Australian equities rose marginally during the September quarter with the S&P/ASX 200 Accumulation Index up 0.7%. The performance for the 12 months to 30 September 2017 was a solid 9.2% driven by a good performance from large caps and strong gains in the resources sector with the S&P/ASX 200 Materials Index up 17.3% for the 12 months.

International LICs performing best

However, the best performing LICs for the 12 months to 30 September 2017 were those with an international focus reflecting the strong performance of international equity markets, with the MSCI World Index (Local) up 17.9% for this period. The top four performing LICs were PM Capital Global Opportunities Fund (ASX:PGF) up 30.4%, MFF Capital Investments (ASX:MFF) up 22.5%, PM Capital Asian Opportunities Fund (ASX:PAF) up 22.2% and Platinum Capital (ASX:PMC) up 20.7%. (IIR does not cover these four LICs and we make no recommendations in relation to these LICs.) The strong performance of these LICs over the past year, which significantly beat the returns of the Australian market, highlights the benefits to investors of a diversified portfolio with a proportion in international equities.

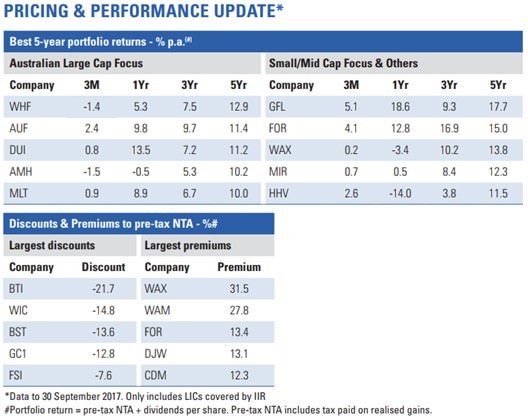

The best performing LIC in our coverage universe was also an international focused LIC, Global Masters Fund (ASX:GFL). GFL invests in quality international shares, but its largest exposure is to Berkshire Hathaway, at 73.8% of its portfolio. Berkshire Hathaway shares rose around 30% for the 12 months to 30 September 2017 helping drive GFL’s 18.6% growth in pre-tax NTA. The reason the pre-tax NTA growth did not match the growth in the Berkshire Hathaway share price was that GFL’s investment in Flagship Investments (ASX:FSI) achieved limited share price growth and the Australian dollar rose over the same period. GFL was also the best performing LIC in our universe over a five-year period delivering a pre-tax NTA return of 17.7% p.a., again, reflecting the strong performance of Berkshire Hathaway shares over the period. GFL has also delivered strong share price returns of 52.9% over 12 months and 28.7% p.a. over five years reflecting elimination in the discount to pre-tax NTA. Our rating for GFL is Recommended Plus, however, the shares now look expensive trading at roughly a 10% premium to pre-tax NTA.

Emerging Markets Masters Fund (ASX:EMF) also delivered a strong 12 month performance with a portfolio return (pre-tax NTA plus distributions) of 13.2%, although this was below the MSCI Emerging Markets Index, AUD return of 17.5%. This reflects EMF’s bias to sectors leveraged to what it believes are growth sectors such as consumer staples and healthcare. These sectors have not performed as well as 'value' sectors of the market over the past year. Over the past three years, this LIT has outperformed the benchmark with a return of 8.6% p.a. compared to the benchmark return of 8.1% p.a. EMF provides domestic investors with exposure to a professionally managed portfolio of emerging market funds, a unique proposition on the ASX. From a country perspective, the largest allocations are to China (26.9%) and India (16.9%). A significant portion (18.5%) is also invested in what the company refers to as Frontier Markets. The portfolio is significantly overweight India and the Frontier Markets relative to the benchmark. At 30 September 2017 EMF securities were trading at a 1% premium to pre-tax NTA, a reasonable entry point for long-term investors looking for emerging markets exposure. Our rating for EMF is Recommended Plus.

Cadence Capital (ASX:CDM) and Perpetual Investment Company (ASX:PIC) which both have blended portfolios of Australian and international equities also delivered returns above the domestic market return. CDM delivered a portfolio return of 10.3% and PIC delivered a portfolio return of 10.2%. Our rating for CDM is Recommended Plus and PIC is Recommended. At 30 September 2017 CDM was trading at a 12.3% premium to pre-tax NTA while PIC looked reasonable value at a 4.7% discount.

Australian large cap LICs underperform over 12 months

The five largest Australian large-cap focused LICs delivered an average portfolio return of 8.0% for the 12 months to 30 September, below the S&P/ASX 200 Accumulation Index return of 9.2%. This largely reflects underweight positions in resources, a sector which has performed well over the last 12 months. Over a five-year period these same LICs have delivered an average portfolio return of 9.1% p.a. versus the market benchmark return of 10.1% p.a.

Over the longer-term we would expect these LICs to perform broadly in line with the market. At 30 September 2017 Australian Foundation Investment Company (ASX:AFI) and Milton Corporation were trading at slight premiums to pre-tax NTA and Australian United Investment Company (ASX:AUI) was at a slight discount. All look reasonable value for long-term investors looking for exposure to a diversified portfolio of Australian large-cap shares. Our rating for AFI and MLT is Highly Recommended and our rating for AUI is Recommended Plus. Diversified United Investment (ASX:DUI) was the best performing large-cap focused LIC over the 12 months to 30 September 2017 beating the market with a portfolio return of 13.5%. Its five-year return of 11.2% p.a. also beat the market benchmark return of 10.1% p.a. At 30 September DUI was trading at a 3.3% discount to pre-tax NTA, a good entry point for investors looking for exposure to a diversified portfolio of Australian large-caps shares. We note that DUI also has a small exposure to international shares and also Australian small caps. Our rating for DUI is Recommended.

Whitefield (ASX:WHF) was the best performing Australian large-cap focused LIC on a five-year basis. Whitefield primarily invests in Australian industrial shares meaning that it does not have exposure to the volatile resources sector. Whilst WHF underperformed the industrials benchmark over the past 12 months, its five-year return of 12.9% p.a. was slightly better than the 12.7% p.a. return from the S&P/ASX 200 Industrials Accumulation Index. At a 6.8% discount to pre-tax NTA at 30 September, WHF’s shares represent good value for investors looking for exposure to Australian industrial shares. Our rating for WHF is Recommended Plus.

Peter Rae is Supervisory Analyst at Independent Investment Research. This article is general information and does not consider the circumstances of any individual.