The theme of International Women’s Day was “give to gain”. If you are still thinking about giving a donation or volunteering I have a suggestion. Consider giving yourself, your daughters or your mother financial advice to gain economic security. Because you probably know these stats: women tend to score lower on financial literacy tests, end up with lower superannuation balances and find themselves in a more precarious financial situation in retirement than men. So, can advice help? Let’s take a look.

Advised members report higher levels of financial knowledge

The gender gap in financial literacy levels is stark. Only 48% of Australian women are considered financially literate compared to 63% of men[1]. Our education system has got work to do, particularly when you consider financial literacy levels are lowest amongst our younger people – those aged 15 to 24. Advice can help.

In a recent UniSuper study[2], we found our advised members reported higher levels of financial knowledge compared to our unadvised members. But remember that advice isn’t just a meeting with an adviser, it can be self-served too. Many super funds provide online education, including webinars on different topics. Some funds also offer free digital advice, or one-on-one advice on topics such as the investment option you’ve selected in super and whether it’s right for you. International Women’s Day is your moment – whether it’s reading a quick article or meeting with an adviser. It can make a big difference to both your financial knowledge, but more importantly your super balance. Involve your daughters – the power of compounding means good decisions made early will have a big impact on their super balance for retirement.

Advice can narrow the super balance gender gap

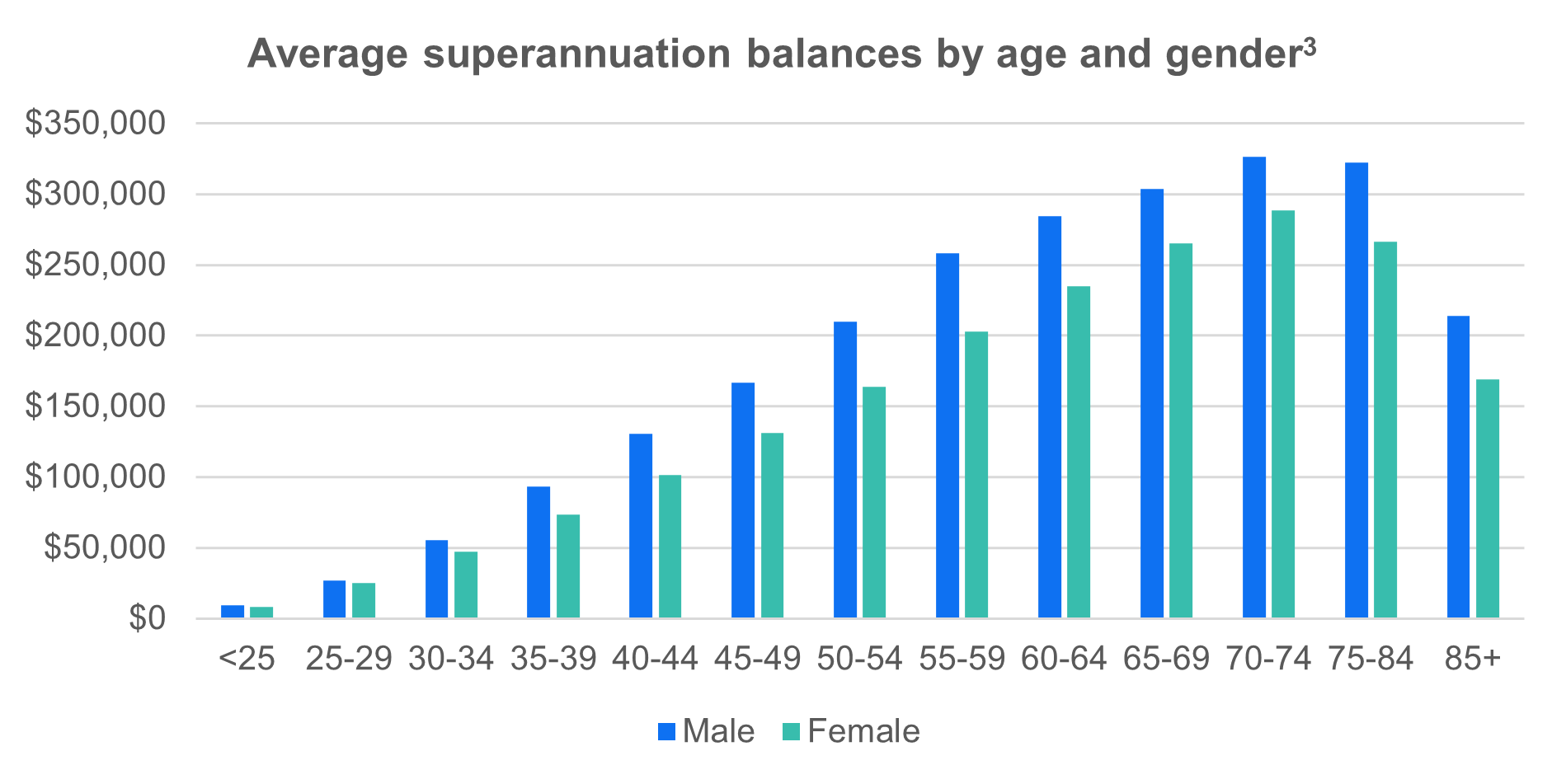

And that’s important because we still lag men when it comes to our super balances. In fact, on average, women in their mid-50s have a super balance that’s $55,000 lower than the average man at the same age.[3] It’s a time when the compound lifetime effects of carer responsibilities and often lower paid work show up.

Advice can help close this gap too. Not only through the options outlined above, but through personalised strategies for women taking time out of the workforce for carer responsibilities. For example, your spouse can make an after-tax contribution to your super while you’re out of the workforce, or split their before-tax contributions into your superannuation account instead of theirs. Give yourself the gift of advice to help equalise super balances!

Advice can improve living standards in retirement

Finally, women generally retire in a more precarious financial situation than men, often for a few reasons. On average, women retire 2.4 years earlier than men; are 2.5 times more likely to face primary caregiving demands between ages 45 and 65 (after having cared for children); and often as a result retire with lower super balances. We then of course typically live longer than men. Any one of these factors impact the financial situation you find yourself in retirement. Financial advice can help. Our study showed that advised members tend to take more tangible actions towards securing their future. A few, simple decisions can make a difference to your standard of living in retirement.

What will you “give to gain” for International Women’s Day?

Gaining financial security is one of the most important gifts you can give yourself and others. Improved financial literacy, a healthier super balance and a higher standard of living in retirement is important for everyone. Advice does help. Our advised members feel more financially confident and more prepared for retirement. Use this year’s International Women’s Day as your moment to “give yourself financial advice to gain” economic security. You’re worth it.

[1] 2020 Household, Income and Labour Dynamics in Australia (HILDA) survey

[2] 2025 CoreData Research, Best Possible Retirement – UniSuper Report

[3] APRA Quarterly Superannuation Industry Publication - Sep 2025

Annika Bradley is Head of Advice Strategy, Research & Technical at UniSuper, a sponsor of Firstlinks. She brings over 20 years of experience across investments and wealth management in both the public and private sectors. In previous roles Annika worked with Morningstar and QSuper. The information in this article is of a general nature and may include general advice. It doesn’t take into account your personal financial situation, needs or objectives. Before making any investment decision, you should consider your circumstances, the PDS and TMD relevant to you, and whether to consult a qualified financial adviser. Issued by UniSuper Limited ABN 54 006 027 121 the trustee of the fund UniSuper ABN 91 385 943 850.

For more articles and papers from UniSuper, click here.