The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two additional articles.

There is a common frustration among investors and financial advisers that obtaining a single piece of advice - such as should I salary sacrifice? or should I invest or repay my mortgage? - involves a lengthy consultation process and a 70-page Statement of Advice. It increases the cost and complexity of financial advice and is a reason the Quality of Advice Review was commissioned. But it is easy to understand why it is necessary. How can anyone answer these questions without knowing a bigger personal picture, especially about long-term goals?

We're all different. I might think borrowing to invest in equities is too risky (yes, I do believe that at the moment) but another person might say we are near the best time for equity exposure, when markets are gloomy. They might be correct, as Ashley Owen's article explains this week, that recessions are usually good for stock returns. It's all in the timing and the cycle of investing, and maybe pessimism is a buy signal.

Our lifestyles are also different, especially the need to forgo something in the present in return for something in the future. Retirement security usually requires saving rather than spending, and buying a home rather than consuming, but plenty of people want the designer clothes, the flash cars, the fancy vacations and the latest tech. It's their life, their goals, their decisions, their consequences, making financial advice rarely a one-size-fits-all.

In car racing, a solid green flag is waved to start a race. In share markets, nobody waves a green flag to start taking on more risk. As famous asset manager, Howard Marks, said:

“I spend a great deal of my personal time trying to figure out one thing, which is, at a given point in time, how should you balance aggressiveness and defensiveness in your portfolio.”

For example, stockmarkets in Australia and overseas kicked up strongly last week, in the hope that the pace of interest rate increases would slow. The S&P/ASX200 was up 4.5% last week, its best few days for two years. According to Calastone, managed equity funds in Australia enjoyed $3.5 billion of net inflows between July and September 2022, well up on the previous quarter. Overseas, BofA Securities reported:

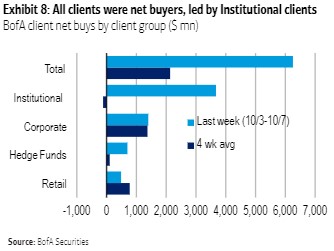

"Last week, during which the S&P 500 rallied 1.5% off recent lows, clients were big net buyers of US equities ($6.1B; third largest inflow in our data history since '08 and the fifth consecutive week of inflows). Our view? More volatility likely ahead."

Get that. The biggest net buyers of equities since 2008. At the same time many are protecting their portfolios with cash, as central banks confirm further interest rate rises, as recessions loom and as Federal Treasurer Jim Chalmers appears on the news each night looking like he's swallowed a lemon, investors are piling into equities. The IMF update this week trimmed economic growth by 0.2% to 2.7% next year, and said:

"More than a third of the global economy will contract this year or next, while the three largest economies - the United States, the European Union and China - will continue to stall. In short, the worst is yet to come, and for many people, 2023 will feel like a recession."

What is the answer if someone asks, "Is it a good time to buy CBA [or another stock]?" We all have different investment horizons. It can vary from a day trader who wants to know what's happening at that moment to trade CBA over a few hours. Then all the way to someone investing for a retirement lifestyle and income over 30 years, which involves a broad assessment of long-term markets and CBA's position in Australian banking.

So spare a thought for the financial adviser asked to give a single piece of advice, which legally they are not supposed to do anyway. We would not expect a doctor to recommend heart surgery without a lot of tests and a knowledge not only of personal health history but that of the patient's family. In recent weeks, ASIC's Financial Advisers Registry (FAR) has recorded a loss of about 500 experienced advisers bringing adviser numbers below 16,000 from a peak of double that. Most of the losses were due to advisers failing exams. There's a lot involved in answering what seem like simple questions.

And everyone is desperate for some expert guidance on where markets are going. In recent presentations, among the first questions directed to me have been, "What do you think of physical gold?" and "Where is the Australian dollar going?" I prefer to talk about long-term asset allocation and portfolio construction, and the audience wants my macro guesses. Someone arranging a conference recently asked me to present but then lost interest when I said I do not pick stocks. Some people get what they deserve.

While I might think someone is looking in the wrong place for their investments, something else is top-of-mind for them. I am reminded of a joke:

"One night, a policeman sees a drunk searching under a streetlight and asks what he's looking for. He drunk says he lost his keys, and the policeman starts searching under the light. After a while, the policeman asks if the drunk is sure he lost the keys there. The drunk replies, "No, I lost them over there in the park." The policeman asks why he is searching over here, and the drunk replies, “This is where the light is.”

In this week's edition ...

The Optus hack has raised the fear of identity theft, and at the same time, market participants are frustrated that financial market processes seem stuck in the dark ages, with many managed funds not changing their ID and application processes for decades. At a recent Connect Forum arranged by Calastone, Annick Donat, CEO of Clime Investment Management, said:

"This industry is highly regulated, but not to its benefit, not to anyone's benefit in the value chain or the ecosystem. And I sit here over three decades, and we're having the same conversation that we were having three decades ago. We've changed nothing, nothing at all. We've created more friction, not less. And we're supposed to be an advancing industry looking after people other people's money."

We take a look at 'tokenisation' (terrible word) as a potential solution to the confidentiality problems faced by Optus and all financial institutions. How do we make investing easier without compromising the identity checks which are essential for public confidence and to prevent cyber crime? It's part of the blockchain revolution relevant to all of us as we seek to reduce friction without damaging our security.

