The annual UBS Global Investment Returns Yearbook offers an opportunity to take a step back from the daily news cycle and reflect on drivers of returns over the long-term. This is always a valuable exercise for investors.

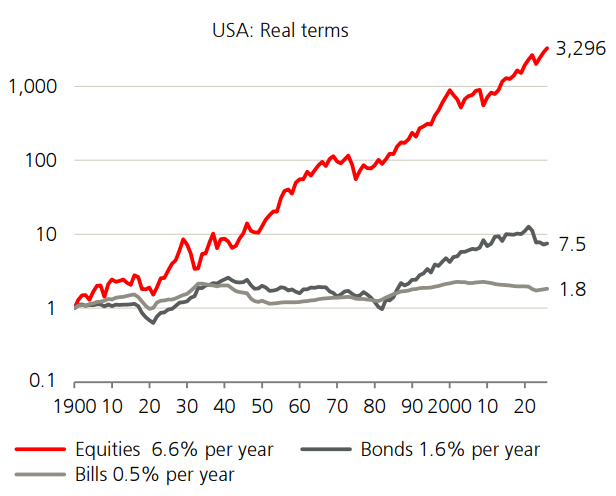

Beating inflation over the long-term

In times of geo-political tensions, it can be easy to move to ‘safer’ investments. The perception of safety is largely illusionary. Shares continue to crush the returns of other asset classes over the long-run on a nominal and inflation adjusted basis.

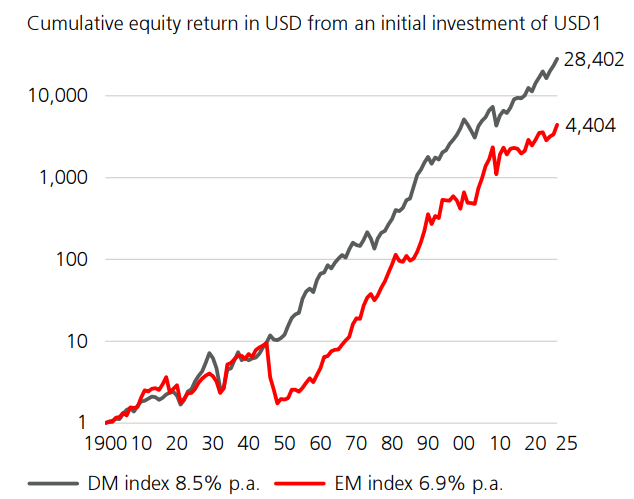

Emerging markets aren’t all they are cracked up to be

Periodically the emerging market bulls will rear their heads. Now is one of those times. Huge untapped markets, fast economic growth and the promise that this time will be different make up the standard sales pitch. To date this pitch hasn’t delivered over the long-term.

