In 2014, I examined sequencing risk in late accumulation with a thought experiment involving two fictional 55-year-olds, William and Edward. Both started with the same superannuation balance, earned identical salaries, and achieved the same annualised return of 7.1% per annum over ten years; yet Edward's final balance at retirement exceeded William's by some 14%.

The difference stemmed from the order in which they received those returns. Returns as experienced by individuals are cashflow sensitive and path dependent: both the timing of cash flows and the sequence of returns determine the final dollar outcome from which a retirement is funded.

The current financial market volatility, triggered by unrest in the Middle East, presents an opportunity to revisit sequencing risk, this time from the perspective of a recent retiree. Let’s now rejoin William and Edward at the start of their retirement years.

Bill and Ted's unwelcome start to retirement

William and Edward's 2014 retirement plans did not unfold as hoped. The COVID pandemic of 2020-22 caused both a short-term loss of employment and relationship breakdown for each. Both delayed retirement until age 67 to qualify for the Age Pension as single homeowners. They now arrive at retirement with $500,000 in superannuation, each moving into an account-based pension (ABP) invested in a balanced option with a large APRA-regulated super fund, with units acquired on 31 December 2025.

Both have elected to draw $30,000 in their first year, $2,500 per month, aware that the median ABP balanced option has returned around 8% per annum over the past decade. Combined with an estimated $685 per fortnight in part-Age Pension, this should provide just under $50,000 for 2026, meeting their spending needs. Neither has any other financial assets or income.

To illustrate the sequencing risk effect, actual daily unit prices from a balanced ABP are used for the first quarter of 2026, with only one variable changed: the timing of monthly pension payments. William receives his payment on the day with the highest unit price each month, Edward on the day with the lowest, thus isolating the pure sequencing risk effect.

Time-weighted versus money-weighted returns

William and Edward each hold an identical number of units in the same balanced ABP on 1 January[1]. A new unit price is struck each trading day reflecting the option's net asset value (NAV) as market movements occur.

Every pension drawing results in the sale of units at that day's price. When unit prices rise before the next pension payment, fewer units need be sold. When they fall, more units must be sold to fund the same dollar payment.

A sequence of poor returns hurts ABP holders because higher portfolio volatility (itself a function of asset allocation) increases the likelihood of negative returns. For a given pension payment, negative returns accelerate unit depletion, which, if sustained, can hasten account exhaustion ahead of the retiree's desired or projected timeframe.

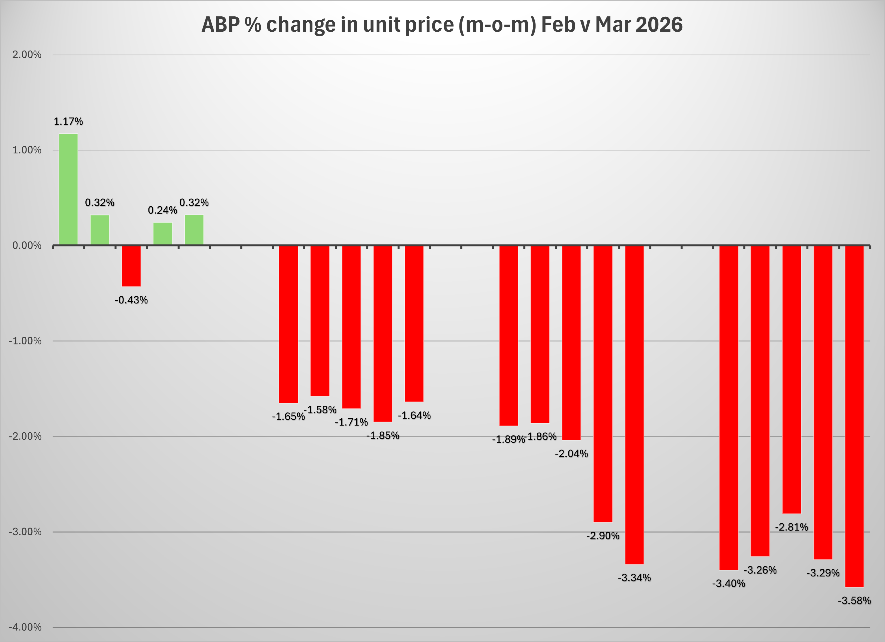

A review of daily unit prices experienced by William and Edward below illustrates the point. The following chart shows the percentage change in unit prices between each trading day in February and the corresponding March day for this balanced option.

