In this era of heightened geopolitical and macroeconomic uncertainty, portfolio construction increasingly favours assets capable of delivering durable income, capital preservation, and differentiated return drivers. Unlisted Australian commercial property continues to demonstrate qualities that may support these characteristics.

The immediate backdrop is hard to ignore. On 12 March 2026, the International Energy Agency said the war in the Middle East was creating the largest supply disruption in the history of the global oil market1. At the same time, the IMF has warned that financial stability risks have increased as trade and policy uncertainty remain elevated.

A fractured landscape demands decision-makers weigh risk and resilience more heavily than a decade ago. This note highlights some of the reasons why an allocation to unlisted Australian commercial property is important in today’s uncertain environment, offering attractive returns underpinned primarily by space market fundamentals rather than daily swings in sentiment.

1. Exposure to a scarce, real asset base

Unlike financial securities, commercial property is anchored to land, planning rights and physical improvements. Like residential property, land comprises a sizable proportion of total asset value, typically 30-60% depending on the commercial property sub-sector2. While exposure to land does not eliminate downside, it does mean value is supported by a real, location-specific asset that cannot be readily replicated.

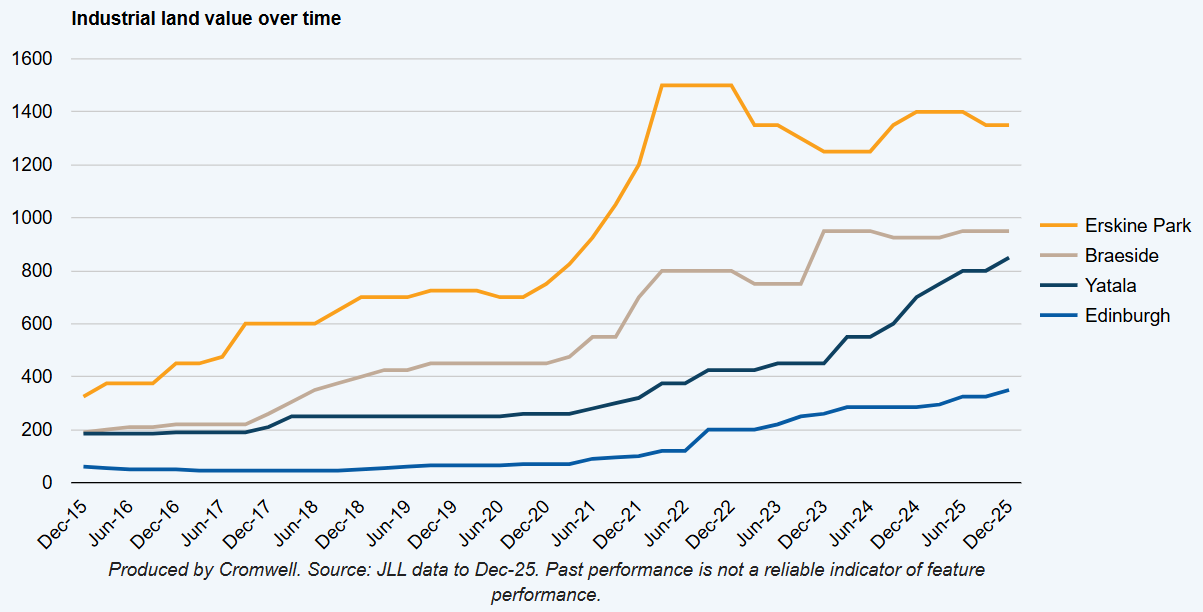

The practical importance of that scarcity is clearest in well-located urban markets. For example, just 4% of Sydney’s serviced industrial-zoned land remains undeveloped3, and Brisbane is expected to run out of developable industrial land in less than five years4. Such shortages limit potential supply, driving land value appreciation and underpinning long-term rent growth.

2. Inflation protection

The income profile of commercial property further strengthens its position in uncertain environments. Australian commercial lease structures typically incorporate annual rent increases, often linked to CPI (e.g. CPI + X%). This helps defend investors from income erosion in real terms, which is particularly important when price pressures are proving persistent.

