The new war in Iran is about to hand politicians yet another ‘get out of jail free card’ – to blame rising oil prices for inflation, diverting attention from the real causes of persistent inflation: loose fiscal policies (spending sprees financed by deficits and rising debts), loose monetary policies (low nominal and real interest rates), plus some pre-existing supply constraints.

Politicians of all flavours to this day still universally blame the 1970s inflation and stagflation on the oil shocks in 1973-74 (Yom-Kippur war/OPEC embargos) and 1979 (Iranian revolution).

They also routinely cite rising energy prices following Russia’s invasion of Ukraine in 2022 as a main cause of the post-Covid stimulus inflation.

The problem is that inflation was ALREADY high and rising well BEFORE each of these oil shocks.

Today’s charts show oil prices, annual CPI inflation rates in USA, UK and Australia before, during, and after the three ‘oil shocks’ that are universally but incorrectly blamed for inflation, plus the current situation.

Here are the facts about oil prices and inflation:

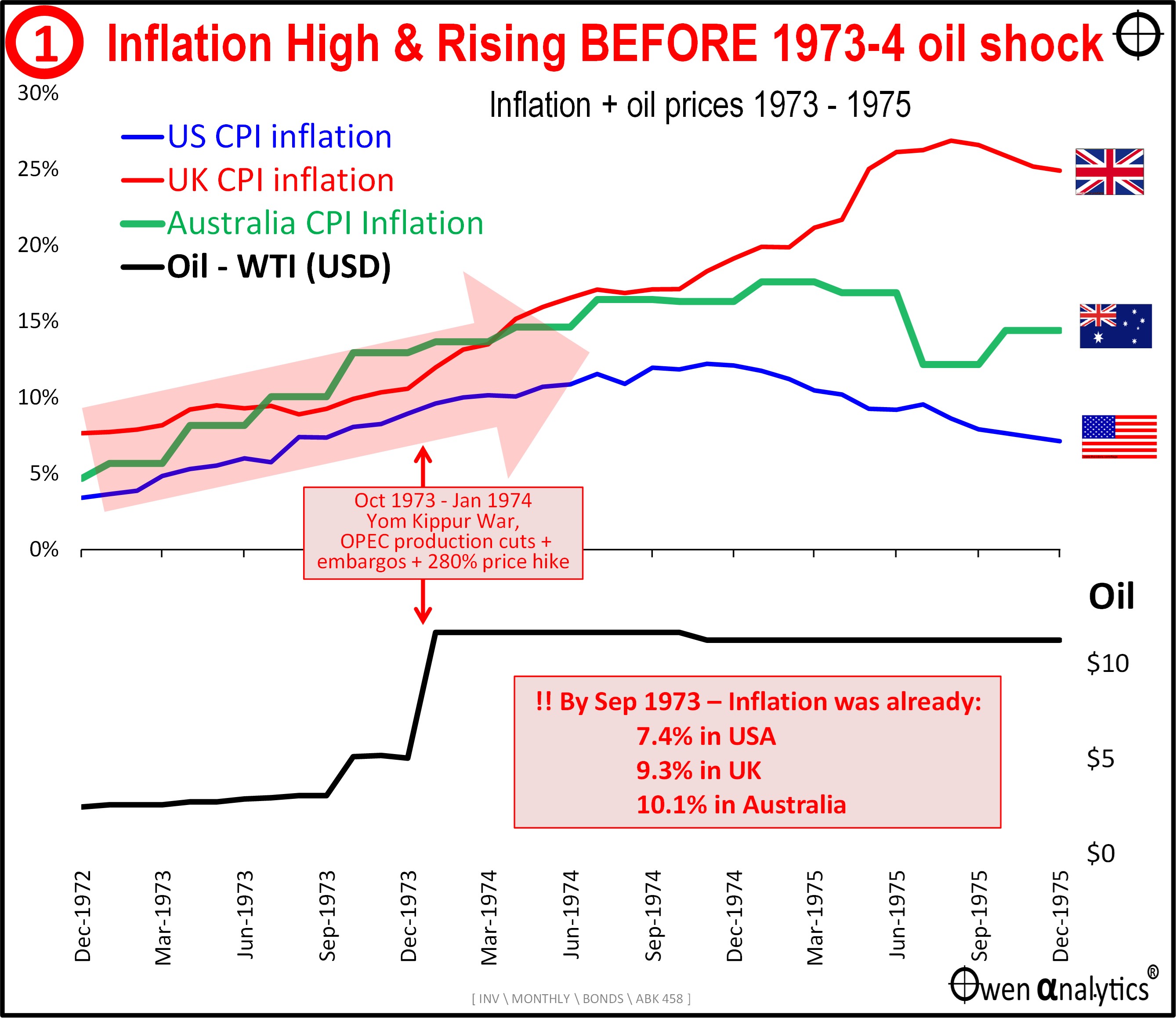

1973-74 oil shock

The main events included:

