The branding of financial planners is causing confusion among consumers, according to a recent report released by Roy Morgan Research.

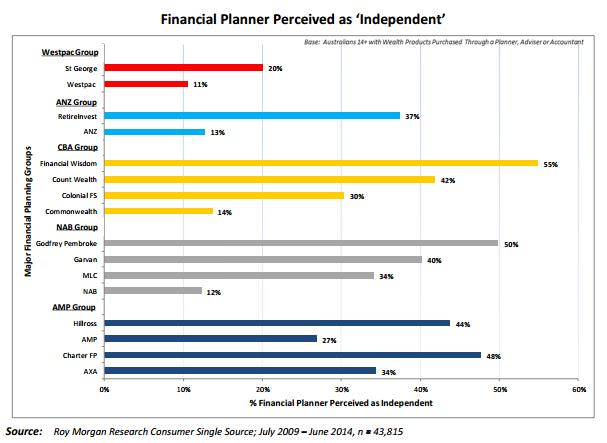

The depth of consumers’ confusion is highlighted by the sobering statistic that 14% of consumers visiting a Commonwealth Bank branded financial planner believe they are getting independent advice. Consumers’ confusion increases when they visit a financial planner operating under a different brand compared to that of the umbrella financial institution; 55% of consumers visiting the Commonwealth Bank owned Financial Wisdom perceived it to be independent.

However the problem of independence is not just one of flawed consumer perceptions. Customers of both independent and vertically integrated financial planners have suffered avoidable financial losses after taking poor conflicted advice.

Sean Graham, Principal of Assured Support and previously Head of Advice and Advocacy at Millennium3, said, “The tendency of vertical integration means that advisors have a list of 100 products or more on their approved product list, but when you drill down they maybe only really recommending eight aligned products.”

But there are many examples of business models where conflicts of interest are successfully managed, including newspapers and auditors. And as part of the financial advice giving process, consumers are given a financial services guide which explains where the advisor and the licensee sit as part of the group.

So should consumers be mollycoddled?

In reality, the marketing material in financial planning practices, which the consumer is far more likely to actually read, seldom highlights any ownership relationship or the implications of that relationship. And the ownership relationship can create a fundamental conflict of interest regardless of what remuneration practices are adopted.

Mr Graham said, “Even if you strip out conflicted remuneration by financial institution-owned financial planners, they are still going to be more likely to recommend their own products, because they want to keep their job. If you went into a Toyota showroom, what is the chance they are going to recommend a Ford?”

Les Goldmann has over 20 years experience as a Chartered Accountant. His other roles have included journalism, working as the policy and research manager for the Australian Shareholders Association and senior positions in the commercial and non profit sectors.