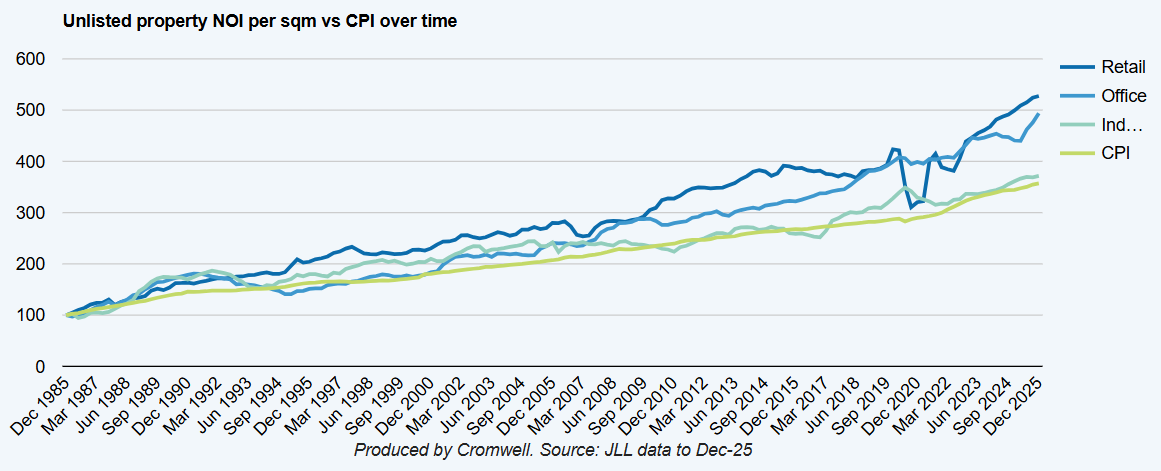

Inflation also influences the supply side of the equation. Construction costs have increased by approximately 30-45% across Australia’s major capital cities over the last five years, with further escalation of 20-30% expected through to 20295. This has contributed to higher replacement costs and rendered most new developments commercially unfeasible, constraining the delivery of new supply. CBRE estimates office economic rents have increased by 30-60% across the major CBD markets since 2020, far exceeding market rent growth, with further increases expected through to 20306. For owners of well-located existing assets, this dynamic supports income growth as competing supply is unlikely to be delivered until market rents (and/or valuations) significantly appreciate.

