While economists increasingly identify public spending as a major driver of inflation in Australia, the impact of energy policy and the renewables transition is a significant yet under analysed source of inflation.

The cost of energy flows through to the cost structure of the whole economy. Elevated energy costs inflate unit labour costs and weigh on productivity growth. This causes supply constraints to be reached sooner with relatively modest economic growth, which lowers the economy’s inflation tolerance. Government spending compounds the problem, sustaining demand close to those constraints, making disinflation more difficult and requiring interest rates to remain higher for longer.

Energy is central to the productivity-inflation equation

Reliability is core to any electricity system, and in order to maintain it when a growing share of energy generation is intermittent, there are two broad paths that can be taken.

One is ’substitution’, where intermittent generation, together with dedicated firming, replaces firm generation one-for-one. The other is ‘duplication’[1], where some existing firm generation must remain for reliability, with intermittent generation layered on top.

And the crux of the problem in Australia is not that we are in an energy transition phase, but that firm capacity in coal is exiting without adequate replacement. Duplication occurs to compensate.

Further planned exits are delayed, gas backup is added, transmission networks expand, storage is added through short-duration batteries, the grid requires stabilisation[2], and demand response may be required in periods of high energy demand. Clearly this is not substitution, it is stretching the system. Layers are added, much of which only runs some of the time and is therefore unproductive and costly. More capital is required to meet the same energy demands.

Electricity prices must therefore rise under a path of duplication, to reflect higher total system costs. And when energy is more expensive, business invests less in technology, and research and development, meaning fewer efficiency gains, rising unit labour costs, and slower productivity growth.

Like persistent public sector spending, duplication crowds out private sector activity by absorbing scarce capital and capability. It not only saps productivity within the energy system, but lowers productivity and inflation tolerance across the entire economy.

A ‘substitution’ path on the other hand, swaps out exiting firm capacity in coal, for combined renewables plus dedicated firm replacement such as nuclear, hydro, or gas. The key is that capacity is replaced and not accumulated. Replacement is orderly and well sequenced such that reliability is in place before the original generator exits. Temporary duplication will be necessary until full replacement is operational, unlike a duplication path where supplementary infrastructure comes into the system permanently, with the original firming never fully replaced.

Even under a substitution pathway, the addition of renewables requires investment in transmission and grid stabilisation, but these costs are bounded by bringing firm capacity into the system. Whereas under duplication, over-building is usually required to fill the firming void such that costs can be limitless. Substitution replaces capacity, while duplication accumulates it.

The path Australia is on is not an explicit choice. While pursuing a renewables-only agenda with backup and storage, we also seek to shut down coal as soon as possible, exclude nuclear energy, and constrain domestic gas supply. Such barriers make duplication unavoidable.

Coal is exiting primarily because it is targeted politically and ideologically. It is also ageing and virtually uninvestable under current frameworks and policies. Shutting down plants early scraps productive capital that is largely depreciated, to be replaced with new capital that must earn a full rate of return and still requires backup and firming. Meanwhile, coal-fired power is efficient and reliable, with low marginal operating costs.

Excluding nuclear energy from the mix matters significantly because it substitutes coal directly. It is ‘firm’, meaning it is guaranteed to be available to the grid 24/7, and it has a high-capacity factor of up around 90% (ratio of actual energy output to maximum potential output). It would greatly reduce system duplication. Australia’s objection to nuclear removes a long-term substitution option and effectively locks in long-term system layering.

Finally, gas could be the saviour. It is able to be built quickly (comparatively), is highly scalable (can be expanded with less constraints), can complement renewables effectively by being able to be ramped up or down rapidly, and would lower capital duplication. But restricting it domestically means we end up exporting gas cheaply and importing it expensively, which raises costs and electricity prices. And that’s very unproductive.

These barriers explain why duplication is not shrinking in Australia, but instead, is becoming permanent. It is a system laden with defensive investment to underpin weather-dependent energy, instead of productive investment that lowers the cost of delivering firm energy.

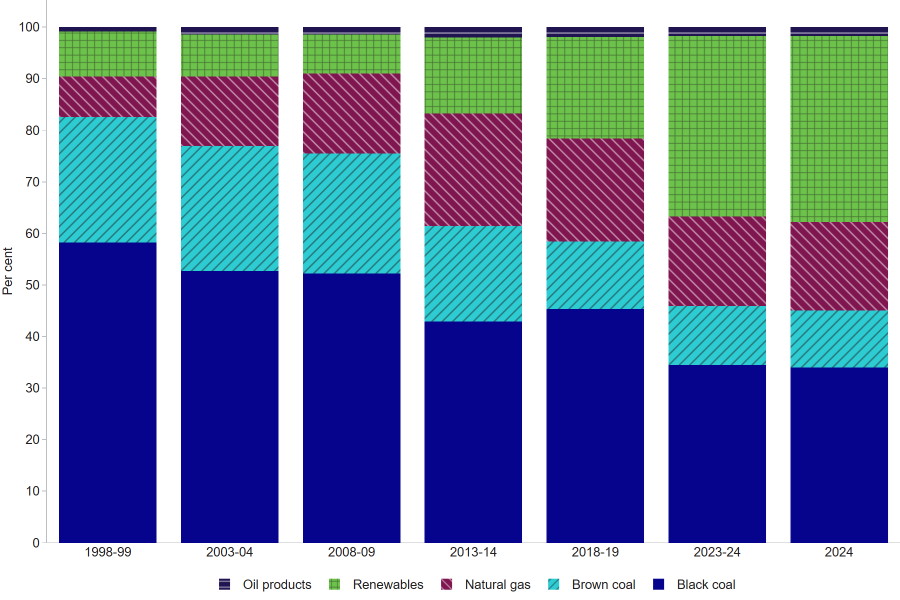

Figure 1: Australian electricity generation fuel mix

Source: Department of Climate Change, Energy, the Environment and Water (DCCEEW) (2025) Australian Energy Statistics, Table O

In the end, consumers buy firm, reliable, deliverable electricity, not generated electricity. They pay for the system that makes that energy useable. While renewable energy generation may be cheap, total system costs keep prices elevated. Which is why the “renewables are cheap” mantra is misleading.

If structural inflation is to be avoided in Australia, energy policy must target productivity and not just emissions reduction. Success should not be measured in terms of emissions reduced or megawatts installed. Rather, the focus should be on reliability per unit of capital, cost per unit of energy, and energy efficiency, because these are the measures that will define productivity, and ultimately inflation.

[1] In a previous article, I referred to ‘energy addition’ as new capacity required to meet higher energy demand, such as that arising from AI data centres, electrification, and population growth. Not to be confused with ‘energy duplication’, which as described here refers to the extra system layers required to maintain reliability as intermittent energy sources replace firm supply. The two go hand in hand in meeting energy demand, but where ‘addition’ is about the quantity of energy, ‘duplication’ is about the quality and reliability of energy.

[2] Stabilising the grid is a layer that is often overlooked. Our electricity system is an alternating current (AC) network operating at 50 Hz, historically stabilised naturally by coal, gas, and hydro generators. That inherent system stability is progressively lost with an increasing share of renewables generation, requiring conversion and synchronisation, which adds complexity and cost to the system.

Tony Dillon is a freelance writer and former actuary. This article is general information and does not consider the circumstances of any investor.