The changing face of markets

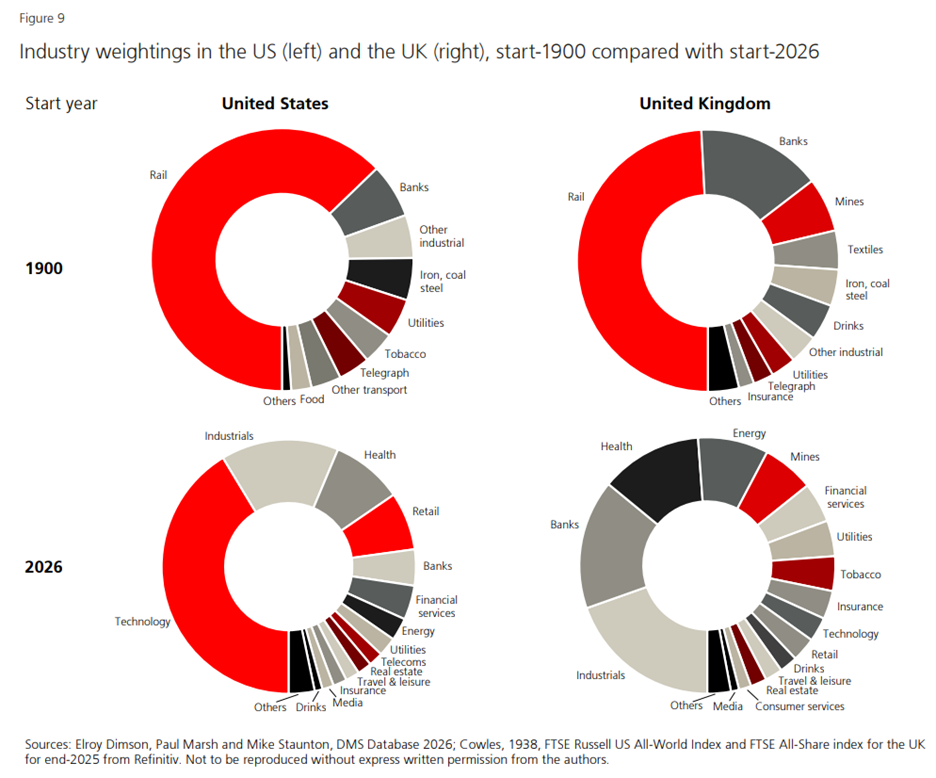

The growing influence of the technology sector on US markets is widely discussed. The technology concentration of today pales in comparison to the dominance of railroad shares at the turn of the 20th century.

Interestingly, the UBS report points out that despite railroad shares dropping from 63% of the US market in 1990 to less than 1% today they outperformed the overall market. Declining industries can still offer strong returns.

Zooming out is easy to say and hard to do. The UBS Global Investment Returns Yearbook is a reminder of what works over the long-term.

Mark Lamonica

In this week's edition...

With the upcoming budget increasingly likely to include bold proposals to alter the tax code Mark outlines three incremental steps with fewer unintended consequences.

Two opposing views on the impact of the war against Iran. David Tuckwell from ETF shares explores the secondary inflationary impacts of higher oil prices and concludes mortgage holders should be prepared for higher rates. Ashley Owens believes the war is another ‘get out of jail free card’ for politicians.

Investors looking for income should consider global infrastructure as yields are in the upper half of their historic range. Better yet, Edmund Leung believes there is room for dividends to grow.

With new leadership taking over in Japan, Leon Rapp outlines the challenges facing the country.

One driver of gold’s run is the shift in worldwide central bank policy with an emphasis on gold reserves over US Treasuries. Francisco Barillas Bedoya looks at the impact of this trend.

Can economic development be measured in terms of social progress? Kevin Fox looks at this emerging trend.

This week's white paper from Fidelity explores four key levers that could help equity investors manage the challenges posed by geo-economic fragmentation, sustainability risks, AI, and market concentration.

Curated by Mark Lamonica and Leisa Bell

***

Weekend market update

Two articles from Morningstar this week. Are we witnessing a modern day bank run in private credit. I took a look at the situation. My colleague Tyger uncovered three opportunities after ASX earnings season.

From Shane Oliver, AMP:

Global share markets had another poor week as the Iran War continued, and the Strait of Hormuz remained effectively closed. Oil prices remained around $US100 a barrel – with West Texas down slightly but Brent up slightly. Reflecting the worries about a boost to inflation and a hit to growth, along with another RBA rate hike, Australian shares fell around another 1.9% with energy, utility and consumer staple shares up but most other sectors down. From this year’s highs US shares are down 5%, Eurozone and Japanese shares are down 9% and Australian shares are down 8%.

Gold and silver remained under pressure despite the geopolitical and inflation risks as excessive speculative positions were wound back. Bitcoin also fell. Iron ore prices rose but metal prices fell. The $A rose slightly as the $US fell and it remains relatively resilient reflecting ongoing expectations for RBA rate hikes at a time when the Fed is still expected to cut, albeit by less than before the War.

Despite the hit to global oil supplies threatening to be the biggest on record the market reaction so far has been relatively mild. Global oil prices are up “just” 70% from their January low (compared to the three or four fold increases of the 1970’s oil shocks) and US shares have only fallen 5% and are bouncing around technical support at their 200 day moving average and the Australian share market has had a fall of around 8% - both of which would count as a mild correction. So maybe the markets know something. There are several reasons for the mild reaction:

- The experience of the last year has been that a shock and awe event (Liberation Day tariffs, ICE raids in Minneapolis, attacks on the Fed, the threats around Greenland, etc) are followed by a backdown or moderation. So market still expect another TACO.

