyers view them as difficult to substitute.

Several factors underpin this low elasticity:

- Highly specialised goods – A significant share of European exports consists of complex or bespoke products, such as pharmaceuticals, advanced machinery and high-end vehicles.

- Brand reputation – For instance, German automotive engineering or Swiss precision machinery carry strong consumer and business loyalty.

- Regulatory compliance – Pharmaceutical imports often rely on strict, long established regulatory approvals, making substitution costly and time consuming.

- Technical specifications – Many European machines are tailored to specific production processes, reducing the feasibility of swapping suppliers quickly.

Even where goods are perceived to be substitutable, in practice, switching takes time. Consumers typically maintain brand preferences, especially when price increases are modest. Businesses face entrenched supply chains, fixed contracts and high switching costs; reconfiguring procurement takes time and coordination.

In addition, some EU products entering the US market face reduced tariffs or exemptions. These often relate to:

- Public health needs, where many pharmaceuticals are exempt

- Critical infrastructure, such as specialist machinery

- Negotiated carve-outs, designed to avoid supply chain disruptions.

Taken together, these dynamics suggest the erosion of EU market share loss could be limited. In fact, if higher tariffs on China persist, European firms may even gain share in certain US market segments.

3. Increase in regional trade within Europe

There is considerable scope for the EU to trade more intensively with one another. Germany’s substantial fiscal policy loosening could support higher domestic demand both in Germany and across Europe. As outlined, the multiplier effect of the package could add 0.25% to 0.5% to EU GDP in the coming years and an additional boost could come from deepening the single market.

Forecasts suggest that domestic demand within the EU may become a more meaningful contributor to GDP going forward.

Another avenue for growth is to build closer trading relationships with non-EU countries. Two particularly strong candidates are the UK and India. Progress is already being make in the UK’s case. While the EU-UK trade deal struck in May 2025 was limited in scope, it laid the groundwork for future cooperation.

Cyclical backdrop

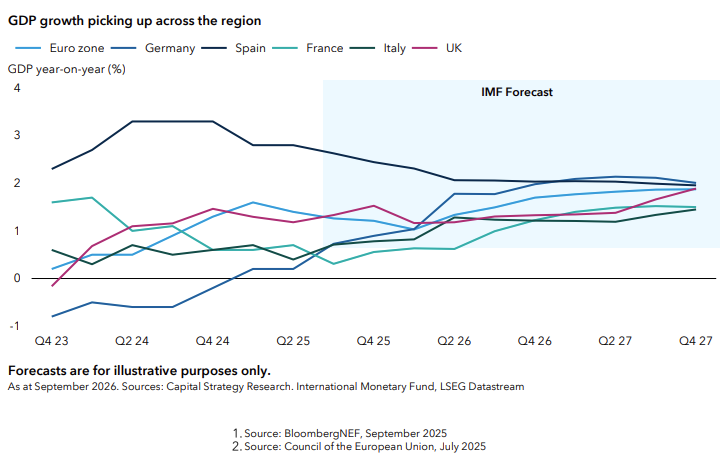

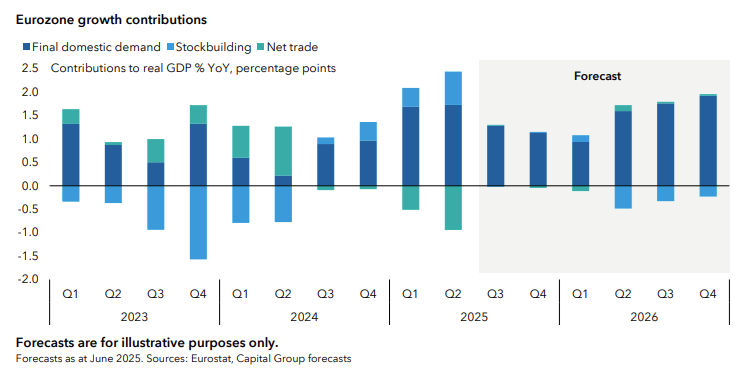

Encouragingly, we are beginning to see the effects of both Europe’s structural reset and its resilience to tariffs come through in economic figures.