3. Lower volatility

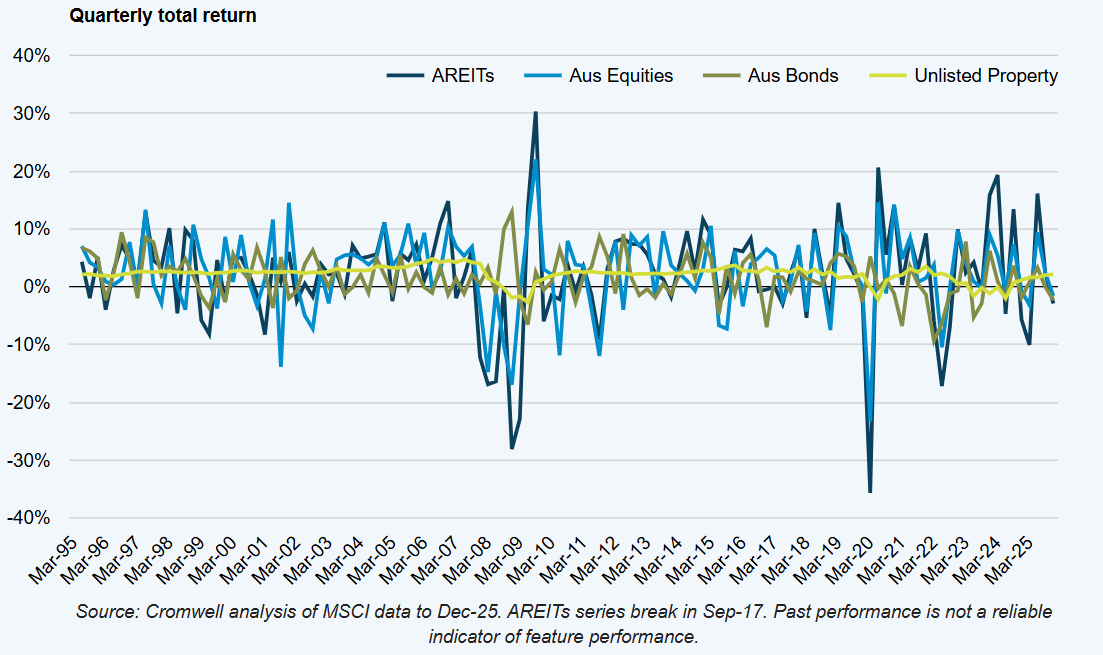

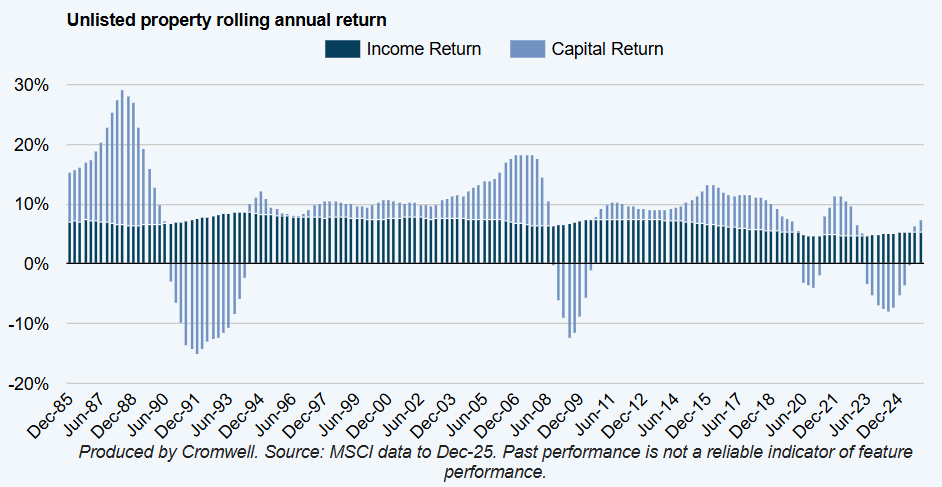

Income durability is complemented by a return profile that is less exposed to short-term market volatility. Commercial property income is typically contracted over medium to long durations, providing visibility over cashflows. Valuations in unlisted markets are appraisal-based and reflect leasing outcomes and capital market evidence, rather than intraday repricing. This approach can dampen short-term volatility and focus outcomes on underlying asset fundamentals across an appropriate investment horizon, rather than constant sentiment swings. This distinction becomes more pronounced in periods where listed markets are reacting rapidly to geopolitical or macroeconomic developments.

4. Performance driven by space market fundamentals

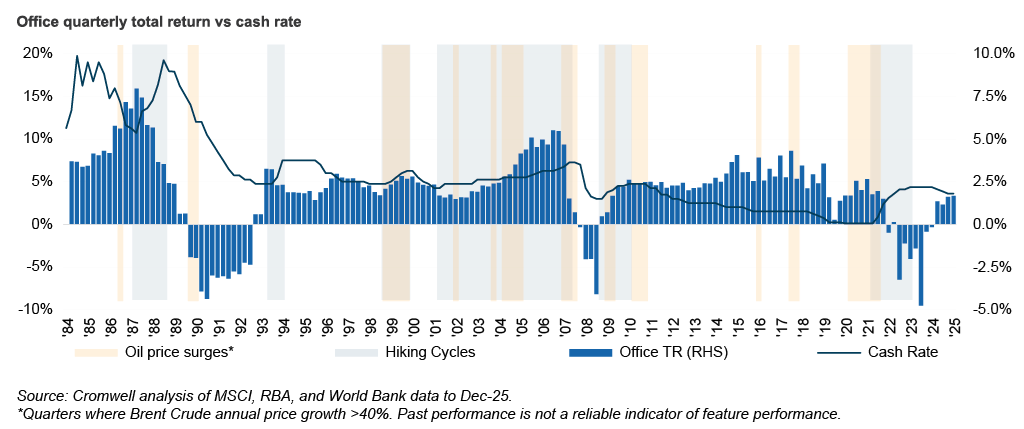

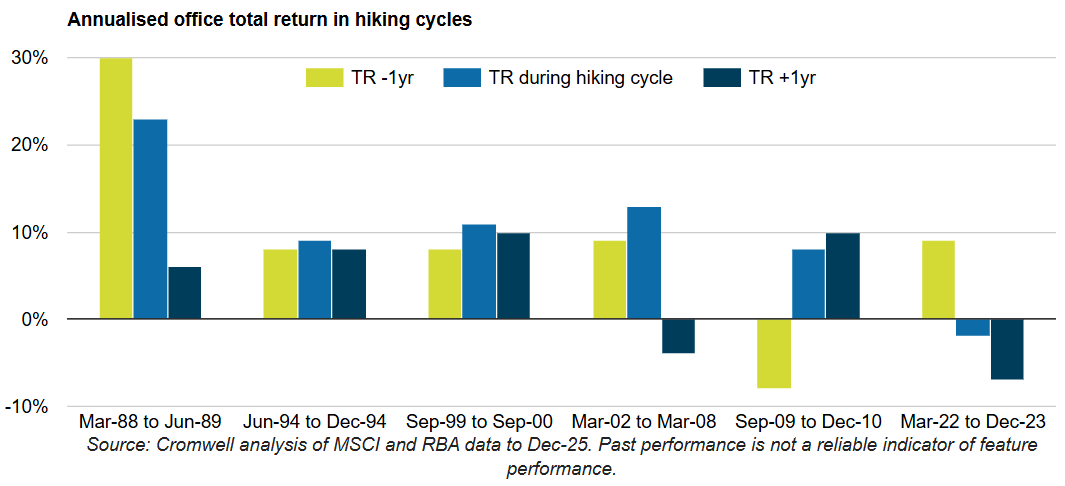

Interest rates are an important consideration, influencing discount rates, debt costs, and transaction liquidity. However, unlisted property performance is usually more dependent on space market fundamentals – demand and supply levers and the resultant vacancy conditions. Using CBD office as an example, analysis over the last 40 years indicates a strong negative correlation (-0.7) between vacancy rate and total return. Further, analysis of past cycles shows returns tend to outperform during rate hikes compared to the year prior. Similarly, unlisted commercial property has not been consistently impacted by oil price shocks historically.

