One of the sillier pieces of nonsense bandied about in recent years by so-called experts has been the ‘new new normal’ in the ‘low return world’. This wonderful idea was coined by Bill Gross and Mohamed El-Erian, then joint Chief Executives of PIMCO (the largest bond fund manager in the world) in 2011 to spruik their bond fund.

They toured the world in mid-2011 skiting about their decision to sell US Treasuries early that year. It was lousy timing as Treasuries promptly rallied strongly in the European bank crisis and US credit downgrade crisis in mid-late 2011. PIMCO realised their mistake and bought back into Treasuries in 2012 right before bond yields rose during 2012 and 2013. Both were bad calls and Gross and El-Erian were fired (I met El-Erian in May 2011 and questioned him about the ill-timed decision).

But somehow the catchphrases ‘new new normal’ in a ‘low return world’ were picked up and repeated ad nauseam in headlines and articles by lazy reporters.

The best run of positive returns ever

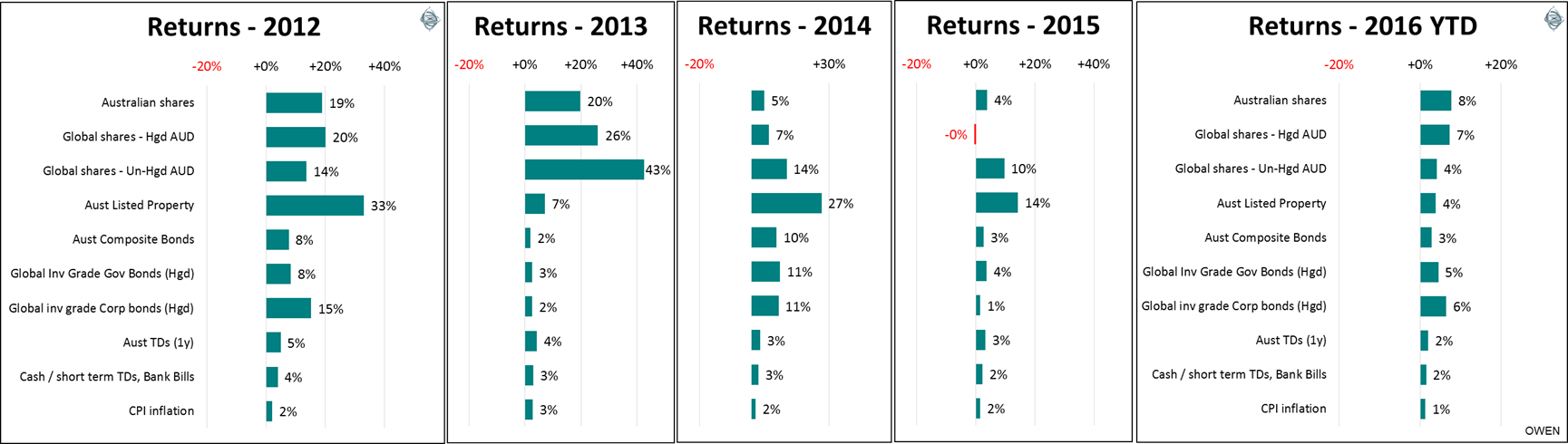

So what has happened in the five years of supposedly low returns since the start of the ‘new new normal, low return world’? Actually, five years of good returns from every asset class!

Click to enlarge

What is remarkable is that there are no red bars (indicating negative returns) in the above charts. None of the major asset classes suffered negative returns in any of the past five years. This has never happened before for Australian investors, ever.

Never in the history of Australian markets have investors received positive real (after inflation) returns from Australian and global shares and bonds, local cash and commercial property in five consecutive years. (For commercial property returns I used listed property trust returns since 1974).

The best run in the past was for four years from 1925 to 1928. Apart from that, the best investors have done has been two consecutive years of positive real returns from all of the main asset classes: 1944-45, 1997-98, and 2004-05.

Some readers might retort with something like, “Ah yes, but that was just because of quantitative easing and negative interest rates.”

Well, not really. In the US, which is still the world’s largest market and the one that drives markets in the rest of the world, the Fed scaled back QE during 2014, started reducing the Fed balance sheet in 2015 and 2016 as bonds matured, and then started raising interest rates in December 2015. So the early monetary expansion turned into monetary tightening. In Europe and Japan, the central bankers are backing away from QE and negative rates. On the fiscal front, expansion turned into tightening; the four years of trillion-dollar deficits in the US from 2009-12 has been followed by fiscal tightening from 2013-16. But still the stock markets, bond markets and property markets powered on.

On top of all that, we’ve had a steady stream of ‘sell everything’ panics along the way that have provided sensible long-term investors with great buying opportunities, such as:

- the Greek defaults

- a couple of bond yield spikes

- a ‘flash crash’ or two

- the Cyprus banking collapse

- the US ‘fiscal cliff’ crisis

- the shut-down of the US Federal government because it couldn’t pay its bills

- the violent unwinding of the Arab Spring uprisings across the Middle East

- the rise of ISIS

- the fracturing of political structures into radical right and left wing parties across the world

- the collapse of commodities prices causing a string of bankruptcies in oil, gas and steel industries

- the slowing of China

- stagnant or weak economic growth in Europe, Japan and just about everywhere else in the world

- a currency war between all of the main central banks in the world

- a series of escalating military tensions in the disputed waters off China

- another Chinese stock market bubble and bust

- the rise of nuclear threats in Iran and North Korea

- deep recessions in Russia and Brazil

- a plethora of pathetic Prime Ministers in Canberra, plus

- a good measure of Brexits and Trumps to boot!

And every asset class did well through it all.

If this is the ‘new new normal in a low return world’, then I want more of it!

It is another reminder for investors to ignore the chatter of fund spruikers, so-called ‘experts’ and the financial media in particular and focus on the facts. Bring on 2017.

Ashley Owen is Chief Investment Officer at independent advisory firm Stanford Brown and The Lunar Group. He is also a Director of Third Link Investment Managers, a fund that supports Australian charities. This article is general information that does not consider the circumstances of any individual.