Despite higher US tariffs and uncertainty, recent data releases have surprised to the upside. The eurozone grew by 0.2% (quarter-on-quarter) in Q3 2025, with France expanding by 0.5% (quarter-on-quarter) amid stronger business investment. Unemployment in the eurozone remained near its record low in September 2025 and interest rate cuts the European Central Bank (ECB) has made since June 2024 are increasingly feeding through to strong borrowing demand. Manufacturing and sentiment surveys also indicate encouraging results for the fourth quarter of 2025.[6]

The draft budgets for 2026 submitted to the European Commission imply a net fiscal loosening across five major eurozone economies of around 0.5% of GDP, mostly driven by the substantial expansion in Germany. This marks a significant shift in policy setting, where fiscal policy will flip from being a drag of 0.25% of GDP in 2025 to a boost. It marks the first net loosening since 2021.[7]

Investment implications

Given the foundations of change taking place in Europe, how could investors position themselves to capture compelling opportunities?

Despite a strong year for European equities in 2025, there are long-term trends that continue to play out. It is important to note that while the European equity universe is smaller than that of the US, it is more diversified. As a result, there is a wide range of sectors and companies likely to benefit from a pick-up in GDP. Adopting a core approach while retaining the ability to invest across a broad investment universe could help increase exposure to both cyclical and growth opportunities.

As such, the key themes for investors to monitor across Europe include:

- Utilities and grid capex

Electrification of the grid and an industrial recovery are expected to drive an increase in electricity demand in Europe by 1.5% to 2% annually through to 2030.[8] Grid investments, projected at €14bn annually in Germany by the late 2020s,[9] will help underpin regulated asset base expansion. Utilities that offer strong visibility on earnings growth and dividend yields appear particularly attractive.

- Construction and infrastructure

Germany’s infrastructure fund is a game-changer for contractors, cement producers and original equipment manufacturers (OEMs) in the energy value chain. Rail modernisation (€107bn earmarked)4 and housing renovation programs will help create sustained demand for construction services and materials.

- Financials

The sector offers a combination of strong fundamentals, improving profitability and compelling valuations. Banks’ earning momentum is supported by strong financial positions and still-elevated lending margins. Valuations look attractive versus US peers, particularly in periphery markets like Spain, Italy, and Greece.

- Defence and security

Defence spending is set to surge in response to ongoing security threats. However, the push for security extends beyond military defence to reliable energy sources, stable infrastructure and secure supply chains. Cyber security is also a growth area as AI has enabled more efficient and effective cyber-attacks.

- Green technologies and heavy industry

Rising carbon prices and policy incentives favour companies investing in carbon capture, hydrogen, and energy efficiency. These technologies will be critical for meeting decarbonisation targets while maintaining industrial competitiveness.

Europe’s structural reforms and fiscal stimulus represent a decisive shift toward resilience and competitiveness. While geopolitical risks and execution challenges persist, the policy mix of EU-wide initiatives and national programs, anchored by Germany’s fiscal pivot, create a robust foundation for growth.

For investors and financial advisers, the implications are clear: sectors aligned with infrastructure, energy transition, defence, and industrial modernisation offer attractive opportunities over the medium to long term.

[1] Source: Bloomberg NEF, September 2025

[2] Source: Council of the European Union, July 2025

[3] Source: Deepnewz, March 2025, Die Bundesregierung, October 2025

[4] Sources: European Commission, Bundesfinanzminsterium, GMK Center, Capital Group

[5] Source: Bundesministerium de Finanzen, June 2025

[6] Source: Tradingeconomics.com, November 2025, Eurostat

[7] Source: Capital Group, November 2025

[8] Source: IEA, Electricity Report 2025

[9] Sources: Berenberg, Capital Group, October 2025

Matt Reynolds is an Investment Director for Capital Group Australia, a sponsor of Firstlinks. This article contains general information only and does not consider the circumstances of any investor. Please seek financial advice before acting on any investment as market circumstances can change.

For more articles and papers from Capital Group, click here.