The Weekend Edition includes a market update plus Morningstar adds links to two of its most popular stock selection articles from the week. You can check previous editions of the newsletter here and contributors are here.

Weekend market update

From AAP Netdesk: It's a good time to be in the Australian share market. The ASX has notched its 10th consecutive month of gains, equalling its record, and is tipped to deliver a buoyant August earnings season. The market gained a little over 1% in July. The most recent time investors enjoyed a run of this length was in 2006 to 2007. The US Federal Reserve this week chose not to lessen its bond buying while US GDP figures showed signs of growth slowing.

On Friday, the iron ore price moved lower and sapped the big miners. Fortescue slumped by 5.3%, Rio Tinto lost 0.5% but BHP shares had a record trade of $54.55 but closed up by only 0.3 per cent to $53.49. NAB gave investors more reason to believe bumper dividends are in store next month after it chose to buy back $2.5 billion in shares. The buyback will happen in August and follows ANZ declaring a similar move earlier this month. Higher coal and gas prices have increased the costs of running power stations and Origin has flagged spending will be slashed to try and balance the books.

From Shane Oliver, AMP Capital: Global share markets fell over the last week, not helped by concerns about Chinese regulatory tightening, a likely slowing in tech sector earnings growth and ongoing worries about a resurgence in coronavirus cases. US shares fell -0.4%, Eurozone shares fell -0.2%, Japanese shares lost -1% and Chinese shares fell -5.5%. The Australian share made it to a new high early in the week but ended the week flat. Bond yields mostly fell, helped in Australia by benign June quarter inflation. Oil and metal prices rose but the iron ore price fell. The $A fell despite a fall in the $US.

Shares remain at risk of a short-term correction or volatility as coronavirus cases rise globally, the inflation scare continues and as we come into seasonally weaker months, but surging company profits in the US and lower bond yields are providing support.

On Friday in the US, the S&P 500 fell 0.5% and tech NASDAQ shed 0.7%, while HK's Hang Seng continued its heavy losses with a further drop of 1.4%.

***

Our Prime Minister, Scott Morrison, is a marketing guy, including as a former Managing Director of Tourism Australia at the time of the 'Where the bloody hell are you?' campaign. He was Federal Treasurer from September 2015 to August 2018 with major responsibilities for superannuation. He was the main architect of changes such as the cap on super pensions, and even on this subject, he showed how nimble he can be with words. So why is super overflowing with unappealing terms few people understand?

For a start, we need another word for a superannuation 'pension' and reserve the word for welfare. It's confusing and inappropriate. A couple with $3.2 million in their pension accounts would not think they are living on a pension, but that's what the account is called. We have lived with CIPRs, or Comprehensive Income Products for Retirement, ever since the Financial Systems Inquiry in 2014, and words like 'salary sacrifice' send the wrong message. Sacrifice is always bad. And let's not start with ECPI and its segregated or proportionate methods (what?!) or NALI or NCC or LISTO or ... I have been at expert sessions at an SMSF Association conference where specialists were confused after half an hour, so what hope do mere mortals have?

You could get arrested in the wrong company by asking: "Psst ... would you like some extension relief on your non-arm's length arrangement?"

And now we have a Covenant for retirement income products. It sounds biblical or maybe a peace treaty. Why not a simple 'agreement'? And here is the definition of 'retirement income':

"Income during retirement, including income streams and withdrawals from superannuation, the age pension, and drawdown of non-superannuation assets."

Get that? Income is spending the capital from both super and non-super assets, not only the earnings. Treasury has released a position paper on the Retirement Income Covenant where members of super funds will be encouraged to spend more of their capital to live on. It's an 'income covenant' but does anyone think a return of capital is the same as income? It's more accurately a spending covenant. We explain how it works, including for SMSFs, and what the products might look like.

Still on retirement incomes, Geoff Warren and David Bell say major super funds will be forced away from navel-gazing to take action over their retirement offerings, but the capacity of members to engage with complex financial decisions is a worry.

Elsewhere last week, The Wall Street Journal noted a remarkable milestone and it shows the challenge of not only recognising a great company at an early stage but hanging on to the investment. From 1999 to 2001, Amazon stock fell in price by 95% as it lost money for 17 quarters in a row and investors ran out of patience. It is 20 years since the WSJ published this story, and the stock fell heavily on the day. Anyone who sold and never went back in is trying not to think about it.

