The Weekend Edition includes a market update plus Morningstar adds links to two of its most popular stock pick articles from the week. You can check all previous editions of the newsletter here.

Weekend market update

From AAP Netdesk: Australian shares had their best day in three weeks on Friday while US jobs figures and a Reserve Bank decision may influence whether the ASX stays near historic highs. Gains for miners and energy providers led the market to rise by 0.5%, set up by Wall Street indices closing at record heights. The ASX 200 is 110 points from its all-time high of 13 August. The nation's two biggest states remain in lockdown and analysts have speculated the Reserve Bank could change its decision to taper bond buying from $5 billion per week to $4 billion per week. The Aussie dollar climbed to over 74 US cents.

On Friday, Rio Tinto improved by 2.5% to $111.37. BHP and Fortescue gained less than 1%. Energy shares were elevated while oil production in the Gulf of Mexico remains mostly shuttered after Hurricane Ida. Shares in Macquarie Group traded for a record high of $169.77. Smash repair group AMA disappointed investors after appearing to prepare a capital raising and then postponing it.

From Shane Oliver, AMP Capital: Global share markets rose further over the past week helped by expectations that the Delta outbreak won’t lead to lockdowns in major developed countries and that the Fed would be gradual in scaling back monetary stimulus, reinforced by a softer than expected rise in US August payrolls. For the week US shares rose 0.6%, Eurozone shares rose 0.1%, Japanese shares gained 5.4% and Chinese shares rose 0.3%. Bond yields fell in the US but rose elsewhere. Oil and metal prices rose, but iron ore prices fell. From their March 2020 lows US shares are up 14 of the last 17 months and Australian shares are up 16 of the last 17 months.

***

The most powerful person in financial markets is not the US President Joe Biden, portfolio managers such as Warren Buffett, bankers like Jamie Dimon, investors like George Soros or politicians such as German Chancellor Angela Merkel. It's not the heads of the biggest asset managers at BlackRock, Vanguard and Fidelity. No, the person who captures the attention of professionals whenever he speaks is the US Federal Reserve Chair, Jerome Powell. He sets the tone for all asset prices and influences the wealth of billions.

As so it was last Saturday, AEST. Each year, the Federal Reserve Bank of Kansas City hosts a conference of the most influential bankers and policymakers, and the main speaker is usually the US Fed Chair. Asset managers with trillions under their control listen for the slightest hint of a policy change.

It's more important than ever. Powell and his central bank colleagues, backed by their governments, have rescued economies from a COVID-inspired collapse, and in so doing, boosted asset prices to all-time highs and made the wealthiest people in the world far wealthier. There is irony that the bastions of capitalism and free enterprise are so dependent on a central banker to hold the system together with unlimited monetary accommodation, desperately hoping he will not utter a suggestion about rising interest rates or anything more than a steady withdrawal of asset purchase programmes.

If you have never read a Fed Chair speech, check it here. It's worth five minutes as it sums up everything about central banks supporting financial assets. While nobody can foresee a black swan event, there is much in there to give confidence that the Fed will rescue the market if necessary. But as IFM Investors CEO, David Neal, told the AIST Conference this week:

"The permanent put option in the market is building in future risk ... I’m a proponent of Stein’s law - if something cannot go on forever, it will stop.”

