What is good financial health? Are there a minimum number of 'big picture', timeless, universal and objective indicators of financial health that can be easily measured and monitored? What benchmarks or targets for those indicators should be met or exceeded to signify good financial health?

These were the questions we asked at my previous financial planning firm, Wealth Foundations, starting around 2010. Our aim was to provide a simple but robust, high-level framework for assessing good financial health, both for existing and potential clients.

After a number of iterations, in mid-2012 we finally settled on five indicators and, subsequently, saw no need for any further change.

Having now retired as a financial planner, and with the consent of Wealth Foundations, the purpose of this article is to introduce this personal financial health framework to a wider audience.

The hope is that it will provide anyone who is willing to do a little homework with a sound basis for understanding the current state of their financial health and the direction they need to head to improve it.

What is good financial health?

First, “What is good financial health?”. We equate good financial health with financial independence. Financial independence is having sufficient accumulated investment wealth to support your desired lifestyle, indefinitely, without the need to work.

Of course, you can choose whether and how much you want to continue to work but you don’t need to earn exertion income. So, financial independence isn’t necessarily retirement.

Five key indicators of good financial health

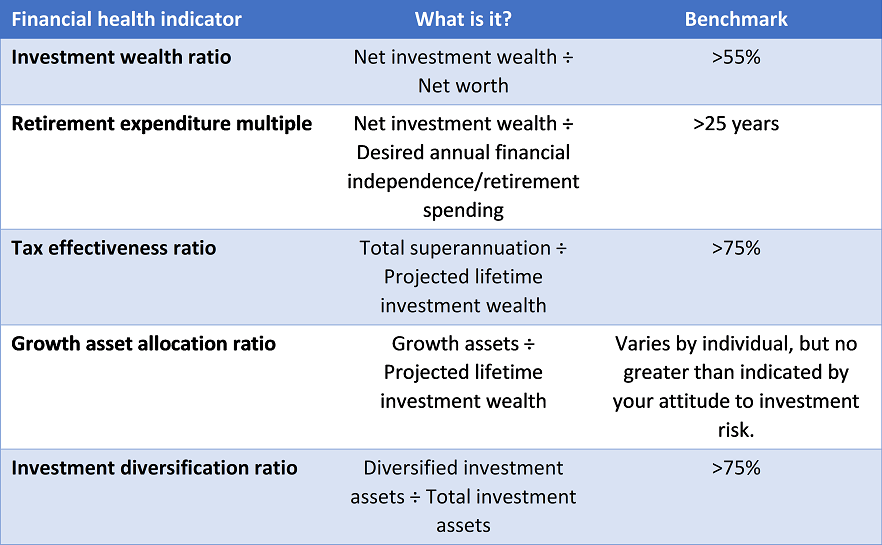

The first indicator is the Investment wealth ratio, defined as your net investment wealth (i.e. investment wealth less debts), divided by your net worth. It’s examining the question “Is too much of your wealth allocated to lifestyle assets?”.

For good financial health, the benchmark for this indicator is set at a minimum of 55% i.e. at least 55% of net worth needs to be held as net investment wealth and no more than 45% as lifestyle assets (e.g. own residence, holiday home, cars, boats etc.).

The benchmark was chosen based on experience with Sydney-based, high net worth/high income financial planning clients and is, admittedly, a little arbitrary. But its rationale is to highlight that if too much of your wealth is tied up in lifestyle assets, financial independence may be elusive.

The second indicator is called the Retirement expenditure multiple. It’s calculated as your net investment wealth divided by your desired annual retirement (or financial independence) spending. It’s looking directly at the issue of “Will you run out of money?”.

The financial independence benchmark for this indicator is a requirement for net investment wealth that is at least 25 years of desired annual retirement spending. It’s the equivalent of the often criticised '4% safe withdrawal rate'.

For those who argue that the benchmark should be more than 25, the reality is that most Australians fall so far short of it that pushing for a higher number is largely academic. And, for those who argue it’s overly conservative, my retort is that you better not plan on living to age 100.

Regardless, the Retirement expenditure multiple benchmark, like all the benchmarks, is a 'rule of thumb', rather than a hard and fast dictate. The benchmarks provide meaningful targets that those who desire to be financially independent can compare their circumstances with.

The third indicator is the Tax effectiveness ratio. It’s your total superannuation holdings divided by your Projected lifetime investment wealth. Projected lifetime investment wealth is your current net investment wealth plus an estimate of the amount you expect to save between now and the date of your desired age of financial independence or retirement.

The Tax effectiveness ratio is a proxy measure to answer the question “Are your investments held tax effectively?”. The benchmark for this measure is at least 75%. Its basis is that since superannuation is currently a very tax effective environment in Australia and it’s where most people should hold the majority of their investment wealth.

Again, it’s a rule of thumb rather than a dictate. There will often be legitimate reasons why the benchmark won’t or can’t be achieved, without jeopardising the goal of financial independence.

The fourth indicator is the Growth asset allocation ratio. It’s your growth investment assets (i.e. shares, direct property, share and property managed funds/ETFs) as a percentage of Projected lifetime investment wealth, discussed above.

The focus here is “How much investment risk are you comfortable with?”. The target or benchmark will differ for each investor. “The target asset allocation decision” discusses this choice in more detail.

However, for most, we advocate that your maximum risky growth asset exposure when financially independent and/or retired shouldn’t exceed a level that would cause you to lose sleep, due to anxiety, and, perhaps, abandon a sound investment strategy in troubled markets. This is generally guided by an assessment of your attitude to investment risk.

The final indicator is the Investment diversification ratio. It’s calculated as your diversified investment assets (i.e. your total investment assets less, primarily, concentrated holdings such as investment properties and large individual share holdings) divided by your total investment assets.

The issue this indicator addresses is “Have you too many investment eggs in one basket?”. Investment theory suggests that concentrated investment holdings offer no expected return premium for their additional investment risk compared with the relevant, well diversified, asset class. Consequently, they aren’t regarded as consistent with good financial health.

While our benchmark for the Investment diversification ratio is a minimum of 75%, our view is that you should diversify your investment holdings as broadly as you cost effectively can.

Summarising a universal framework to assess your financial health

The table below summarises the five financial health indicators discussed above and their recommended benchmarks.

Good financial health is revealed by being at or above each of the indicator benchmarks. You’ll notice that it’s not directly dependent on how high your income is or how much you’re worth.

While shortfalls on some benchmarks may not be a major problem, the framework encourages you to address the reasons for any divergences.

And, of course, should you fall well short on a number of the benchmarks, the direction of the changes you need to make to improve your financial health, in terms of the framework, should be apparent.

So, how’s your financial health?

John Leske is Founder and CEO of finhealth, the provider of an approach to assessing the state of your personal financial health. The article describes a general framework to compare your current situation with some meaningful financial benchmarks. No specific personal financial advice is provided and it is up to readers to determine what actions, if any, they take in response to the article. A more detailed explanation of the indicators can be found in the free eBook, “What is finhealth?”.