Australia is in a housing quagmire. Each aimless and counterproductive lurch finds us mired deeper in a morass.

In my eleven years in Australia I’ve seen multiple attempts at increasing affordability. None of these affordability measures are designed to lower housing prices. Pretending there is a way to make housing more affordable without somebody losing out is intellectually dishonest.

Politically I see the logic. No politician wants to be responsible for lower housing prices. Increasing supply by building more houses would reduce prices. Limiting demand by slowing immigration would reduce prices. Successive governments have been unwilling or unable to do either despite pledges to the contrary.

Nobel prize winning economist Richard Thaler coined the phrase libertarian paternalism to describe a system where personal autonomy is maintained but choices are guided in a direction that helps individuals and society as a whole.

I think this concept strikes an appropriate balance between personal freedom and nudging people in the right direction. If this is the yardstick to measure housing policy Canberra is falling short.

The 5% deposit scheme is a perfect example. It plays on the emotional pull of homeownership to encourage participants to put themselves in potential financial peril while simultaneously tying the hands of policy makers to respond to economic challenges.

Stimulating demand to make housing ‘more affordable’

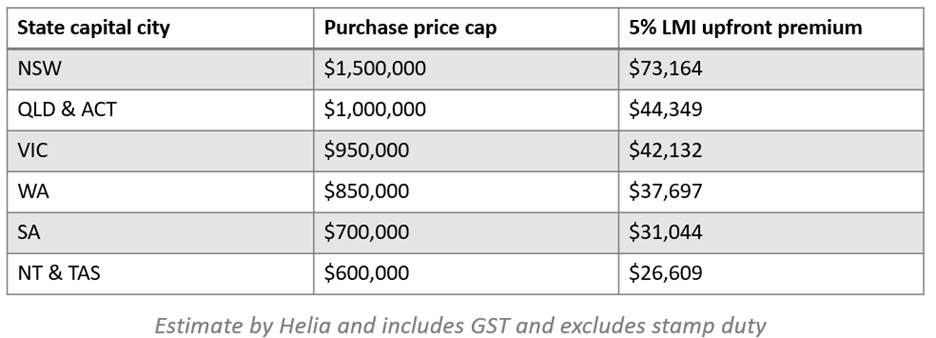

The 5% deposit scheme isn’t new but the Labor government removed income limits and increased property price caps. As a result, over 1 in 3 first-time homebuyers and 1 in 10 overall homebuyers used the scheme in 2024-2025.

As part of the program the government takes on the liability that would normally be covered by lender mortgage insurance (“LMI”). This is not an insignificant amount of liability and LMI costs reflect the risk of higher defaults given smaller deposits.

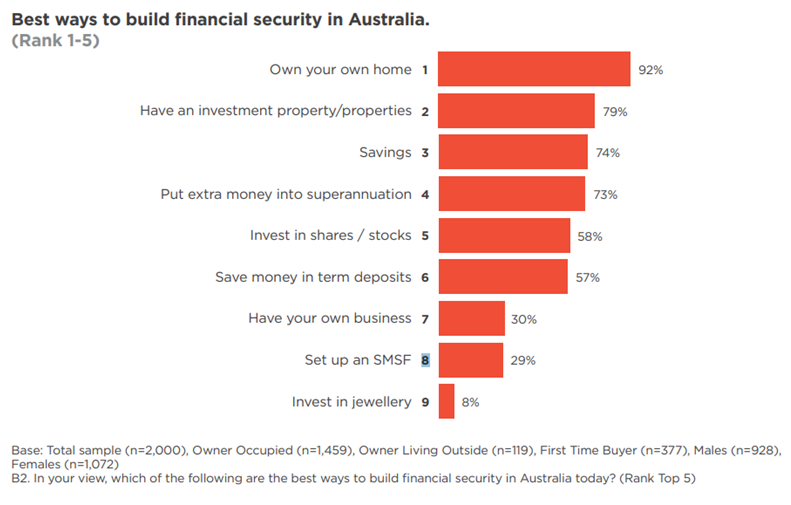

There are many reasons people want to own a home and most aren’t financial. However, the near universal view that housing is the best way to build wealth is playing a role.

In a Westpac survey Australians were asked to rank nine different financial strategies to build wealth. Owning your home came in at number one with 92% of respondents selecting the option. Number two was buying an investment property.

This view has been shaped by watching proceeding generations ‘get rich’ by simply owning a home. Many of the people that have reaped these outsized gains never saw housing as an avenue to accumulate this degree of wealth.

What has happened historically is unlikely to be repeated. It is improbable that historic price appreciation can continue given current property prices. To purchase with a 5% deposit results in higher interest expenses and slower accumulation of equity.