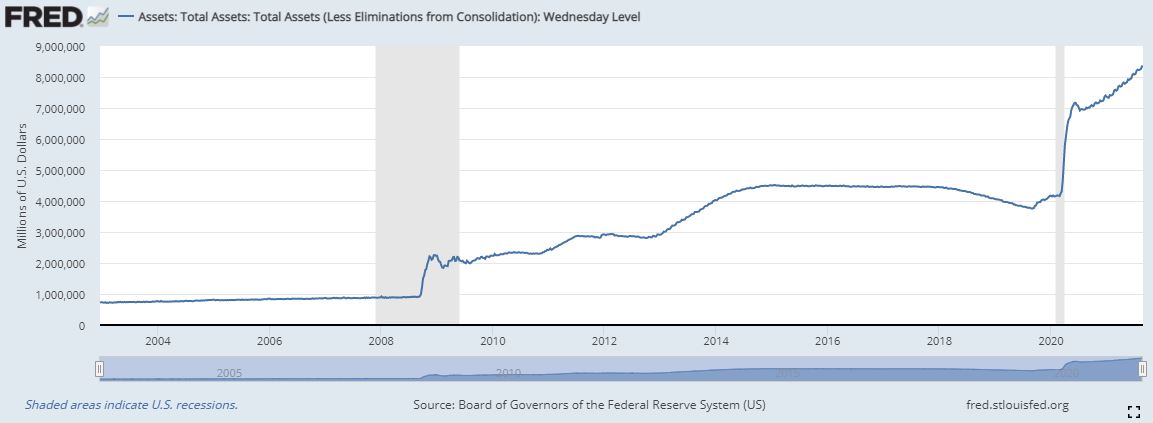

As Powell keeps coming to the rescue, the Fed is buying US$120 billion of bonds every month, not only US Treasuries but mortgage-backed securities. Look at the Fed balance sheet rising to US$7 trillion and the continuing growth over 2021. Next time you read about the billionaire fund managers and their amazing achievements, check if there is any acknowledgement that it is the public balance sheet keeping them there.

Last weekend, Powell did not disappoint. Not only was it 'steady as she goes', but there were so many qualifications on the widely-expected easing of bond purchases that interest rate rises seem years away. Stockmarkets rallied strongly after his speech. He said:

"If the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year ... The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test."

That tough test is the Fed’s target of “maximum employment” which is indeed challenging and there is “much ground to cover”.

At least Powell realises his actions have increased inequality while saving the world. He added:

"The economic downturn has not fallen equally on all Americans, and those least able to shoulder the burden have been hardest hit. In particular, despite progress, joblessness continues to fall disproportionately on lower-wage workers in the service sector and on African Americans and Hispanics.

Powell is patiently aiming for a point where he can signal a gentle reduction in the bond-buying programme, selling it to a nervous market as no longer necessary. As he hopes and expects, inflationary fears will subside and he can ease buying further as the US grows employment, then when things look so good, he might even find a moment for a tiny increase in interest rates. But that sounds a long way off.

This policy of holding down interest rates is sometimes called financial repression (and certainly savers feel repressed), and we explore it further in an interview with Christian Baylis of Fortlake Asset Management, including how he manages his funds in this environment. He also makes the case for the benefits of smaller portfolios. Christian is also a guest on this week's podcast so listen in.

A focus on asset allocations ...

As far back as 1598 when The Merchant of Venice was written, Antonio said:

"My ventures are not in one bottom trusted, nor to one place; nor is my whole estate, upon the fortune of this present year.”

Shakespeare knew about diversification.

And so at this time of year, when we find out more about the asset allocation decisions of our major institutions such as the Future Fund, we look at Jerome Powell's own investments. Unlike Australia's leaders, he has plenty of exposure to equities, not that we are suggesting this influences his policy positions in any way.

To celebrate his 94th birthday, we revisit our fascinating interviews with Harry Markowitz, the 1990 Nobel Laureate and Pensions & Investments Magazine's 'Man of the Century'. He explains a magic 'aha' moment on risks and returns and how he arrived at his Modern Portfolio Theory and Efficient Frontier.

One amusing vignette from the conference where I interviewed Markowitz shows how competitive and bright Markowitz is. The 2011 Nobel Prize winner, Chris Sims, had just finished a highly technical presentation on how fiscal policy affects inflation. As he paused for questions, Harry was first in. “Now we know how you got your Nobel Prize, let me show you how I got mine.” And he gave his critique of the presentation as if lecturing at a university.

