In the midst of the public market run-up of the last three years, private equity has advanced, but not to the extent that investors have previously been accustomed. Off the highs of 2021, slow dealmaking has limited ‘exits’ from portfolios, fostering an attractive opportunity for liquidity-oriented strategies, such as general partner-led ‘continuation’ transactions, co-investments and capital solutions, as well as a heightened focus on the secondary market (see “Current Opportunities” below). Recently, however, activity has started to recover, with a rise in initial public offerings and M&A activity resulting in an increase in distributions to investors through the third quarter of 2025 versus the same period in 2024.1

What could happen from here? We have reason to believe that a slow normalization of the market is emerging, slowly trimming the inventory of private investments and making use of elevated ‘dry powder’ from investors seeking to capitalize on private markets’ historically favorable risk/reward characteristics. In our view, the liquidity solutions noted above should continue to play a pivotal role in this process. More broadly, at a time when public equity is reaching extended valuations, we think private market prices look relatively reasonable. (See our Private Equity Outlook for further details.)

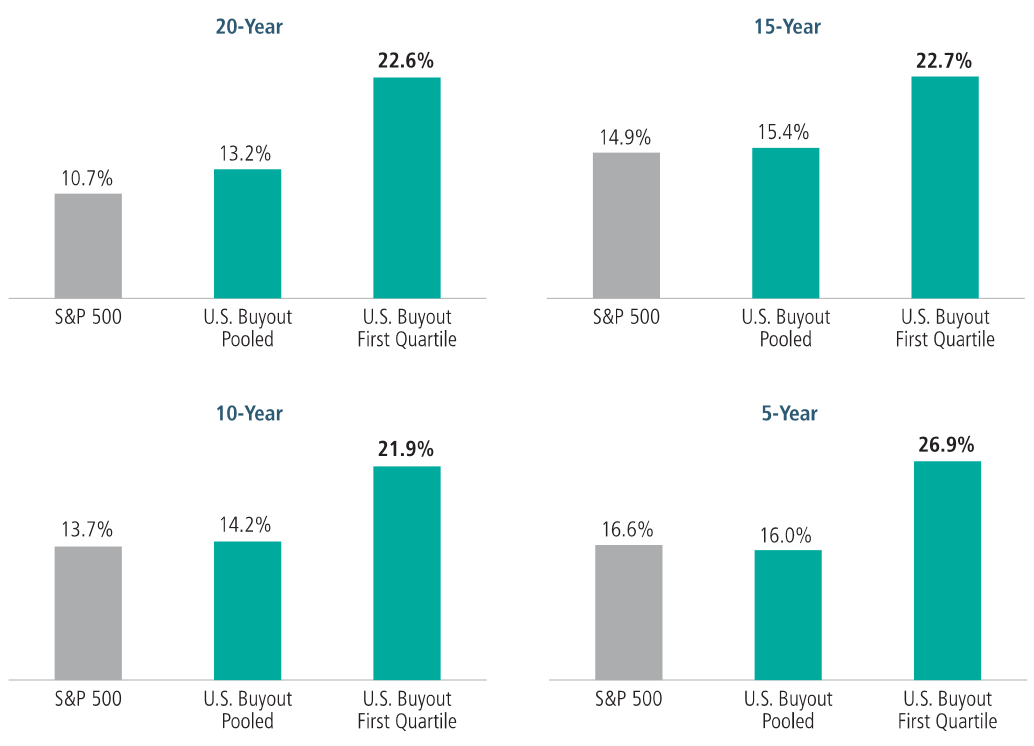

Figure 1: Private equity has provided strong long-term results

Annualized total return

Source: Private equity data from MSCI (formerly Burgiss). Represents pooled horizon IRR and first quartile return for U.S. Private Equity as of 2Q 2025 which is the latest data available. Public market data sourced from Neuberger as of 2Q 2025.

That said, we live in a highly volatile world, with numerous forces affecting economic and market dynamics. Attention to key secular forces could be highly important in seeking to achieve success in private markets over the coming years. We explore them below.

The Seismic Six

1. Artificial intelligence

AI-driven disruption is now everywhere, affecting consumer behavior, business models and the markets. For private market firms, the impact will relate not only to investment choices, but to how those firms run their businesses. In our view, the best practitioners are investing in AI for use in evaluating portfolio companies, streamlining operations and enhancing their sourcing for deals. Private market firms that enthusiastically embrace AI and have sufficient in-house resources and expertise should be better positioned to determine the winners and the losers in the new environment.

