How to turn a 10-day expedition to Antarctica with 120 other passenger into an investing and superannuation story? Simple. Look around the dining room on the first night and chat to a few people, and you soon realise how many retirees are ticking off their bucket list. And it’s quite a list, with the next trip and the one after that already planned.

For those who can afford it, this is what saving, investing and superannuation are intended for. It’s not simply being ‘comfortable’. ASFA’s Comfortable Retirement Standard for a couple is $61,500 a year, and Antarctica is an expensive trip. Many passengers have worked hard all their lives, and they are enjoying their freedom while they are healthy enough.

The warm kayak, or making the most of a life of work

Let’s start in South America, at the bottom of Argentina in Tierra del Fuego province, which translates to ‘Land of Fires’. The major city is Ushuaia (see map at end), and it’s close to the Southern Ocean and the departure point for many boats heading for Antarctica. The name derives from a time when natives lined their canoes with clay and lit fires to warm themselves on fishing trips. While this immediately prompted the ‘you can have your kayak and heat it too’ thought, it’s also a good summary of the aim of ‘retirement’.

During the 10 days, it was apparent how much money and willingness to spend it was in that room. Lots of affectionate chat about grandchildren (try to look interested) but handing them back to their parents and going away is as good.

Businesses and marketers, including in wealth management, who focus on younger generations are missing an opportunity. Generally, these people were not born into money and would not consider themselves ‘wealthy’ but have accumulated assets over 40 years of work. They now carry expensive cameras with zoom lenses, dress in the latest outdoor gear, wear cool sunglasses and carry the latest mobile tech. They may be into their seventh or eighth decade, but there’s no asking the kids how the internet works or how to copy photographs to a USB. Other equipment such as walking sticks and hearing aids are common, but there’s surprisingly little complaining about aches and pains and health.

We previously published this article on marketing:

“Australians over the age of 50 have the highest levels of wealth and disposable income of any age segment, they outspend millennials in entertainment, auto, health, travel and almost every other category, but are largely ignored by brands.”

The Bank of Mum and Dad

Another popular topic was how difficult it has become for their children (now adults aged in their 30s and 40s) to buy their first home. Even when the Bank of Mum and Dad comes to the rescue, there are at least three models on the best way to do it for those who have sufficient resources.

(Most older people do not have the luxury of helping their children in these ways, but it’s a goal to aspire to when planning for retirement a few decades in advance).

- Give a gift as a contribution to a better property

Residential real estate in most Australian capital cities (what’s wrong with Darwin?) has become so expensive that gifting half a million to help buy a $1.5 million property still leaves the child to find a significant $1 million. For those who think it is ‘spoiling them’ and ‘they should make their own way in life’, consider if it is better to wait until they are 60 when they will inherit the estate anyway. Why not give some of the money early and make a better life for both children and grandchildren when they need it most?

- Provide a loan backed by an unregistered mortgage

A couple who had worked hard in a successful business wanted to help each of their three children equally but were worried that their marriages may not last and any gift would then be shared with the son- or daughter-in-law in a settlement. So they lent the money with a unregistered mortgage, which would give them a claim on the debt in a change in circumstance. They had no intention of invoking the mortgage terms, but it was a safety net. Consult with a financial adviser for this strategy.

- Become joint owners of the property

Another person had gone 50/50 with his son as joint owners. This enabled the child to make a start in a better quality of house, without the feeling of a handout, which the son strongly resisted. Instead of paying rent to his parents, they agreed he would be responsible for all outgoings including council and water rates and renovation costs. The parents have an investment with capital gain potential (which in reality is only about 2% after expenses on a normal residential investment property).

For anyone who can afford it, these methods allow the Bank of Mum and Dad to function while addressing some of the emotional, financial and future risk problems that might arise. Seek financial advice before taking any of these big steps.

Some ways to have your cake and eat it too

Let’s acknowledge not everyone can plan to spend far more in retirement than in their younger years. The 2015 Intergenerational Report says most people will continue to rely to some extent on a part age pension in retirement.

The starting point to affording trips like Antarctica is setting a goal early in life, often with the aid of an adviser who will have the tools available to show how much needs to be saved, in which investment vehicles over what period.

Assuming some level of spare spending capacity, how can a retiree travel the world when they have spent most of their lives paying off the mortgage? They may have accumulated a decent superannuation balance and a house but little extra spare cash.

Far be it for me to encourage profligate spending when running out of money is a major worry for many retirees. However, anyone who lives a parsimonious retirement, denying themselves a few luxuries and then leaving millions of dollars to their kids seems to have the wrong priorities. Yes, the house might be needed to fund the nursing home, but the deposit usually goes back to the children on death. Do your numbers and live a little, such as:

- The Pension Loan Scheme (PLS) can be accessed by eligible people over the age of 65 who own their own home. The PLS ensures some restraint by not allowing lump sum borrowing but gives a cash flow equal to 150% of the age pension, creating a debt against the future value of the home after death. See previous articles here and here for more details.