- The ‘Yom Kippur’ War (6-25 October 1973) in which Arab states led by Egypt and Syria (and backed by USSR) attacked Israel (backed by US) to try to win back territory seized and occupied by Israel in the 1967 ‘Six-day war’.

- From 17 October to January 1974 – several initiatives by Saudi Arabia and other OPEC members to cut production, raise prices, and impose embargoes on US in retaliation for US backing Israel.

As a result of these measures, the benchmark oil price quadrupled from US$2.90 to $11.65. Here is what happened to oil prices and inflation before, during and after the crisis:

Impact of the oil price spike on inflation? Only a late contributor, NOT the primary cause. By September 1973 (before the oil shock), inflation was already running at very high and rising levels:

- 7.4% in USA

- 9.3% in UK

- 10.1% in Australia

The main reasons for rising inflation in the early 1970s included rising government spending from the mid-1960s (including tax-cuts, ‘nation-building’, social infrastructure, Vietnam War spending), some very poor and counter-productive policy responses to inflation in the early 1970s, and some monetary policy errors.

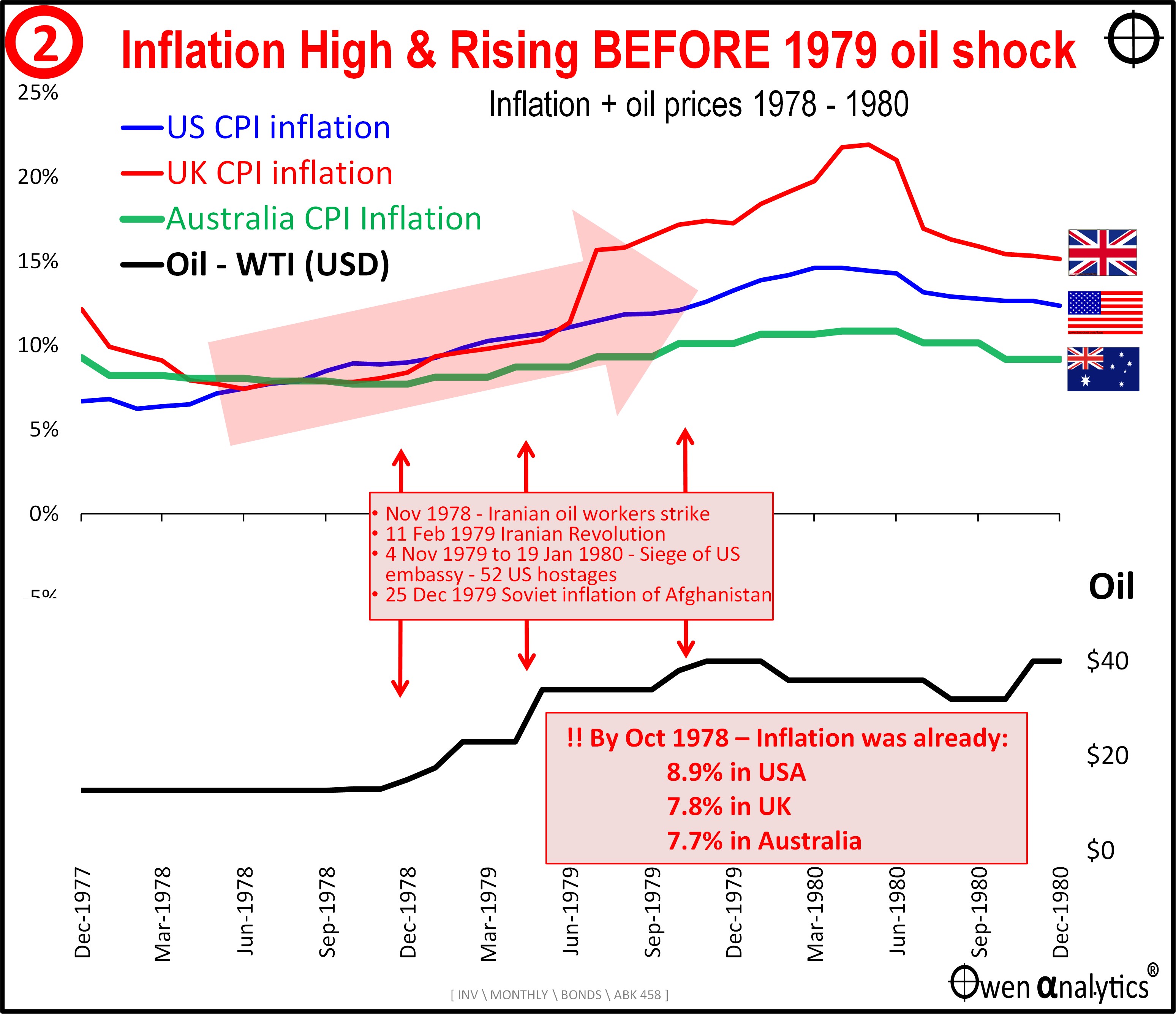

1979 oil shock

The main events in the late 1970s oil shock included:

- November 1978 Iranian oil worker’s strike.

- 11 Feb 1979 – Iranian Revolution, resulting in the overthrow of US/UK backed Shah of Iran (House of Pahlavi, which had ruled since 1941), and replaced Ayatollah Khomeini’s Islamic Republic.

- 4 Nov 1979 – Tehran students’ siege of US embassy, taking 52 US hostages who were finally rescued 444 days later on 19 Jan 1981 after several failed and costly attempts by the US.

- 22 Sep 1980 – Iraq (Saddam Hussein) invades Iran to capitalise on the revolutionary turmoil in Iran.

Here is what happened to oil prices and inflation before, during and after the crisis:

Impact of the oil price spike on inflation? Only late a contributor, NOT the primary cause. By October 1978 inflation was already running at:

- 8.9% in USA

- 7.8% in UK

- 7.7% in Australia

Once again, the real causes of the 1970s inflation and stagflation (simultaneous inflation and low economic growth) had their roots in the rising government spending from the mid-1960s, poor/counter-productive policy responses to inflation from the early 1970s, and monetary policy errors throughout the 1970s until the appointment of new Fed Chair Paul Volcker in August 1979.