In terms of exposures, the buildout of AI data centers and the energy capacity needed to support them will continue to be a major trend in which private capital should be a major player. Investment opportunities could extend to industries and businesses across the economy that leverage AI to their advantage.

2. Economic uncertainty

For much of the past 40 years, private markets generally enjoyed decreasing interest rates and increasing valuations, often obscuring differences in quality across companies and transactions. That ‘free lunch’ appears to be over, as we enter a period where interest rates, while likely trending down, could remain higher for longer, limiting potential upside for valuations.

This could put the onus on private market firms to make money ‘away from the market’, by creating value in their portfolio businesses in order to generate potential returns. Those who invest heavily in internal resources like AI expertise can help their portfolio companies and make strategic and operating improvements that accelerate their companies’ earnings growth and make them more appealing to potential buyers.

3. Deglobalization and populism

The fragmentation of the global economic system continues unabated, driven by the growing influence of populist political movements, as well as competition and geopolitical rivalries. Deglobalization has been evident for some time but has accelerated in the wake of the pandemic and amid growing interest in reshoring to insulate supply lines and maximize benefits to domestic populations.

The April ‘Liberation Day’ tariff announcements were a part of this shift, unsettling markets and freezing mergers and acquisitions as businesses awaited clarity on key decisions tied to tariffs and other business limitations. Continued economic activism on the part of governments will likely remain in place and result in significant market volatility moving forward.

While private markets will likely be affected, we believe that they can help mitigate some of the risks of this volatility. For example, our analysis suggests that private equity investments are less exposed to tariffs than public counterparts, largely by virtue of the types of industries favored by PE managers, including domestically oriented technology and business services.2 This means that private markets could offer valuable diversification from global economic risks. More basically, the long-term and nimble nature of private capital should help managers navigate or avoid many challenges as they arise.

4. Changing investor base

The mix of investors in private markets is shifting rapidly, with individuals and sovereign wealth funds taking an increasing role. For different reasons, these investor groups prefer or need larger platforms with stronger brand names, which has tended to drive fundraising to major players. In 2024, for example, just six private market firms raised 60% of the money in the asset class, up from 20% five years earlier.3 Moving forward, we expect this trend to remain intact.

For individuals, such growth is tied to the emergence of ‘evergreen’ funds with reduced minimums and investment restrictions that provide more access to private market diversification. For large managers, the trend requires continued discipline in the amount of capital they will accept and deploy. Ironically, the trend creates opportunity for successful middle market firms as competition for deals softens given the fundraising struggles of their peers, and the middle market leaders’ ability to exit investments by selling high-quality assets into large pools of capital raised by the mega-cap fund managers.

5. Increased M&A and public offerings of private market firms

A wave of mergers and acquisitions and initial public offerings is taking place among private markets firms. Strategic combinations can provide the deeper resources needed to serve the retail investors noted above and to enhance global reach, whether for fundraising or distribution. Meanwhile, traditional asset management firms are seeing acquisitions of private market firms as a way to enter the fast-growing private segment. Some of these deals could be highly successful, providing better strategies and services to clients, but they may come with operational risk tied to clashing cultures and employee turnover, reinforcing the need for selectivity in deal and manager selection.

