Capital gains tax is once again the subject of parliamentary debate, with Treasurer Jim Chalmers declining to rule out options for reform.

Along with negative gearing, the capital gains tax discount has long been suggested as one cause of Australia’s housing affordability crisis.

The tax applies to the capital gain when an asset is held for more than a year, and it currently includes a “discount” of 50% on the total gain as a nominal offset for inflation.

These policies make speculative investment in housing more attractive, driving up prices and making it harder for first home buyers.

The true cost to the federal budget

Australia only introduced a capital gains tax in 1985, applying it to all gains made from investments. Importantly, the family home was not included, but investment properties were. Originally, the tax applied to the gain in value above inflation, known as the consumer price index (CPI) method.

In 1999 the Howard government, informed by the Ralph Inquiry, changed the way capital gains tax was calculated. A flat 'discount' of 50% was applied to capital gains, rather than adjusting the price by inflation. This figure was an estimate given the limitations with the available data.

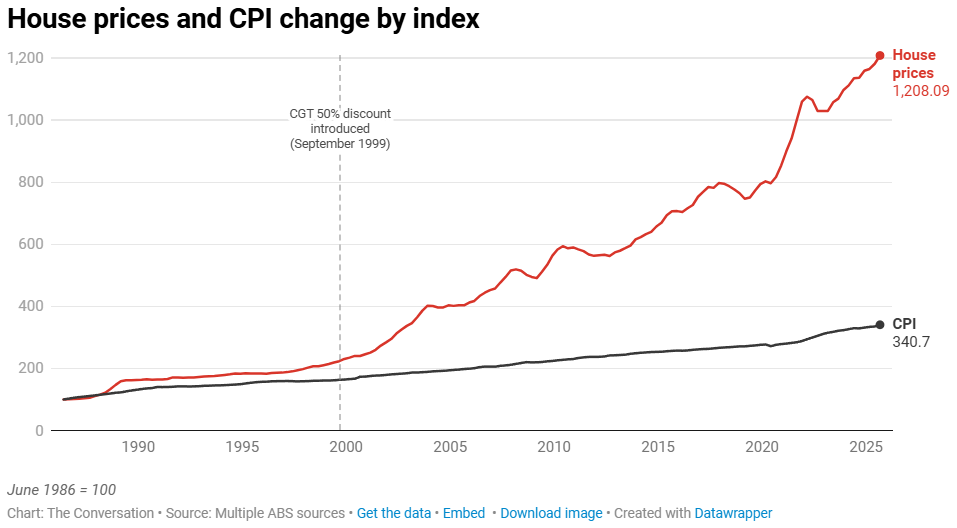

Each year, Treasury calculates the costs of tax policies. This data reveals that in 2024–25 the 50% discount cost the budget an estimated $19.7 billion. This is partly driven by increases in housing prices which have far outpaced inflation, as shown below.

It is notable that between 1986 and 1999 housing prices were growing slightly faster than inflation, but since 1999 (the year the 50% discount was introduced) they have accelerated.

The benefits flow to the wealthy and people over 60

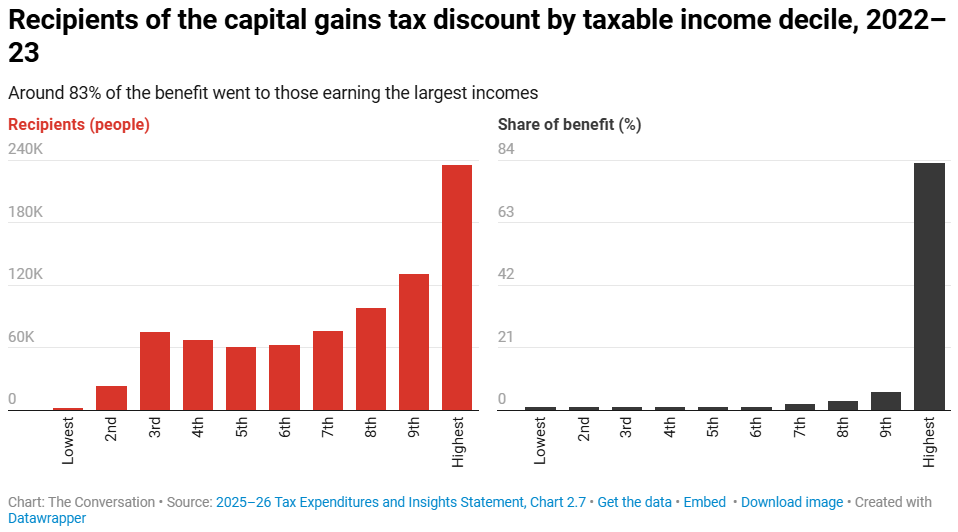

The benefits from the capital gains tax discount overwhelmingly benefit the wealthy and older people.

