In the last five years, there has been an impressive array of new Listed Investment Company (LIC) issuance. The number of LICs listed on the ASX has seen a dramatic surge from 52 in June 2012 to 102 listed presently.

Here are seven tips for choosing a good LIC:

1. Compare against historical premium and discount

LICs are market-listed, closed-ended funds, which leaves the security exposed to the vagaries of supply and demand in the market. A LIC can trade away from its underlying pre-tax Net Tangible Assets (NTA), with the discount contracting (or premium expanding) when demand exceeds supply and discount expanding (or premium contracting) when supply exceeds demand.

Trading at a premium or a discount is a fundamental part of the LIC structure, and investors can benefit by understanding this premium and discount behaviour.

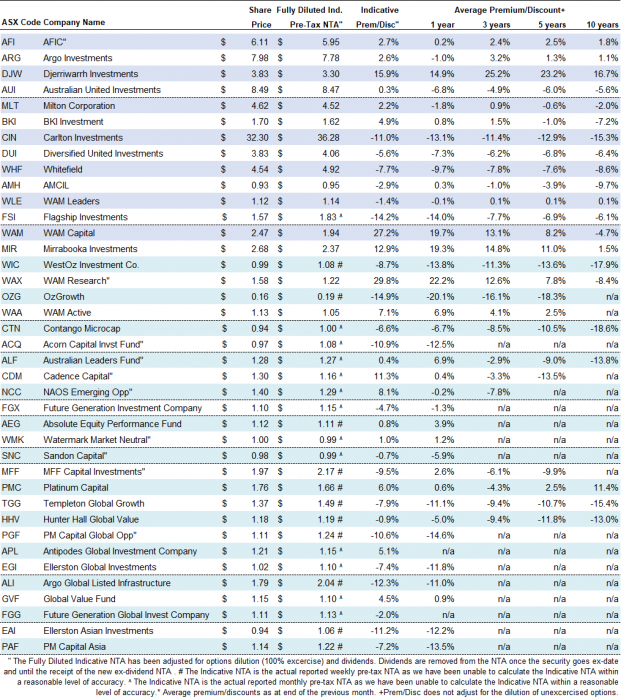

The table below shows the underlying NTA of the individual LICs in our coverage. This is calculated by modelling the percentage movements of the underlying disclosed holdings. Where holdings are not disclosed, the weekly or monthly NTA figures released on the ASX are used. This report is most effective for LICs with a high percentage penetration of investments in the Top 20, lower turnover of investments and regular disclosure of cash position. We also calculate the average premium/discount over one, three, five and 10 years.

For instance, Platinum Capital (ASX:PMC) is currently trading at a 6.0% premium to NTA (column 3), however, it has traded at an average 11.4% premium over the last 10 years (last column). This may indicate potential value, given it is trading at a lower premium than normal. However, we would argue that this premium is likely no longer sustainable noting a number of new and credible global LICs have recently entered the ASX and created viable alternatives.

Indicative premium/discount to Pre-Tax NTA (as at 01/08/17)

Source: Company data, IRESS and Bell Potter

Purchasing a LIC at a lower discount or premium to the long-term discount or premium to pre-tax NTA will not guarantee outperformance. However, if at the time of investment, the LIC looks expensive versus historical norms, perhaps an alternative LIC should be considered.

2. Familiarise with share price normalisation

There is a tendency for LICs to revert to their mean premium or discount throughout the cycle. It is important that investors understand the implications this will have on the share price.

Essentially, if an investor buys a LIC at a 20% premium to its pre-tax NTA and it ordinarily trades in line, the investor is increasing the risk of a capital loss should normalisation go towards the mean. It's similar for a LIC that trades at a narrow discount compared to its historical average of a much wider discount. Investors should be aware of the capital upside or downside when purchasing LICs, and avoid purchasing LICs simply because they are at a discount.

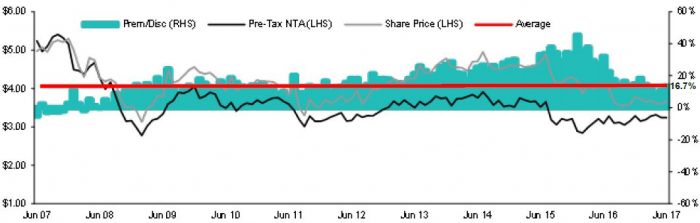

Djerriwarrah Investments (ASX:DJW) is a good case study. DJW invests in Australian equities and writes call options over individual positions, enabling an enhanced level of dividends.

DJW’s share price and NTA

Source: Company reports, IRESS and Bell Potter

Demand for DJW has historically been strong with a lack of alternatives, resulting in DJW trading at a nearly 50% premium to its pre-tax NTA in early 2016. However, in recent times, both DJW’s share price and premium have fallen. This was likely due to a dividend cut and an influx of alternative products, but the heightened premium was unrealistic. As at 1 August 2017, DJW traded at a 15.9% premium, more in line with its 10-year average premium of 16.7%.

