If you were offered $100,000 worth of CSL shares at 80% of their current market price, what would you do? Easy. Buy them and make an instant $20,000.

What if you could buy CSL at the same discounted price but not sell the shares for at least three years? Most people would probably still do the deal, as a 20% discount on CSL would be hard to resist.

Now, what if instead of CSL, the 80% offer was on a diversified portfolio of quality shares selected by a prominent fund manager? Pay 80 cents for $1 of their favoured selections. In theory, it’s better than the CSL shares because the portfolio is diversified and backed by an expert team’s opinion. Still hard to resist, even with no requirement to hold for a set period?

Every day of every week

Welcome to the world of Listed Investment Companies (LICs) and Listed Investment Trusts (LITs), a sector of the market valued at over $40 billion in 111 listed vehicles.

You can do the 80% deal every day of the week. There are so many LICs and LITs managed by well-known names regularly trading at significant discounts to their Net Tangible Assets (NTA) value that it’s hard to know where to start. But unlike the CSL example, there is a risk the discount will go even wider.

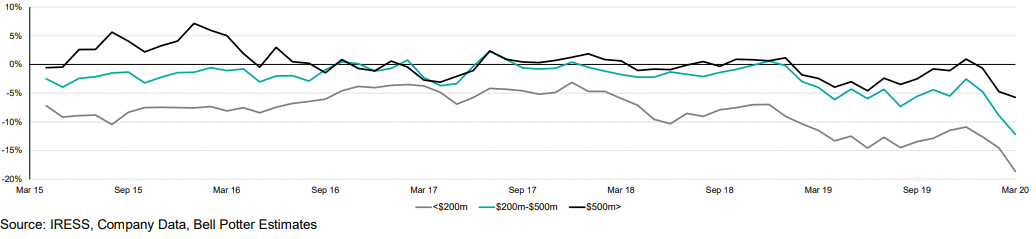

Bell Potter’s chart below from its latest Quarterly Report shows trading levels relative to NTA for LICs and LITs according to size. The average discount of those issues with a market value of less than $200 million was close to 20% at the end of March 2020, and many remain around this level in June.

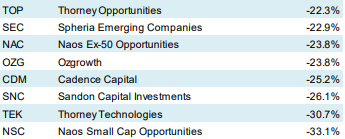

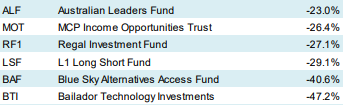

The Quarterly Report included the following listed vehicles trading at discounts greater than 20% in the three sectors of Australian equities, global equities and alternatives as at 30 March 2020. For a check on more recent prices, see our Education Centre.

Australian equities

Global equities

Alternatives strategies

In case some of the above names are unfamiliar, consider other famous fund managers who missed the 20% cut-off but their discounts were still over 10%:

- QV Equities (Investors Mutual) (QVE), -14.4%

- Ophir High Conviction (OPH), -13.5%

- Magellan Global (MGG), -10.2%

- Platinum Capital (PMC), -11.2%

- Templeton Global (TGG), -17.1%

- Antipodes (APL), -17.1%

- Perpetual Credit (PCI), -14.5%.

Let’s face it, it’s unacceptable that retail investors cannot sell near the value of the underlying shares, especially during a critical time such as the need for money during the pandemic. The discounts are in addition to the falls in the value of the assets. These are among the highest-profile, most-respected fund managers in the country. Yet for many reasons, investors do not support their listed vehicles in sufficient numbers to sustain a share price near NTA (examples are pre-tax NTAs, and in most cases, post-tax NTA comparisons are worse).

In investing, where there are thousands of competing funds all looking for a marginal edge, 10% to 20% is a big deal. If a fund manager were able to deliver a consistent 1% per annum above a broad market index over the long term, and tell a good story, the investing world would beat a path to his or her door. Most active managers do not beat the index after fees, and would happily settle for 1% outperformance. Yet here we have significant discounts to the market value of the underlying assets, forcing investors to hang around in hope or sell at a big relative loss.

Five famous fundies with heavily-discounted LICs

Let’s select five high-profile managers with ‘cheap’ LICs, defined as trading at a discount to NTA of about 20% as at the latest NTA disclosure (generally, 5 June 2020). None of these are recommendations, but clearly, if anyone likes the fund manager and believes the NTA discount will narrow, it could be a good entry point.