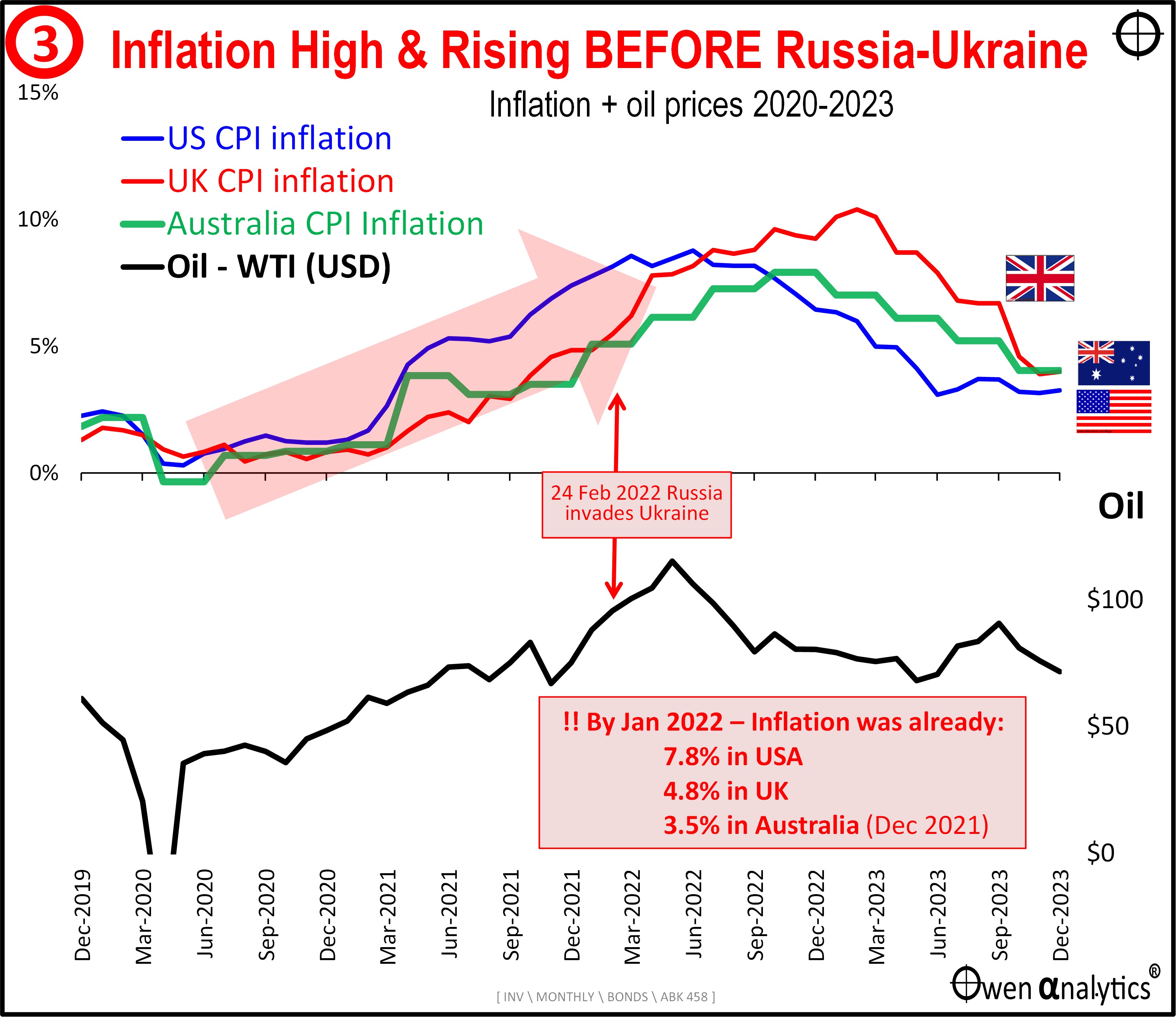

2022 Russian invasion of Ukraine

Likewise, inflation was already running out of control by the end of 2021, which was BEFORE Russia invaded Ukraine (February 2022).

Here is what happened to oil prices and inflation before, during and after the crisis:

Impact of the oil price spike on inflation? Only a later contributor, NOT the primary cause. By December 2021 which was BEFORE Russia invaded Ukraine (24 February 2022), inflation was already running at:

- 7.4% pa in USA (and annualised quarterly rate of 9.8% pa)

- 5.4% pa in UK (and an annualised quarterly rate of 9.4% pa).

- 3.5% pa in Australia (and an annualised quarterly rate of 5% pa).

Each of these were well above target ranges already. Nothing to do with Russia.

The post-Covid inflation was the result of ultra-loose fiscal policies (governments throwing money at anything that moved, running up wartime-like deficits and debts), plus ultra-loose monetary policies (central banks cutting interest rates to zero and even negative (Japan, Europe), artificially suppressing long rates with ‘QE’ money printing, handing out ultra-cheap loans to banks, etc).

There were also supply constraints that raised prices, but they were the direct and indirect results of government policies (lockdowns, closed borders, etc).