3. Understand each LIC’s investment strategy

The LIC universe can be divided into three main categories, and the results can vary significantly between the groups:

- Domestic mandates offer exposure to the Australian market. Subsets include Large, Large to Medium, Medium to Small, and Small to Microcap companies, Long/Short/Market Neutral, Specialist and Tech.

- International mandates offering offshore exposure, with subsets such as Global and Asian.

- Specialist mandates offering other choices.

It is essential investors pick the right exposure to fit their investment portfolios. For example, an Australia equity LIC might be long only with full market exposure, or long/short with a market neutral bias, and results will differ markedly.

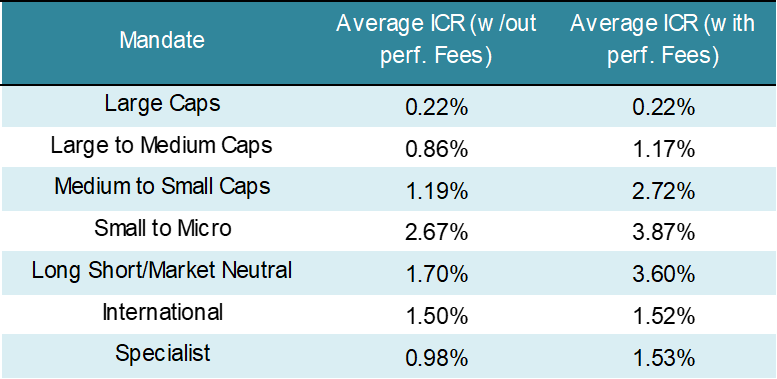

4. Watch the fees

Fees play a big part in any investment vehicle. A small difference in fees and expenses can have a substantial impact on the investor’s long-term performance given the compounding nature of returns.

Some investment mandates by their very nature are more cost intensive to execute than others. For instance, funds focused on small companies where external or broker research is limited may incur higher costs given the necessity to bridge the information gap through in-house research.

Lower fees will not guarantee superior performance, but they are clearly less of an impediment on returns. For instance, if one fund is charging a management fee of 0.2% and another charges 2.0%, it will be more difficult for the latter to deliver outperformance on a consistent basis given a requirement to recover the additional 1.8% management fee prior to delivering a positive return to the investor.

Average Indirect Cost Ratio across each LIC’s investment mandate

5. Look for medium to long-term outperformance

Historical performance is not a guarantee of future performance but it is a guide. The key consideration is whether this performance is sustainable.

The performance of a LIC can be measured using either the NTA or security price. The NTA performance seeks to measure the performance of the underlying investments of the manager. The security price performance seeks to measure the performance of the security as it trades on the ASX.

The benchmark defined by the manager is used to measure relative pre-tax NTA performance. This allows the investor to gain an understanding of whether the manager has added value through its active investment. While there may be reasons to expect improved performance in the future, a LIC that has materially underperformed its benchmark over the medium-to-long term should be approached with caution.

6. Be careful of options overhang

Most of the LICs that have listed on the ASX in recent years have come to market with a bonus option to compensate the initial investor for the issue costs reflected in the NTA. The option holder thereafter receives a right, but not an obligation, to purchase additional shares in the LIC at a fixed price (strike price) until a specified date (expiry date). The bonus option is usually listed and can be sold on the ASX, but the option overhang needs to be monitored.

Investors that seek to purchase LICs in the secondary market need to watch the potential dilutionary impact on the NTA of in-the-money options. The person who exercises the option is not diluted as they have received the benefit of the lower exercise price. In fact, if less than 100% of options are exercised (which is generally the case unless options are underwritten), they are actually accretive to those who exercise and dilutive to those who don’t.

There has been a recent evolution in the LIC industry with two LICs, VGI Partners Global Investment (ASX:VG1) and MCP Master Income Trust (ASX:MXT) coming to market without the attached option and with a proforma NAV in line with the issue price. For example, the manager will pay the issue costs for VG1 out of the fees it receives, to give shareholders access to the product at NAV at initial issue.

7. Value the dividends

A final consideration for investors is distributions. These can vary markedly from manager to manager, largely dependent on its mandate. Franking can also provide additional upside. The table below lists the top yielding LICs over the past 12 months across each investment mandate.

Highest distributions for LIC across each investment mandate

Source: Company data, IRESS & Bell Potter

Conclusion

Investing in a LIC is an investment in a listed fund manager, and the main aim should be to select a manager that has the ability to consistently beat the market and provide strong after-tax performance. However, the manager must also have the ability to manage the premium or discount. Quantitative measures can assist investors with picking the right LIC, which can be used as building blocks to complement a robust investment portfolio from a risk and return perspective.

Nathan Umapathy is Research Analyst at Bell Potter Securities. This document has been prepared without consideration of any specific client’s investment objectives and there is no responsibility to inform of any matter that subsequently may affect any of this information. For the latest Bell Potter Quarterly Report, click here, and for the Weekly NTA update, click here.