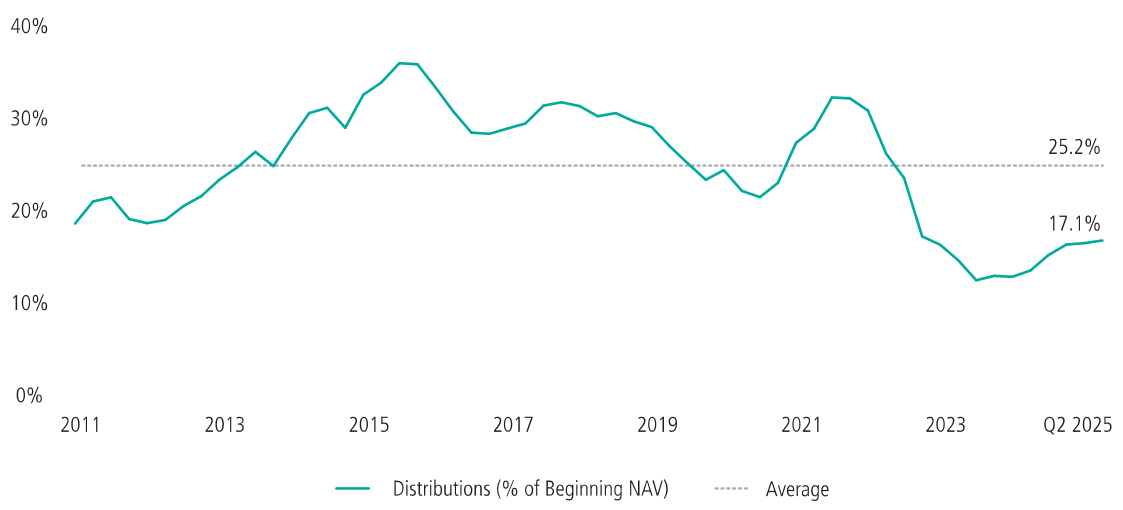

6. The liquidity crunch

Even though the M&A and IPO markets have rebounded, the private markets must work through existing inventory to move toward a more normal environment for exits, elongating the average hold period of a typical investment. That means that liquidity, although improving, is likely in the beginning of a multiyear normalization period.

Figure 2: The liquidity spigot is loosening—slowly

Buyout fund distributions as % of beginning net asset value (last 12 months)

Source: NB Alternatives Advisers analysis as of August 2025. Represents pure private equity primary investments, excluding venture capital as of 2Q 2025. Figures are simple averages.

The good news is that these conditions have created meaningful opportunities for some private market strategies. One is secondaries, where a continued imbalance between skeptical investors and eager sellers is creating what we consider a buyer’s market with more deals than capital raised. ‘Midlife’ co-investments are also benefiting. Here, general partners may sell a portion of their holdings in typically strong portfolio companies to gain liquidity for investors or to generate capital for continued growth. The companies sold will have a track record under current ownership, reducing the ‘blind pool risk’ that may exist with more traditional buyout transactions. So-called capital solutions or hybrid capital, which utilizes highly structured equity, preferred equity or credit solutions, are also getting traction as a means to manufacture liquidity while accessing capital to execute strategic plans.

The bottom line? Strategies that can fill that illiquidity gap can take advantage of it for the potential benefit of their investors.

The big picture

Seismic change is reshaping private markets, challenging old paradigms and accelerating industry transformation. In our view, investors should expect greater dispersion of returns and prioritize managers with deep expertise and broad resources that can generate value without relying on public market tailwinds. For their part, managers need to be disciplined, making sure that they maintain a balance between deal flow and the capital they are able to raise. While a range of private markets strategies may be appropriate, we believe that investors should consider seeking exposure to strategies that address liquidity challenges as private market firms work off their inventory over time.

Current opportunities: Leaning into liquidity

- Buyout: Dealmaking has increased, auguring a slow thawing of the private equity market. Investments tied to the AI boom could play a key part in this revival.

- Secondaries: Quality, seasoned assets remain ‘on sale’ as current investors seek to generate liquidity.

- Co-invest: Limited partners invest alongside general partners in midlife portfolio assets with reduced ‘blind pool’ risk.

- Capital Solutions: Flexible capital, typically in the form of preferred equity, convertible preferred equity or similar hybrid capital, allows current private equity owners to fund strategic plans or return capital to investors.

- Private Credit: While competition has increased and spreads have tightened, carefully selected quality transactions can offer favorable yield and return prospects relative to more traditional fixed income markets.

- Evergreen Funds: Investors benefit from diversification, transparency, capital efficiency and typically lower investment minimums while gaining exposure to institutional-quality investments across the above asset classes.

1 Source: Pitchbook, as of October 31, 2025.

2 Source: Neuberger, “Tariffs Are Here: What Does That Mean for Private Equity?”, February 2025.

3 Source: Pitchbook, as of October 31, 2025.

Anthony Tutrone is Global Head of NB Alternatives, and Chris Bokosky is a Private Markets Strategist at Neuberger Berman, a sponsor of Firstlinks. This material is provided for general informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. You should consult your accountant, tax adviser and/or attorney for advice concerning your own circumstances.

For more articles and papers from Neuberger Berman, click here.