- The age pension ’retirement gap’ attracts a lot of attention, such as in this article which describes how much pension is lost due to holding assets above a set level:

“On the assets side, for individual homeowners whose assessable assets are above $263,250, the pension is reduced by three dollars a fortnight (or $78 per year) for every additional $1,000 in assets. To offset this reduction, each $1,000, if invested, must generate an annual return above 7.8%.”

There are obvious risks in spending money (on non-assessible assets such as the family home or expenses such as travel) to qualify for a larger pension. I don’t like this strategy for the reasons outlined here but some financial advisers encourage their clients to spend money on themselves for this reason. There’s also a possibility that the rules might change.

- Downsizing a property can release capital and allow up to $300,000 per person to be added to superannuation for people aged over 65.

Back to the trip itself

We heard that the tempestuous Drake Passage crossing between South America and Antarctica could literally be hell at the bottom of the earth, and three days there and three back in violent seas was a major barrier.

But with our fly/fly trip, we flew to and from Punta Arenas in Chile into a military airfield on King George Island in the South Shetlands near the Antarctic Peninsula, where zodiacs whisked us onto the waiting ship and the warmth of hot chocolates and spacious cabins. No Drake Passage ship crossing in our case.

Source: Aurora Expeditions

This is the type of trip that many of the passengers had worked and saved for, and SKI holidays which ‘spend the kids’ inheritance’ are real.

The size of the ship is a vital part of the enjoyment. There are dozens of interesting places to visit in Antarctica, from isolated scientific research bases to penguin colonies, to close-up whale and seal watching and stepping onto ice floes. However, the maximum number allowed at any landing site is 100, and some sites permit only 35 people at historic locations.

A ship with 120 passengers, with a couple of dozen who take off elsewhere on kayaks and snorkelling trips, is ideal because everyone can go ashore at the same time. It allows two activities a day, and these visits are the highlights. It’s extraordinary to run around while floating on sea ice on the Weddle Sea, with massive icebergs drifting past. Not as amusing is a penguin pecking at your legs when you’re not supposed to move.

A ship with 500 passengers, and certainly one with thousands, would require passengers to remain onboard and this would compromise the experience. It must be an expedition, not a cruise. A ship with large numbers of passengers might mean they rarely disembark, with glaciers and wildlife spotted in the distance.

Having your cake

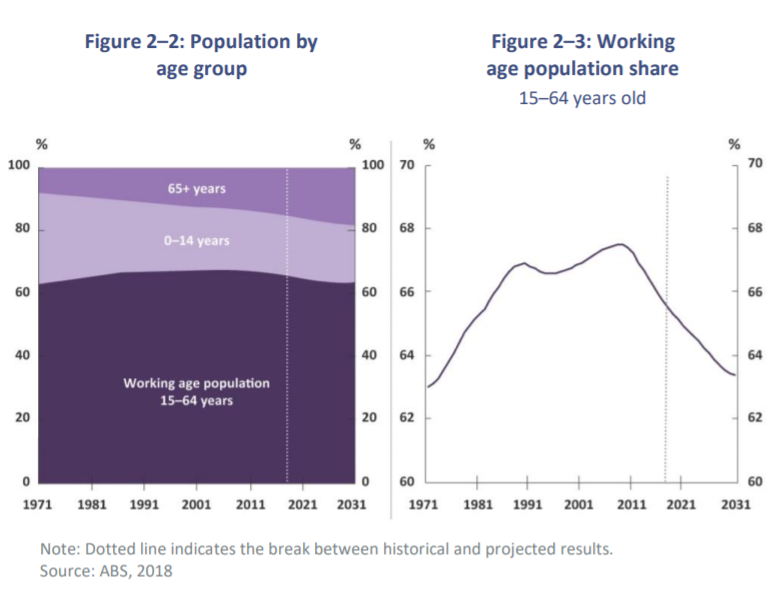

The chart below, provided by the Parliamentary Budget Office in February 2019, from a report called ‘Australia’s Ageing Population’, shows the proportion of the Australian population aged over 65 is set to double between 1971 and 2031.

In 2020, these people are not like their parents at the same age. It’s a growing, multi-billion dollar market of retirees living the good life, for travel, outdoor gear, cameras, hearing aids, expeditions, retirement savings, mobile tech, health services, airlines, real estate … the list is endless, long before nursing homes kick in.

What are you waiting for? Start your plans now, if not for Antarctica, then for something you have always wanted to do. Tell your adviser about your goals.

Comments welcome on how you have done it, or why you haven’t.

Graham Hand is Managing Editor of Firstlinks.