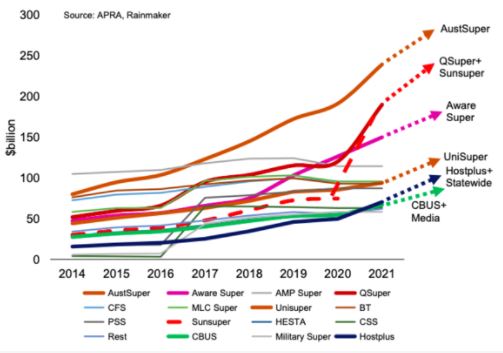

It is a massive week for large superannuation funds and trustees with APRA releasing its performance list under the Your Future, Your Super legislation. David Carruthers checks the calculations and warns of the unwelcome and unintended consequences.

A few industry funds made the underperformers list, and despite their explanations of specific mitigating circumstances, they are now in APRA's sights. These funds will no longer be able to use the 'cupped hands' branding and 'compare the pair' advertising of Industry Super Australia. The latest Rainmaker forecast says that if current trends continue, only 10 super funds will administer 80% of APRA-regulated funds under management by 2025. Here are their expected winners.

Super fund asset forecasts to 2025

Still on asset allocation, what about gold? There are plenty of portfolios hedging their bets some exposure to precious metals. While gold prices have generally lagged the impressive bond and equity returns in the last decade, what about the next 10 years? Jordan Eliseo expects more even investment conditions.

Contrary to the expectations driving the current rush to buy houses and predictions of further rises over 2021 and 2022, Tim Toohey argues the risk of lower house prices over the next two years is high. As our biggest asset class, there are widespread implications for banks and the economy.

In our latest Wealth of Experience podcast, Peter Warnes finds the winners and losers from the August reporting season, and we discuss the main point critics of franking credits are missing miss and how the NSW stamp duty reforms pick winners. Plus we each have a bit of a grump.

Interesting to read what the rest of the world thinks about Australia's efforts during COVID-19. This is The Economist on 28 August 2021:

"Early in the pandemic, Australia appeared a shining success story. By closing its borders, tracing contacts and rigidly enforcing quarantine restrictions, its “covid zero” strategy seemed to be working. (Geography helped, too: it is easier to keep a virus at bay on a remote island than in a country with long land borders.) The Delta variant has ended that strategy. As one doctor in Melbourne noted, even if contact tracers find an infected person within 30 hours, that person’s contacts would already have passed the virus down several chains of transmission. The country is now putting its hopes in vaccines, and will allow cases to rise as long as hospitals can cope."

A fair summary as we fall behind many countries with a locked up economy and a gradual acceptance that we will need to live with the virus, rising case loads and deaths.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Many industries looking to go green still need a kind of explosive, high-heat power that batteries can’t yet provide. Hydrogen fits the bill. The global market is heating up writes Andrew Willis. And, would you have bought Berkshire Hathaway in 1975? Probably not, based on the performance charts says John Rekenthaler.

Finally, the franking credit article last week drew some fantastic comments in a high-quality debate with over 100 comments. I really believe some of the explanations in the comments are the best and clearest anywhere, so it's worth another look. The Comment of the Week from Kevin is typical:

"I earn $100K in franked income outside of super, as I planned. They take $30K tax off that. I net $70K. I do my tax at the end of the year. The tax on $100K is $25K.They give me a $5K rebate, great. Exactly as if I was working. Fully self funded, I also draw $36K out of super, tax free, great. On a gross income of $136K, they take the pension off me ($36K), they also take $25K franking credits.

In the world of hypotheticals, look over there, what about etc, this $61K that they take off me doesn't exist. The $61K they take off me isn't called 'tax' so it isn't real. I really do laugh at people as they say I rort the system, I cheat. I am very happy I contribute that $61K to society (plus Medicare levy) I can afford to do it.

They complain 100% of the time. If they spent 1% of that time working out how this very simple system works, they would be much better off."

This week's White Paper from UBS continues the asset allocation theme where they look at equities and bonds in different conditions (especially adjusting for inflation) and forecast returns from a typical 60/40 portfolio. Don't expect the riches of last year to be repeated.

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

Airlie Roadshow 2021 - Australian Equities: the outlook is brighter than you think. Live broadcast 9 September 2021, 11:30am (AEST). Register here.

IAM Capital Markets' Weekly Market Insight

Australian ETF Review from Bell Potter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website