Source: author’s calculations (based on daily unit prices for February and March)

The chart shows that anywhere from 1.2% fewer to 3.6% more units would have needed to be sold in March to fund the same dollar pension payment relative to February (depending on the day of transaction), creating sequencing risk.

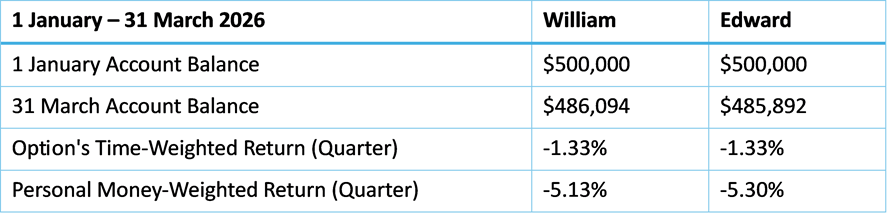

The table below summarises the quarterly outcomes for both retirees.

Source: author's calculations (except for the option’s time-weighted return)

Two differences stand out. First, despite identical starting balances and identical monthly withdrawals, Edward ends the quarter with a slightly lower balance than William purely due to the sequencing risk effect of lower unit prices on his pension payment days. Second, the fund's reported time-weighted return of -1.33% differs markedly from each retiree's personal money-weighted return, a gap of around 4 percentage points.

This distinction matters. Time-weighted returns neutralise cashflow impacts and are adopted as the global standard for fund managers to report performance, because fund managers are not in control of when investors contribute or redeem.

For the individual retiree however, money-weighted returns (IRR) capture both the timing and size of cash flows, making them a far more meaningful measure for personal retirement planning and ongoing management thereafter.

Managing sequencing risk in retirement

Of all the strategies available to mitigate sequencing risk, switching a diversified option to cash is among the least likely to succeed. In a retirement that could span two or more decades, attempting to time every significant market drawdown, by moving to cash and waiting to re-enter ‘at the bottom’, is not a winning approach. Future returns are simply too resistant to short-term forecasting by individual investors.

Diversification, by contrast, provides genuine benefits. Sequencing risk is a direct function of portfolio volatility, so reducing that volatility through broad diversification reduces the risk itself. A balanced option may have lost around 3.5% on a time-weighted basis during March but compare that to the 7.15% decline in the S&P/ASX 200. Diversification worked through the GFC and is working now.

At the fund level, super funds could provide money-weighted returns for their ABP members alongside time-weighted figures, helping retirees better understand their personal ‘hip pocket’ experience and so take earlier action to manage drawdown size and frequency if needed.

At the product level, forward-thinking funds can strengthen ABP design through improved drawdown rate guidance, smarter bucketing strategies (rebalancing triggers, frequency and directionality) and more nuanced glidepath thinking. For example, the ‘V-shaped glidepath’, de-risking into late accumulation followed by gentle re-risking into retirement, offers one possible new approach to navigating the retirement risk zone.

At the individual level, approximately two in three retirees will be eligible for part or full Age Pension at qualifying age. The Age Pension acts as a natural sequencing risk mitigant, rising as ABP balances fall through either pension payments or market dislocations.

Lifetime income products offer a further option, allowing retirees to transfer some or all investment/capital risk to a solution provider, and thus potentially suitable for those seeking to hedge both longevity and sequencing risk.

Account-based pensions will however remain the workhorse of the Australian retirement landscape, and sequencing risk will thus continue to test members in retirement, as it is doing right now.

The lesson from William and Edward's experience is not to avoid sequencing risk, which is largely unavoidable for retirees periodically drawing on a unitised diversified portfolio. It is to manage it appropriately, using the tools available at the individual, product, and fund level. Risk management, not avoidance, is the key to superior retirement outcomes.

[1] It is acknowledged that not all retirees are in unitised pension products with pension transactions at NAV, with APRA-regulated defined benefit pensions and SMSF trustees being two examples of those who may not be.

Harry Chemay is a co-founder of Lumisara, a consultancy that assists clients across wealth management, FinTech and the APRA-regulated superannuation sector, with a particular focus on the late accumulation to early decumulation phase of the retirement journey.