The Treasury’s Tax Expenditure and Insight Statements show that in 2022–23 89% of the benefit went to the top 20% of income earners, with 86% flowing to those in the top 10%. On average, the highest income earners received a benefit of more than $86,000, while those in the bottom 60% received around $5,000.

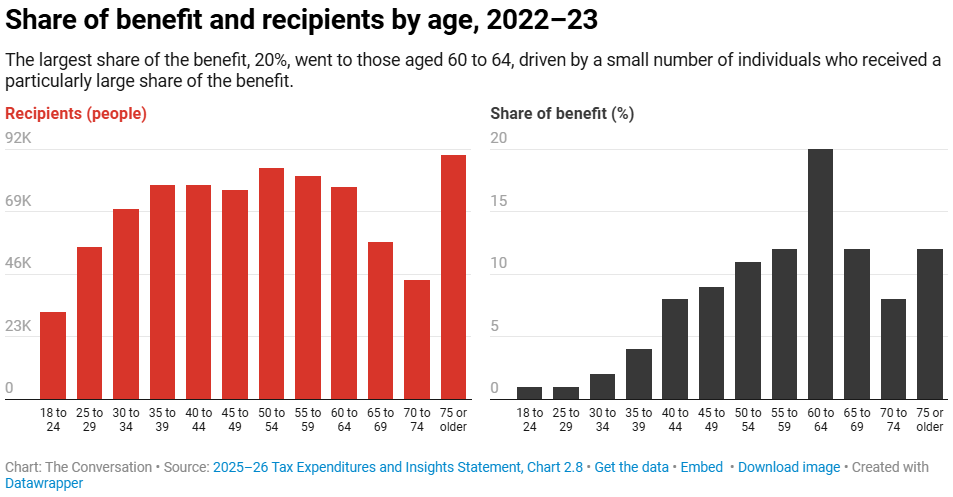

Similarly, older people benefit far more than younger people. People over 60 received 52% of the benefit, while those between 18 and 34 received 4%. That is despite both groups comprising around 29% of the adult population.

Some options for reform

Current attention is centred on the prospect of the government reducing the capital gains tax concession for landlord investors in residential property. This reduction would have the combined effect of reducing the attractiveness of owning an investment property.

A further option is to retain this 'gift' to landlords and investors, but to make it work much harder to improve housing outcomes, especially for households who are caught in the lower-quality end of the private rental market.

We have previously proposed to make negative gearing and capital gains tax concessions available only to investors who adhere to higher national dwelling and tenancy quality standards or who participate in social housing investment schemes. Landlords who did not want to operate according to these requirements would not receive either negative gearing or capital gains tax concessions.

How the housing system rewards wealth, not work

But a bigger problem lies beyond the investor segment of the residential housing market.

The total overall value of Australia’s residential stock is around $12 trillion. Of this, about $4.5 trillion is growth since 2020, spurred in part by very low interest rates over 2020–22. Around 65% of residential dwellings are owned by owner-occupiers, who are exempt from paying capital gains tax on their primary residence.

Growth in dwelling prices is due to many factors. Income growth and availability of credit are among the most important.

Since the deregulation of Australia’s financial sector in the 1990s, greater access to housing finance and relatively low interest rates have allowed households to leverage their incomes into tax-free capital gains in housing.

Wealthier households can gear their incomes and existing assets into even more valuable housing assets that they can also live in. This comes at the expense of households with lower incomes and assets, or those who are renters.

There is no sound economic reason why owner-occupied housing should be exempt from capital gains tax.

A more rational taxation system that supports home ownership but discourages asset speculation could provide greater financial support to first home buyers but also demand a greater tax share of the capital gains that their asset enjoys.

The tax rate could be set to allow capital growth in line with inflation, wages or the economy (gross domestic product), but then apply to the gains beyond that.

Such an arrangement could also tax higher-value properties at a higher rate than cheaper properties – thus tilting the burden of taxation towards the wealthy whose properties see the greatest capital growth.

Is housing a human right or an asset?

Ultimately, there is a more fundamental question to be answered about role of housing in society.

While housing has always had a speculative dimension in addition to providing shelter and comfort, the past 30 years since financial deregulation has seen the balance shift in favour of the former.

The question facing the current government is to what extent it is prepared to reduce speculation in housing in favour of the social purpose of housing? Does it have the appetite for a structural reset that prioritises housing as a home, rather than as a debt-geared speculative asset?

Is this a government of nervous tweaks and twiddles, or might the dire times in housing embolden landmark transformation? Can the values that Labor espouses be translated into progressive policy?

Jago Dodson, Professor of Urban Policy and Director, Urban Futures Enabling Impact Platform, RMIT University and Liam Davies, Lecturer in Sustainability and Urban Planning, RMIT University

This article is republished from The Conversation under a Creative Commons license. Read the original article.