Constructing an investment portfolio should not begin with the investments. That’s where it ends. There are several steps before you reach the stage of selecting funds or direct shares, such as:

- First, define your goals

- Second, assess your risk appetite and behaviour

- Third, decide your broad asset allocation

- Fourth, examine your costs, tax and administration structures

- Fifth, choose your specific investments, which might include a fund manager.

Every investment with a fund manager should form part of an overall plan and fit into an asset allocation decision that matches your goals and risk appetite. For example, you might not invest in fixed rate bonds because you believe rates are too low or they are about to rise or credit margins will soon widen. You are not looking for a fixed rate bond manager or listed vehicle, regardless of how good they are.

Similarly, if your asset allocation requires an exposure of 10% to global equities, you then compare the products available, usually unlisted fund managers, listed investment companies (LICs), exchange-traded funds (ETFs) or direct equities. You might be seeking the greater diversification into overseas markets, or you are worried about the Australian dollar falling. You want foreign companies on foreign exchanges with foreign currency risk.

It’s your decision to suit your circumstances.

It’s not for the fund manager to change your asset allocation

So you find a global equity manager you like, and you give them 10% of your portfolio to manage. You assemble the rest into a small allocation to cash for liquidity, some into Australian equities, and you like property and infrastructure. You look with some satisfaction at the portfolio on your administrative platform or spreadsheet, knowing where you stand as markets move around. It’s a portfolio designed by you for you.

Then six months later, you attend an update from your global equity manager. He’s worried about market valuations, feels the market has run too hard and he sees it as his job to protect your capital. He has moved 50% of his portfolio to cash, waiting for better valuations.

What? So now your cash allocation is 5% higher and it might not even be in a foreign currency, and you are 5% underweight global equities. That’s not what you wanted, and you feel there’s plenty of potential in global shares.

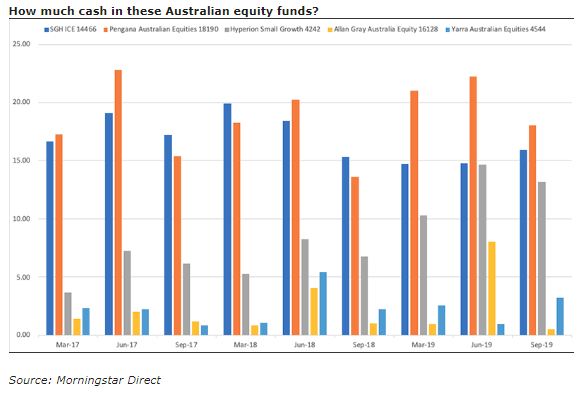

Have your Australian equity managers done the same thing? There is a wide variation in cash allocations in equity funds, as shown below for five prominent Australian funds on the Morningstar database. Several equity managers held over 30% of their fund in cash at the end of 2019.

Formal asset allocations in an SMSF

If you are investing for your SMSF, you have a defined Investment Strategy in a legal document lodged with your administrator as a prerequisite of managing an SMSF. If their portfolio software is good, it will monitor your asset allocation against your limits. If it’s really good, it might have the ability to look through the manager’s portfolio to their asset allocation.

You check your SMSF portfolio, and the red bars stare back at you. You are breaching your asset limits, overexposed to cash, underexposed to equities. You are a trustee and you may have fiduciary responsibility to other members. Fortunately, most Investment Strategies use wide ranges and it is probably not a major issue, but your asset allocation has changed without your knowledge or action.

The Australian Taxation Office (ATO) specifically instructs SMSF trustees to follow a defined Investment Strategy, such as:

"The percentage or dollar allocation of the fund’s assets invested in each class of investment should support and reflect your articulated investment approach towards achieving your retirement goals ... You should also include the reasons why investing in those assets will achieve your retirement goals."

It's worth noting that an index fund such as a global equity ETF will always be fully invested. There is no active manager decision, and that is another reason why passive management has performed well in the bull market.

In the institutional mandate world, billions of dollars are allocated by major super funds to external managers according to asset allocation decisions agonised over by Investment Committees and Investment Consultants. They are measured precisely to the first decimal place. Do the trustees realise that the $100 million global equity allocation is actually $50 million in global equities and $50 million in cash? In a separate mandate, the rules may not allow this, but many investors put millions of dollars into pooled managed funds.

Personally, when I give a global equity manager a global equity allocation, I want near to 100% permanently invested in global equities. It’s not the portfolio manager's job to protect my capital. I do that myself with my asset allocation decisions, made long before I decided they were a worthy custodian of my hard-earned.

What if the fund manager cannot find good investments?

Global active management fees vary widely, but they are far more expensive than cash management fees due to the potential for adding alpha (or outperformance) and arguably a more complex universe to navigate. A common global active fee is 1.0% to 1.5% per annum plus performance fees, but cash funds for retail investors cost about 0.4% or less.