(Investors should check the latest price relative to NTA as changes in absolute and relative terms occur every day).

1. Australian Leaders Fund (ALF), price $0.90, NTA $1.14, discount 21%

ALF is managed by Justin Braitling and a large team at Watermark Asset Management. ALF is not one of the new breed of funds jumping on the LIC bandwagon, having been established in 2003. ALF is differentiated by its absolute return strategy and long/short positioning, and although this protected the NTA during the March 2020 coronavirus sell off, the share price did not respond. After some early success, ALF has struggled to attract support for many years and remains at a wide discount.

2. Thorney Opportunities (TOP), price $0.50, NTA $0.62, discount 19%

The portfolio manager and chairman of Thorney is Alex Waislitz, regularly featured in the media as a ‘billionaire investor’ (see below from the front page of The Australian Financial Review on Tuesday this week). In the 2018 Rich List, he was estimated to be worth $1.39 billion and in the same year, the Thorney Investments Group celebrated its 25th anniversary. All the ingredients for success sound right to find market gems (he was early into Afterpay and Zip) but the retail investor support is disappointing.

3. PM Capital Asian Opportunities (PAF), price $0.73, NTA $0.92, discount 21%

Paul Moore is the founder and chief investment officer of PM Capital. Moore had a long career at the famous investment powerhouse of its time, BT, before establishing his own business in 1998. PM Capital also has a large team of experienced managers, but Moore’s investment approach is as a value manager, a style generally out-of-favour versus growth in recent years. Moore is better known as a global manager rather than Asian-specific, but even the global fund (ASX:PGF) is at an 18% discount.

4. Cadence Capital (CDM), price $0.65, NTA $0.87, discount 25%

Karl Siegling established Cadence in 2003 and listed CDM in 2006. Over nearly 15 years, the fund is ahead of its benchmark but recent years have been tough, underperforming the All Ords Index by 7% over the last five years. Cadence makes a feature of the fund that the management team are the largest shareholders so at least they are suffering alongside retail investors.

5. Spheria Emerging Companies (SEC), price $1.41, NTA $1.85, discount 24%

For variety, let’s consider a younger boutique that is part of the large Pinnacle Group. Spheria’s investment team includes three fund managers with over 40 years of experience in the small-cap market. SEC is a listed version of its unlisted Smaller Companies Fund, so why would anyone invest at NTA in the unlisted fund when the listed vehicle is offered at a 20+% discount? SEC came to market in November 2017 at $2 and reached its minimum target of $100 million in only two weeks, based on previously outperforming its index by 6.5% in the year before IPO. Since launch, the loss from $2 to $1.41 mainly comes from the discount to NTA and market falls but the fund has also underperformed its index.

All of these managers need to find a catalyst for the market to believe in their skills and styles and the merits of the LIC structure.

A weakness of structure as well

No doubt the discounts in the sector say as much about the weakness of some LIC and LIT structures as the fund itself, as the only liquidity comes from finding a buyer on the market. It should also be acknowledged that some LICs trade at a premium and benefit from active marketing by their managers or good economies of scale.

But there’s no way to gloss over it. Billions of dollars were invested in the best names in Australian funds management, every investment originally costing NTA (or worse if fees were involved), and now most of the issues trade at a discount.

And there is a residual adverse impact from the commissions paid to brokers and advisers to place LICs and LITs, which have now been banned. The reputation of the structures took a hit when some massive transactions traded at a wide discount, and investor trust is slow to return.

It's one reason why some managers are moving into active exchange-traded funds (ETFs), where there is an in-built market-making function which ensures trading close to the NTA value.

Perhaps it needs a major consolidation where the big funds take over the minnows. It might be better from the investor's perspective to turn some funds into unlisted vehicles in an open-ended vehicle which trades at NTA, or an active ETF, as long as managers are willing to face redemptions. Ouch! Less funds under management means less fees.

Graham Hand is Managing Editor of Firstlinks. Graham owns some of the issues mentioned in this article, much to his chagrin. This article is general information and does not consider the circumstances of any investor.