Past performance is not a reliable indicator of future performance. Unless it relates to superannuation funds it seems. The release of the Your Future, Your Super (YFYS) performance test results shines a bright light on underperformance.

MySuper funds, which account for $900 billion in assets, around a third of all superannuation savings, are the default options for employees who don’t select their own fund. Greater transparency and increased member engagement will benefit both members and the industry. The long-term returns these funds achieve will determine how comfortable members will be in retirement.

Funds which are persistently underperforming, particularly those that charge high fees, have no place in a compulsory industry. Frontier supports increased scrutiny for the benefit of improving all member outcomes.

However, predicting future performance from past performance is difficult, even for professionals. ASIC reviewed over 100 academic papers from the last 40 years and concluded:

“Good past performance seems to be, at best, a weak and unreliable predictor of future good performance over the medium to long term.”

In addition, ASIC concluded performance comparisons can be quite misleading if not done properly. Importantly, returns are only meaningful if adjusted for risk/volatility or comparing "like with like".

Member outcomes

Maximising net returns (after fees and taxes) over the long term is the most important way in which the superannuation system contributes to adequate and sustainable retirement incomes.

Understanding the risks associated with investment is important for assessing the relative investment performance of funds and products, both retrospectively and into the future.

However, the YFYS annual performance test neither measures the return members achieve, nor adequately measures the risks a fund took in achieving the returns. The performance test compares each fund’s returns over the last seven years with its strategic asset allocation.

The performance test only assesses a small part of member outcomes:

- The test assesses how well a fund has implemented its chosen strategy, not whether it is a good strategy.

- It ignores actual returns and the CPI+ objectives of funds that reflect long term member outcomes.

- It does not incorporate most risk adjusted improvements from more diversified exposures.

- It is not a peer relative assessment of underperformance (unlike the YourSuper comparison website and some heatmap measures).

The test also assumes a common approach to establishing portfolios - namely a traditional approach of setting a strategic asset allocation and implementation around a goal to outperform the strategy. In practice portfolios are built in a variety of ways. In the current challenging market environment, a total portfolio approach that considers these two elements together may well provide better outcomes to members over the long term. Unfortunately, such an approach could see a fund fail the YFYS performance test and so may now be less likely to be adopted by funds.

A fund with an investment strategy which will deliver poor long-term member outcomes, but is well implemented, will be judged better than a fund with a good long-term investment strategy but its implementation has been poor in the short term.

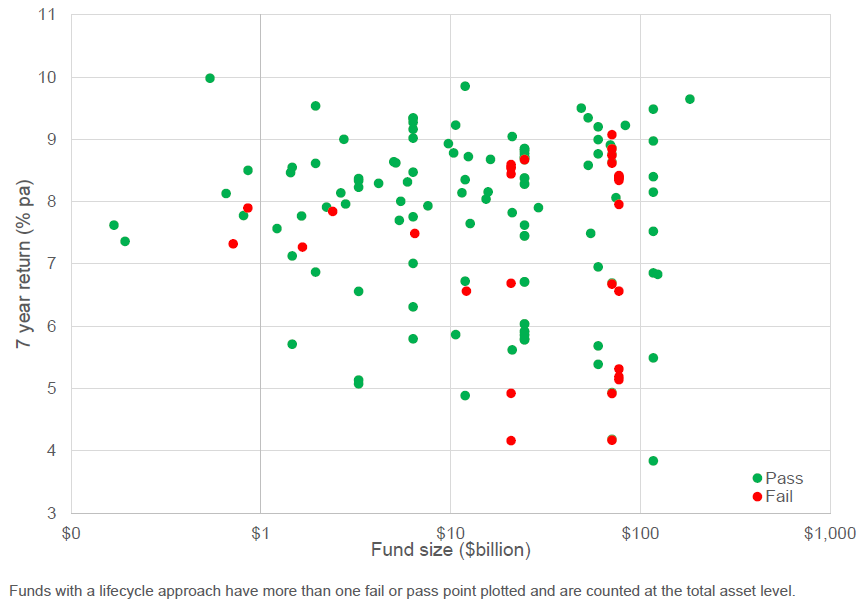

The chart below compares the actual performance for each fund with its performance test result. The chart also shows the asset size of each fund.

The chart highlights it is not just poor performing funds which have failed the test. In part, this reflects lifecycle funds, where the overall fund can fail the test despite some of the underlying options producing good returns.

Observing that some funds which have returned highly for their members have failed the test, while other lower returning funds have passed the test is intuitively hard to reconcile and could lead to consumer confusion and disengagement – the opposite of the desired outcome.

In addition, while a number of small funds failed the test, size isn’t a key indicator of the test result. Large funds also failed, showing increased scale isn’t the panacea to good member outcomes.

Indeed, the distribution of ‘failed funds’ appears to be quite random when viewed by return and size – two factors many would assume to be indicators of success.

Persistent performers

The Government and the regulator continue to reference addressing ‘persistent underperformance’. This reflects that superannuation is a long-term investment and that even good funds will suffer from periods of underperformance.

The performance test measures funds returns over seven years (eight next year), reflecting the period since the introduction of MySuper. However, the test doesn’t differentiate between funds which have had one or two years of poor recent performance from those funds which have persistently underperformed in each, or even most, of those years.