What happens when an active equity manager runs a large cash book for a long time and charges active fees on the total asset balance? They face three choices:

- Return the money to their clients. Although such a step is common with hedge funds, where a fund manager may decide a style no longer works for the long term, the permanent loss of funds is unacceptable to most managers. There is no guarantee the money will come back in better circumstances.

- Charge a lower fee on the cash component. Some fund managers reduce their fees if the cash component sits above a defined level. For example, in the Lazard Defensive Australian Equity Fund, investment costs fall from 0.67% to 0.37% when the proportion of the Fund in cash exceeds 50%.

- Explain to investors that the cash is waiting for better opportunities while continuing to charge full fees on the entire balance. This may be a reasonable short-term position but a large cash allocation for long periods is difficult to justify. A fund manager who cannot find suitable investments over a couple of years probably needs another technique … or job.

Should an equity fund manager time the market?

It is difficult enough for fund managers to find good companies and outperform the index without also timing the market using macroeconomic tactical asset allocation. Fund managers who are active stock pickers should focus on their microeconomic, company analysis strengths.

Bank of America Merrill Lynch has developed a ‘Cash Rule Indicator’ which is a contrarian forecasting tool. It gives a buy signal for equities when cash balances held by fund managers rise above their long-term averages, and it has been a bullish indicator for almost two years. In other words, it says buy when cash is high and managers are least invested in equities.

In another example, in June 2019, The Australian Financial Review ran an article called ‘Global money managers go defensive’ which said:

“Fund managers are also holding more cash on average as they struggle to find appropriate assets to deploy excess money. "Of all the fund managers we talk to, we only know of one group that is overweight equities," Katana Asset Management Portfolio Manager Romano Sala Tenna said. "Most of them have mandates that preclude fixed income and bonds, so they're going to cash weight mandate peaks."

The market has rallied strongly since June 2019, so how well did that inability to ‘deploy excess money’ work out?

When Morningstar is rating an equity fund, it is a warning when an active fund consistently allocates large amounts to cash, as timing when to buy and sell shares is so difficult.

When is tactical cash allocation acceptable?

If a fund is specifically operating with a tactical asset allocation approach, marketed on the basis of its ability to switch between multiple asset classes based on the fund manager’s expectations, it is legitimate to hold cash. It is not sector-specific and the investor knows at the outset that the asset allocation will change. Some funds are explicitly labelled ‘tactical’. For example, the Legg Mason Martin Currie Tactical Allocation Fund is:

“*A diversified portfolio of Australian equities, fixed income and cash designed to take advantage of relative asset class mispricing

*Tilted toward the relatively undervalued asset class in anticipation that it will outperform as it returns to assessed fair value.”

Any investor in such a fund will need to either follow the changes in asset allocations for their own financial plan, or make some assumptions. It is what it is.

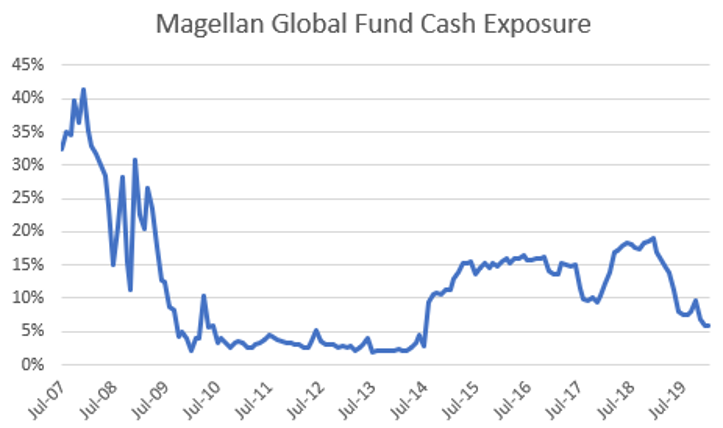

Another group of managers is explicitly focussed on capital preservation, with a benchmark-unaware style and an absolute return target. For example, Magellan's objective for its main Global Fund is 9% per annum across the investment cycle “to achieve attractive risk-adjusted returns over the medium to long term, while reducing the risk of permanent capital loss.” The Fund is allowed to hold up to 20% in cash (after the initial launch period), and it almost reached this level during the Fed tightening phase of December quarter 2018.

Source: Magellan

Know what your fund manager is doing

In summary, each investor should know how much cash is held by the funds they choose in sector-specific allocations, as the overall cash exposure in a portfolio may differ significantly from expected. When an equity fund manager has a maximum cash allocation of 5%, at least the investor knows where they stand. My preference is for an equity manager to remain fully invested and I will manage my exposure to markets through my overall asset allocation.

Please complete our one-question survey below, or use this link, on whether you are happy that your equity manager allocates large amounts to cash. Full results with comments next week, and we will post extract in the comments section.

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances of any investor.