Regardless of our market expectations, we need a place to invest our super, and Annika Bradley of Morningstar takes an independent look at the likely structure of the coming Vanguard offer, and how it compares with a similar fund currently available from the largest super fund in the country, AustralianSuper. These are valid alternatives for every SMSF investor (and look out next week for Meg Heffron's take on when an SMSF should be closed and the money moved to a public fund).

In the almost 10 years of Firstlinks, one of the most-viewed topics was our extensive coverage of the franking credit proposals before the 2019 Federal Election. Although nowhere near the same scale as a policy, a new franking credit proposal from the Government is attracting plenty of attention, and Matthew Collins explains what the fuss is about.

It's Year 12 exam time, and Angus Dennis of Australian Ethical checks the latest subject changes in the Economics exam, and finds far more focus on externalities, private versus public goods and sustainability. Pass his thoughts to anyone sitting the exam in coming weeks, and best wishes to all students.

Last week's article on homeowner-retirees not running out of money drew about 20,000 views and lots of comments, and we continue this theme with research by Helen Baker of money.com.au on the expectations and aspirations of Australians heading into retirement.

Back to security fraud and the obvious connection to cryptocurrencies. While superannuation is usually at the conservative end of investing as retirees seek to preserve capital, SMSFs have invested about $1.5 billion in crypto assets according to ATO data, up from only $240 million in two years. It's a small part of the $840 billion in SMSF assets but likely to rise as more younger people establish their own funds with investing freedom.

Some SMSFs have been subject to crypto fraud, such as reported by The Australian Financial Review:

"Queensland-based cryptocurrency, digital asset exchange and brokerage Mine Digital has collapsed and control handed to external administrators, amid a dispute where it is being sued for allegedly not doing enough to weed out scammers from its platform."

Dr Paul Mazzola and Mitchell Goroch look at how regulators should control the rapid growth of crypto.

In the two new articles for the weekend, Nicola Chand highlights five charts from a Morningstar report called an Industry Pulse on Australian banks, while Dave Sekera makes the case that US stocks are undervalued despite high inflation and weak economic growth.

This week's White Paper from VanEck called "In the Fed, we trust" looks at how completely the US Federal Reserve is determining the direction of bond and equity markets, and the implications.

Graham Hand

***

Weekend market update

On Friday in the US, the pessimism returned with the S&P500 losing 2.4% and NASDAQ down 3.1%. Tesla was a drag with shares off over 7% taking the loss since November 2021 to 50% as fears of recession added to misses on delivery schedules.

From AAP Netdesk: On Friday, the local share market gained across the board after some extreme volatility on Wall Street overnight following the release of monthly United States inflation figures. The benchmark S&P/ASX200 index finished up 116.2 points, or 1.7%, to 6758.8 after US shares staged a massive comeback on Thursday in one of the biggest one-day reversals in Wall Street history. The Dow Jones surged 1,500 points off its lows and the S&P500 snapped its six-day losing streak to close up 2.6%.

Friday's rally wasn't quite enough to offset the losses on Monday and Tuesday and for the week the ASX200 closed slightly in the red. It is up 4.4% so far this month, but down 9.2% for the year.

The energy sector was the biggest gainer on Friday, rising 3.8% as Woodside climbed 4% to $33.95 and Santos added 4.4% to $7.80. Coalminer New Hope finished up 2.1% to an all-time closing high of $6.86, while Whitehaven Coal added 2.1% to $10.82. The big banks finished at their best levels in several months. Bank of Queensland, whose strong full-year earnings report on Wednesday apparently inspired the rally among its larger peers, finished up 1.6% to a five-month high of $7.73. In the heavyweight mining sector, BHP gained 2% to $40.02, Fortescue Metals rose 0.7% to $17.11 and Rio Tinto advanced 1% to $96.61.

From Shane Oliver, AMP: Shares had another volatile week that left US stocks down 1.6% for the week, Eurozone shares up 0.1%, Japanese shares down 0.1% and Chinese shares up 1%. The near-term downside risks for shares remain reflecting the array of macro risks – ultra hawkish global central banks, high and still rising recession risks, the $US still trending up on global safe haven demand risking a financial accident, ongoing policy mayhem in the UK, an escalation in the conflict in Ukraine and continuing downwards revisions to earnings expectations. And despite lots of bounces sharemarkets remain stuck around or just below their June lows, a decisive break of which could open up another 5-7% leg down.

US September consumer and producer price inflation surprised on the upside with the CPI up 8.2% yoy and the core CPI up 6.6% yoy. While goods inflation continues to slow, services inflation is continuing to pick up driven particularly by strong gains in shelter (which is mainly rent), medical care and transport services. This will keep the Fed hawkish for now and on track for a 0.75% rate hike next month with the risk it does another 0.75% in December rather than slowing to 0.5%.

Latest updates

PDF version of Firstlinks Newsletter

Cboe Australia: Investor Day 2022, 20 October 2022. As financial markets are roiled by aggressive changes in monetary policy and shifting geopolitics, hear from leading local and global investment managers. Register to secure your spot.

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website