The key underwriting question, therefore, is not the trajectory of the cash rate or the price of oil, but where vacancy is heading and which assets still retain pricing power with tenants. Positively for commercial property, economic expansion and jobs growth remain solid, supporting space demand. At the same time, a dearth of supply, exacerbated by higher-for-longer inflation and rising interest rates, bodes well for a tightening in vacancy and stronger income growth across quality assets.

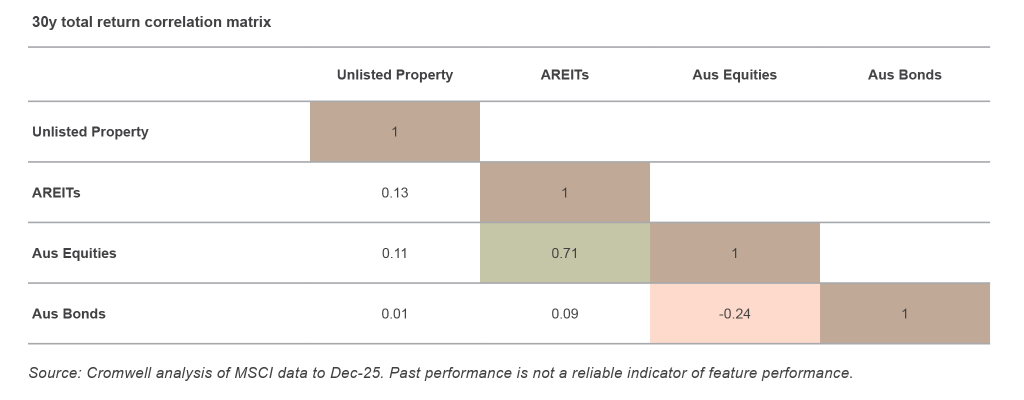

5. Genuine diversification

Unlisted commercial property has different return drivers compared to other asset classes such as equities and bonds – lease structures, tenant covenants, asset quality and local market conditions, rather than interest rates, earnings cycles and risk premia. This differentiation results in largely uncorrelated returns, providing diversification and resilience within a broader portfolio, particularly in periods where equities and other liquid assets are more directly influenced by macroeconomic or geopolitical developments. The relatively stable income component of total return further enhances its role within a diversified allocation.

Where to be selective now

Office (quality bias):

Focus on well-located, efficient and sustainability aligned assets with strong transport connectivity and credible NABERS and Green Star pathways. The office sector has experienced the sharpest repricing in the recent cycle, and there is emerging evidence of improved leasing conditions in higher quality assets, where active leasing and capital expenditure execution are key differentiators.

Neighbourhood & convenience retail:

Neighbourhood and convenience-based centres continue to benefit from their nondiscretionary tenant mix and long-dated leases, which can support more predictable rental income. Transaction activity in this segment has remained resilient as investors prioritise income visibility and covenant quality.

Industrial & logistics:

While returns have moderated from the exceptional conditions seen in recent years, occupier demand remains focused on well-located, infill assets. Space availability and future supply are both constrained within this segment of the market, supporting positive rent reversion upon lease expiry. Ageing stock and rising obsolescence present an additional opportunity set for active managers with value-add capability.

Conclusion

Over the long-term, Australian unlisted commercial property has demonstrated resilient returns through periods of conflict and oil shocks, with performance supported by income and leasing fundamentals. Unlisted commercial property offers a compelling combination of income stability, inflation linkage, and real-asset backing. When combined with underwriting discipline, discerning asset selection, and active management, these characteristics reinforce its role as a core allocation within diversified portfolios, particularly in periods of heightened volatility.

Footnotes:

1International Energy Agency Oil Market Report (March 2026)

2Cromwell analysis of Victoria Valuer-General 2025 statistics

3Sydney Industrial and Logistics Land Supply, CBRE (Feb-25)

4No room to grow – Industrial Land Supply & Vacancy Report, Property Council of Australia & SA1 Property (Sep-25)

5TPI % Change Calculator and Q1 2026 Construction Market Update, RLB (Mar-26)

6CBRE (Feb-26)

Cromwell Funds Management is a sponsor of Firstlinks. This article is not intended to provide investment or financial advice or to act as any sort of offer or disclosure document. It has been prepared without taking into account any investor’s objectives, financial situation or needs. Any potential investor should make their own independent enquiries, and talk to their professional advisers, before making investment decisions.

For more articles and papers from Cromwell, please click here.