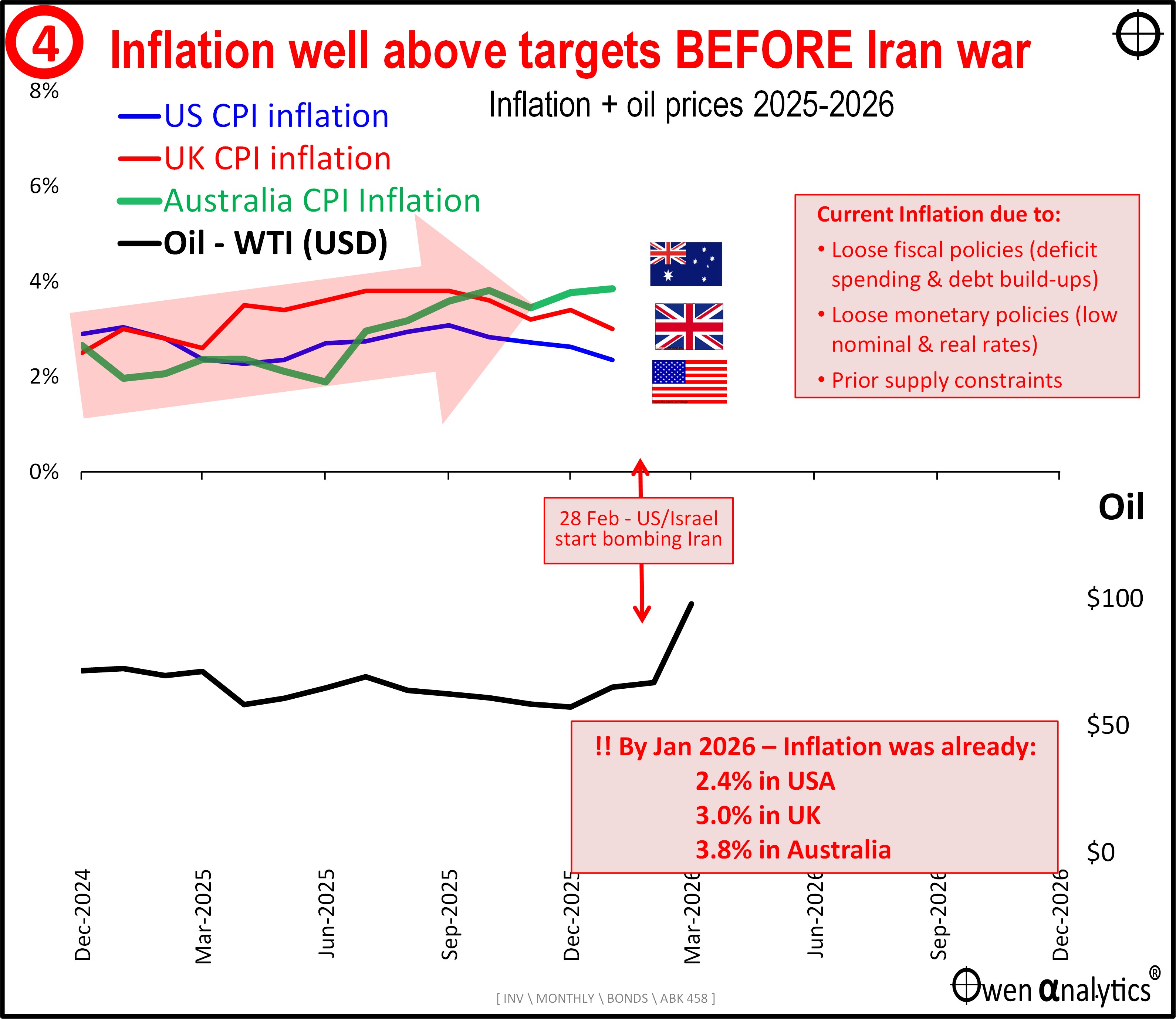

2026 War in Iran

Here we are again with inflation running above target here and in other countries – despite oil prices declining over the prior year, and now another oil price spike is about to let governments here and everywhere divert attention from the real causes of persistently high inflation.

Oil prices had been declining during 2025 but suddenly shot up to $120 (for one day - Sunday 8 March 2026) but quickly fell back to $100, where it is now (13 March). This is still below the price peaks in early 2022 after Russia’s invasion of Ukraine.

Here is the current picture on oil prices and inflation:

By January 2026 (before the end of Feb 2026 start of US/Israeli bombing of Iran), inflation was already running well above target:

- 2.4% in the USA

- 3% in the UK,

- 3.8% in Australia.

And that was with oil prices falling over the previous year while inflation still remained stubbornly high.

Get ready for another barrage of lies and mis-directions that will blame the war in Iran and resultant oil price spike for rising inflation, interest rate hikes, and rising mortgage repayments.

Government ministers and even the RBA will start pointing mainly to ‘international events’ and ‘external influences’ out of their control.

Once again diverting attention from the real causes – uncontrolled, largely ill-directed, productivity-sapping government deficit spending sprees, plus still loose monetary policies (low nominal and real rates).

We deserve better!

Ashley Owen, CFA is Founder and Principal of OwenAnalytics. Ashley is a well-known Australian market commentator with over 40 years’ experience. This article is for general information purposes only and does not consider the circumstances of any individual. You can subscribe to OwenAnalytics Newsletter here.