- Similarly Trump’s military adventures (Nigeria, Venezuela) have been targeted and brief.

- There is hope the hit to supply flowing from the effective closure of the Strait of Hormuz will be overcome or by-passed in various ways (naval escorts, IEA reserve releases, Iran letting some ships through, etc).

- And finally Trump is regularly using jawboning to head off a market meltdown – the War will be over “pretty soon”, the Iranian military is being “literally obliterated”, the operation is “far ahead of schedule”, oil prices will see a “sharp fall” when it’s over, etc. And this may be helping put a lid on investor fears - so far. Nixon, Carter and Bush senior never had Trump’s ability to bamboozle.

Some or all of these may be true to varying degrees. And Trump has a huge incentive to do a TACO with the War being unpopular, increasing odds he will lose the Senate as well as the House in the midterms, & increasing objections from MAGA supporters over his waging of another war. Losing the House would be normal in a midterm election for the president’s party, but losing the Senate would be a huge win for the Democrats as all four GOP Senate seats up for election are in safe Republican states.

But at this point it looks like the War has further to go and so oil prices could still go a lot higher before they start sustainably falling even if the War is relatively short. Aerial campaigns don’t have a great track record of success and reports indicate that the Iranian leadership is digging in and getting more hardened in resistance to the US. And the Pentagon has reportedly asking Congress for $US200bn to fund the War suggesting it has a way to go yet. So much for Trump’s hope (or was it a plan?) for a re-run of the Venezuelan model. This may make it hard for the US to simply declare victory in relation to some of its narrower military objectives (like wiping out the navy, missiles and nuclear capability) and then simply withdraw as Iran may still have an ability to cause havoc including with the Strait of Hormuz. And while there are various workarounds to the Strait blockage of around 20 million barrels of oil a day, or 20% of global supplies, these won’t make up for it all:

- The IEA reserve release is likely to be only around 3.3% of pre-War global oil consumption a day;

- Easing Russian sanctions could provide another 1.5%;

- Allowing ships from China, India and Pakistan to pass will provide around 7.5%;

- And maybe an extra 4% or so can go through pipelines.

But that still leaves a shortfall greater than the 5% supply hit from the second oil crisis in 1979. And the steady destruction of energy (mainly gas) infrastructure in Iran and surrounding countries means it will take longer to get supply back to normal once the War ends. And its also worth noting that past oil shocks unfolded over many months in terms of the rise in oil prices as the full impact became clearer – it was over about 4 months in 1973 and a year in 1979. So far, it’s still early days.

Our base case is that the War and oil supply shock will be relatively short. Iran will not be able to keep the Strait closed indefinitely as it continues to see its military capability degraded, the US will eventually turn to naval escorts (albeit they are problematic) and or look for some sort of off ramp as the political pressure mounts. But it could still go on for many weeks yet and so could still see oil prices rise a lot further in the interim say to $US150 as the risks of a longer War and threat to oil supplies (oil to $US200) escalate.

The key things to watch out for will be a sustained fall in missiles & drones coming from Iran, increasing numbers of ships through the Strait of Hormuz, indications Iran wants to negotiate and another sharp rise in oil prices and a 10% or more fall in US shares which will increase pressure on Trump to find a way out.

Given Australia’s vulnerability as it imports 80-90% of its oil products it should be moving to cut back on demand now to add to our stockpile. So far the supply of fuel coming to Australia has not been disrupted according to the Government but there is a high risk it will be as some of our supplying countries impose bans on exports the longer the War continues, like China has. So, just as other countries are already starting to do, we should be moving now to curtail demand in ways that are least disruptive to business – like encouraging or allowing workers who can to work from home, encouraging more reliance on public transport, encouraging people and businesses to avoid non-essential air travel and encouraging greater use of E10 fuel. The longer we leave it the greater the risk of real disruption.

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website