Extract from The Wall Street Journal, 24 July 2001

Said the WSJ: "You know the rest of the story. From that day through this week, Amazon has gained 29,345.1% cumulatively, or a 32.87% annualized total return. The S&P 500 has returned 440.1%, or 8.8% annualized, counting dividends."

The market continues to throw up fascinating examples where it is prepared to pay for future growth as it looks for the next Amazon. The best examples are the growing number of unicorns or privately-owned (that is, unlisted) startups with a current valuation of over US$1 billion. That was once a lot of money, but based on fundraising valuations, a new unicorn has emerged EVERY DAY in 2021. According to cbinsights, there are now 771 unicorns with the largest Australian company, Canva, valued at about US$15 billion.

As investors are increasingly willing to put some of their risk capital to use in these growth dreams, Andrew Mitchell explains how to recognise the next great startups when conventional metrics are useless.

With interest rates so low, investors are increasingly turning to equites for their dividends, willing to take the risk to generate income. Max Cappetta shows which Australian companies are about to deliver handsome rewards for dividend investors, often from non-traditional sources, but stocks should not be chosen simply because they pay high yields.

But it's not stocks that determine the best portfolio returns but overall asset allocation, and Damien Hennessy says the conventional 60% growth/40% defensive mix has thrived in recent decades, especially as bond rates fell. However, the future will be more difficult and he offers ideas to hold up returns.

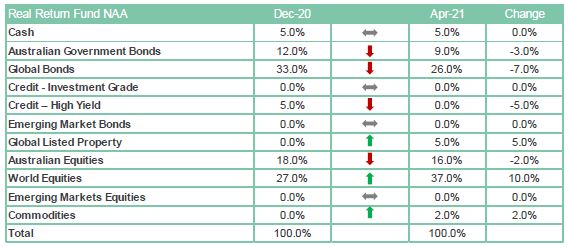

A new financial year is a good time to think about asset allocation, especially as many portfolios might be overweight equities after a long rally. Here is how First Sentier Investors' Multi-Asset team made adjustments to their portfolios in the first half of 2021. Less in bonds due to the downside risk, more in global equities and property due to growth prospects and a dabble in commodities.

On the global stage, we are reminded of the prospects for Japan by the Olympics and Claire Gallagher. She explains why Japan now offers value, diversification and the safe haven benefits after a time off the radar of most investors.

And in bonds, Matthew Macreadie uses Virgin Australia as an example for anyone looking to directly invest in a portfolio of corporate bonds. Despite good ratings before the onset of COVID, Virgin became a bad experience for bondholders showing the risk in a highly-concentrated portfolio of a few names.

The final two retirement income ideas in our series of five (reviewed in more detail in the retirement income article lead this week) comes from Caitriona Wortley explaining protected income strategies using derivatives, while Doug McBirnie shows how pooling of longevity risk might be a solution for some large funds. Lots of new developments coming to retirement income in the next year.

This week's White Paper from First Sentier Investors looks at a part of the property market few people consider: ghost kitchens. The theme takes advantage of our rapidly-changing habits and the increase in ghost kitchen demand is encouraging investment in real estate in the new age economy.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Big investors are divesting from fossil fuels. Lewis Jackson speaks with bulls and bears on the future of these industries. And five cheap names among the biggest changes to Morningstar's fair value estimates since June 2020.

Finally, last week's article by Christine Benz on her faux-retirement was very popular and drew some excellent feedback, but we have chosen Martin Mulcare's response to our thoughts on the politics of superannuation as our Comment of the Week:

"I agree, Graham, that the super industry has not sold itself well. I think this starts with the poor level of engagement that funds have with their own members. My wife and our three children are each intelligent, numerate adults but have no interest in their super because the communication of their various different funds is not at all interesting. I would be keen to hear other reasons for this but let me start with a couple:

1. Communication is compliance driven not customer driven

2. The owners of the communication have traditionally been technical people rather than people people

3. There are no 'diverse customer voices' being heard inside the funds."

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC Monthly Report from Morningstar

Plus updates and announcements on the Sponsor Noticeboard on our website