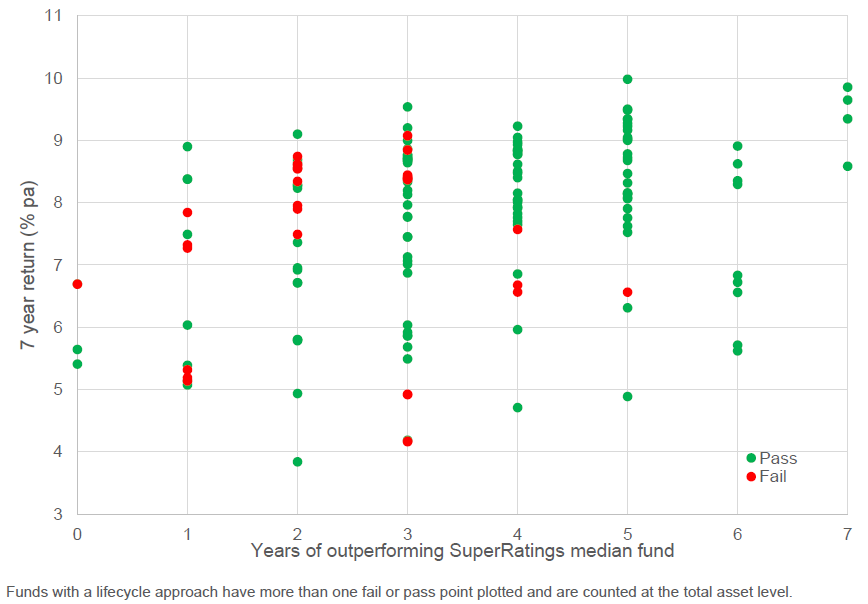

The chart below examines the number of years each fund has outperformed the relevant Super Ratings median fund in each of the last seven years.

Funds which have outperformed the median fund in only one or two years in the past seven, and so underperformed in the rest, could be considered ‘persistent’ underperformers. However, the majority of these funds have not failed the performance test. Indeed, there are some funds which have never outperformed the median in any single year but have still passed the performance test.

The test does not allow much leeway for funds who have made improvements to their approach and performance in recent years and therefore are on a good trajectory to become a higher performing fund in the near future. Such a transition would generally take longer than the one year allowed post the initial test failure notification.

Adjusting for risk

When comparing funds on performance, it is important to make sure you are comparing ‘like with like’. Super funds offer a range of different super products. These products have different levels of risk and thus different levels of expected reward.

A high-growth product would be expected to return more over the long run but might experience higher highs and lower lows in the short term than a balanced product. In turn, a balanced product would be expected to return more in the long term, but with increased volatility in the short term than a conservative or cash-based product.

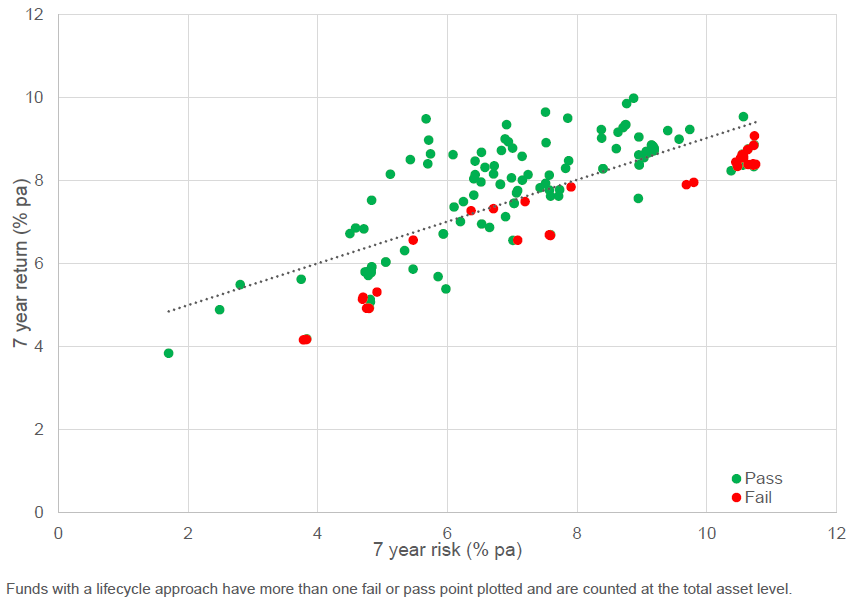

The chart below plots the performance of each MySuper fund over the last seven years against the level of risk (measured by the volatility of return). As expected, funds which have a higher return have typically also had higher risk.

Several funds that have failed the test are very close to the trend line of the overall population. This highlights the binary nature of a pass or fail and means there are several funds passing ‘close to the line’, while others have missed out by very thin margins.

Additionally, a number of funds with higher risk strategies have failed the seven-year test. Many of these represent very long term ‘lifecycle fund’ stages developed purposefully for their youngest members.

Engaged members

Great member engagement is beneficial to the superannuation system if it leads to better decision making. However, attempts at better engagement which only lead to member confusion or poor decision making should be avoided.

Funds who ‘fail the test’ will be required to send their members a letter informing them of this result and setting out, in standard terms, a range of information for members to consider. What should a member do if they receive a ‘fail’ notification from their fund?

- Visit the YourSuper comparison tool and compare your fund’s performance and fees with other funds. Be more concerned if your fund has poor performance compared to other similar funds.

- Use the ‘compare’ functionality of the comparison tool to investigate the performance of your fund over three and five years as well.

- Do your homework on your fund’s performance – check out the fund’s website, read the annual report and attend the annual member meeting.

- Understand the other services offered by your fund, especially the insurance coverage. Switching funds can have a significant impact on your insurance benefits.

- If you are thinking of switching to another fund with better performance, make sure you understand its risk level. If it’s a higher risk fund, are you comfortable with the possibility of more volatile returns?

David Carruthers is a Principal Consultant and Head of Member Solutions at Frontier Advisors. A full copy of this report can be accessed here. This article is general information and does not consider the circumstances of any investor. Investors should seek individual advice prior to taking any action on any issues raised in this article.