Phil Ruthven’s contribution as one of the nation’s foremost business commentators and forecasters has been acknowledged in this and many other publications. I worked with Phil in the 1980s and 1990s and it was the research techniques and models for business and strategic analysis he pioneered that led me to change careers and move into investment management.

In the interest of investor education and for the long-term investors out there with a Buffett-style investment philosophy, here are a few things Phil taught me that helped make me a better long-term investor.

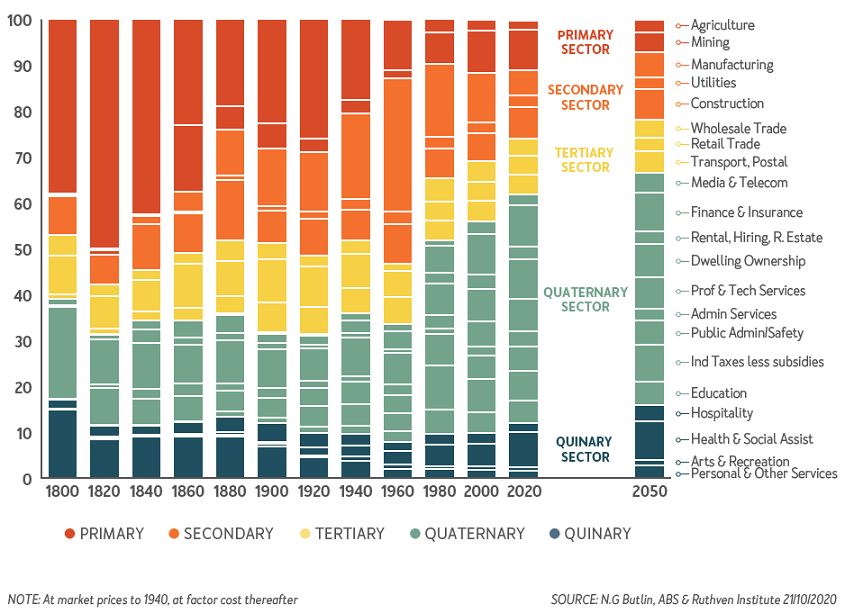

Lesson 1. Follow the money

One of Phil’s more famous charts illustrates the changing structure of the economy over the past two centuries as we moved from the agricultural age when our primary industries dominated wealth creation through to the industrial age where secondary industries and particularly manufacturing were the major wealth creators. Now into the information or digital age, it is the quaternary (information industries) and quinary industries (service industries) that are winning share of the earnings pie.

Industry Division: Changing Importance

Australia, shares of GDP by industry division, 1800–2050

Intuitively, I use this backdrop as an input into portfolio construction where my preference is to skew the portfolio towards companies in industries that are increasing their share of the earnings pie. This is not to say there are not some wonderful Australian and international companies in mature industries that continue to grow and deliver excellent returns by winning market share. There are. But at the portfolio level, my tilt is toward companies well positioned (see lesson 4) in this change.

Lesson 2. Understand a company’s competitive operating environment

Critical to long-term stock outperformance is understanding the industry in which a company operates and its competitive operating environment. We cannot begin to think about the potential size of the opportunity set and threats facing any company without this. To quote the great business strategist, Peter Drucker, the first question to answer is: what business are you in?

This is not as easy as it sounds, and it is made harder by the GICS classification system which often classifies companies according to the markets they serve rather than what business they are in. This often leads to muddled thinking and flawed analysis.

How often have we read that we should invest in internet companies with the usual list of names such as Uber, Amazon, and Netflix. There is no internet industry as such. Uber is in the taxi and ride-sharing industry, Amazon is in the department store industry and Netflix is in the broadcasting industry.

All these companies represent new disruptive technologies in these industries. The IBIS industry database is based on the official Standard Industrial Classification system (SIC) used by statistical agencies the world over to define industries and with a few exceptions is a good place to start when defining and analysing a company’s competitive operating environment. It is also where you can get official statistics on the size of the industry when quantifying the size of the opportunity set and the positioning and market share of industry participants.

Lesson 3. Know the development phase of the industry in which the company operates

Michael Porter, another famous business strategist, stressed the importance of knowing the development phase (i.e. pioneering, growth, maturity, decline) of the industry in which a company resides. While some long-term investors acknowledge its importance when assessing the short, medium, and long-term outlook for earnings, few to my knowledge have come up with a methodology to determine it. Phil did, using the industry’s value added as a share of the value added of the total economy, (i.e. our Gross Domestic Product) and tracking it over time.

Again, I find this a powerful valuation tool when thinking about the longevity and future growth of the earnings stream of any company. The average industry cycle is around 35-40 years with each new cycle characterised by a new disruptive/transformational technology or system. This is the average, but some are much longer, and some much shorter. Think of the motor vehicle manufacturing industry where the basic technology and systems has changed little since the first model-T Ford rolled off the production line over 100 years ago. The motor vehicle industry peaked as share of the economy and business earnings in the late 1960s and after declining relative to the total market for 50 years is now clearly back into a new cycle pioneered by electric vehicles and the likes of Tesla. Compare this to the television broadcasting industry where the cycle length is much shorter with new cycles around colour TV, pay TV and now streaming all in living memory.

Lesson 4. Understand a company’s position within its industry

Years of research by Phil confirmed that there are only two sustainable positions within an industry that can deliver long-term outperformance.

A company must be either a major player with significant cost and scale advantages or a niche player usually focusing on one product group within an industry. Caught-in-the-middle players rarely outperform or survive over the long term. My observation over many years is niche players often have stronger and more sustainable competitive advantages than the industry majors and therefore can be one of the best hunting grounds for companies delivering superior long-term outperformance. This is particularly true where one or two players dominate a niche globally. Australia is blessed with some outstanding niche players across a range of industries. Examples include pharmaceutical manufacturing (CSL in blood products), medical device manufacturing (Cochlear and ResMed) and internet publishing and broadcasting (Carsales, REA, and Seek).

Lesson 5. Learn from history

Applicable in life and investing, Phil was renowned for his long-term charts and time series on the macro business environments and individual industries. Tracking the economy from the macro to the micro often enabled Phil to see linkages and trends well before anyone else. This alone is a very valuable investing tool, but for me even more valuable is using history as an input into weighting risk when valuing a company. It is the risks you can’t measure that can often hurt you the most.

Studying the history of any industry, the key drivers of every cycle and the changing composition and market share of participants is always valuable in weighting risk at both the industry and company level.

Thank you, Phil.

Jennifer Mead worked with Phil Ruthven in the 1980s and 1990s before changing careers and moving into investment management.

Firstlinks’ archive of Phil Ruthven’s contributions can be viewed here.