We are doubling down on housing when few experts would argue it is ideal to have 70% of Australian wealth (according to AMP) tied up in an illiquid asset which does little to improve the day-to-day life of the owners or country. Yet this is where we find ourselves.

The folly of the 5% deposit scheme

Problem one: Heavily indebted individuals have lower economic resiliency

One implication of the 5% deposit is the obvious one – bigger loans. According to Finder, the average loan amount for a first-time homebuyer reached $607,624 in December 2025. That is a 24.60% increase in one year which far outstrips property price gains of approximately 10% nationally. Loan growth outstripping price growth is a symptom of a scheme where 5% deposits can be used on houses costing up to $1.5 million in certain parts of the county.

This trend of growing mortgage debt is not new. When I moved to Australia in 2015 the average loan amount for a first-time homebuyer was $333,500. In a little over a decade the loan amount has increased by over 82% while median wages are up 54%.

Servicing these larger loans has not gotten easier. 2015 is an arbitrary point in time but that year the RBA cut the cash rate to 2% on the way to a low of 1.50% in 2016 where it remained through 2019. In 2020 the cash rate was down to 0.10%.

Larger loans and higher rates are putting more Australians in financial distress. According to Roy Morgan 24.50% of owner-occupied mortgage holders are experiencing stress which refers to households spending 30% or more of pre-tax income on a mortgage.

More Australians are vulnerable to any type of economic disruption. This includes job loss, stagnant wage growth, inconsistent earnings, unexpected bills or interest rate increases.

Some assume this problem will solve itself as young homeowners advance in their careers and get pay increases. This was the pattern in previous generations. But the profile of first-time buyers has changed.

Data from Westpac shows the average age of new homeowners is 34 years old with some brokers indicating it is closer to 37. The Westpac data shows one in five first-time homeowners are over 40.

Carrying mortgages later in life while dedicating a larger percentage of income to service a higher amount of debt is not a formula for financial security.

Problem two: Less policy flexibility

There has been ample coverage of Trump’s attack on the independence of the Federal Reserve. But we’ve seen similar – if less dramatic – disagreements in Australia about central bank policies.

The Greens proposal for government intervention to lower interest rates and the largely performative debates over the role of government spending on inflation distract from our economic catch-22.

The heavy debt levels of mortgage holders mean interest rate increases crush household spending and push more homeowners into mortgage stress. The alternative of continued high inflation might not get as much attention but the impact on household finances is similar. With higher inflation the pain is spread to everyone in the economy including vulnerable non-homeowners.

This is creating a no-win situation for policy makers. Larger mortgages increase the costs of interest rate hikes. The higher the cost of interest rate hikes the more calls there will be to curtail RBA independence. That likely means higher inflation.

Problem three: The economy is more vulnerable to declines in housing prices

One way to address affordability is to for housing prices to go down. This is exactly what happened in New Zealand.

Between 2021 and 2025 inflation adjusted housing values fell by 31% due to a combination of aggressive interest rate hikes, an increase in housing supply, new rules targeting investors and a meaningful drop in immigration. This has been economically painful as the Kiwi economy contracted in three of the last five quarters.

Many homeowners in New Zealand who bought in the late stages of the post-Covid surge in property prices have negative equity. Many Australians would find themselves in the same situation with the small buffer of a 5% deposit.

Given that mortgages have recourse in Australia this likely wouldn’t trigger the spiraling defaults in the US during the global financial crisis. If defaults do increase the government is on the hook for the portion of the loans covered by the LMI.

Just because people keep paying their mortgage to prevent the bank from seizing their other assets doesn’t mean there isn’t an impact.

Homeowners with negative equity likely wouldn’t be able sell or refinance. This removes one way to mitigate interest rate increases and the lack of mobility can have knock-on economic impacts. Having negative equity has a psychological effect on homeowners and would likely reduce consumption.

This once again puts policy makers in a difficult position. The same policies that led to the drop in New Zealand housing prices are being debated in Australia including in the comments section of Firstlinks.

If these policies are enacted the economic impact of a slump in housing would likely be exacerbated as more people have small equity buffers.

Final thoughts

St Augustine said, ‘Lord give me chastity and continence…but not yet.’ This paradoxical prayer sums up our housing policy. Everybody admits there is a problem but we keep kicking the can down the street.

I understand the psychological lure of homeownership. The sense of stability, the desire to have a place to call one’s own and the signaling mechanism of reaching that milestone are all powerful forces. I feel for the Australians who can’t buy a home.

But that doesn’t mean the 5% deposit scheme is the answer. It is contributing to the deteriorating financial situation of Australians. It is making the country more vulnerable to economic shocks. It is placing a meaningful liability on the taxpayer books.

Far from helping, the 5% deposit scheme is making things worse.

Mark Lamonica, CFA, is Director of Personal Finance at Morningstar Australia.