Given all the bubble talk I thought it would be interesting to share a perspective and some data from a report I read this week. Morgan Stanley’s report Who is on the other side addresses several topics including bubbles.

There have been countless bubbles throughout history. Bubbles are caused by our natural tendencies as humans and if we are still making decisions bubbles will continue to occur. The problem we face as investors is we know bubbles will occur but can’t definitively identify a bubble until after it has popped.

Famed economist Eugene Fama described this conundrum:

I think most bubbles are twenty-twenty hindsight. Now after the fact you always find people who said before the fact that prices are too high. People are always saying that prices are too high. When they turn out to be right, we anoint them. When they turn out to be wrong, we ignore them. They are typically right and wrong about half the time.

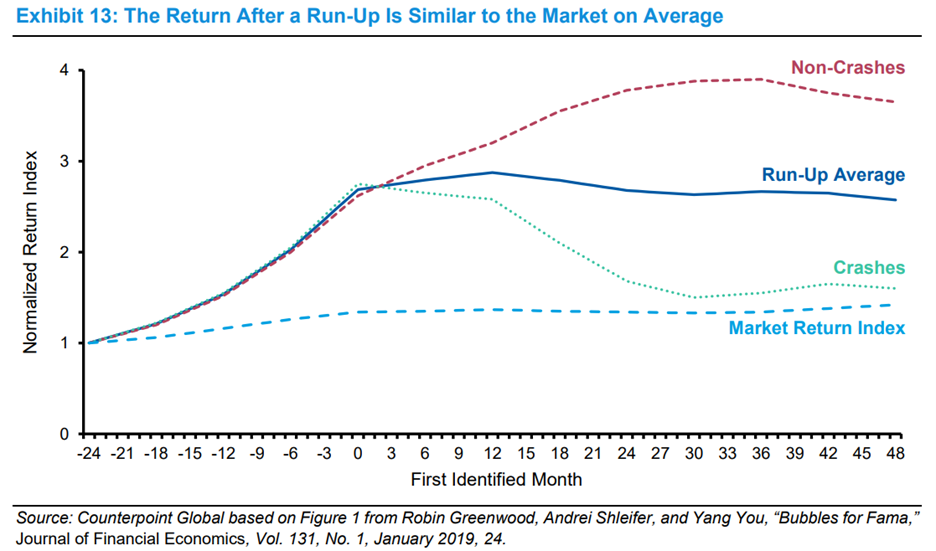

Fama didn’t have the data when he made that statement, but three researchers named Robin Greenwood, Andrei Shleifer and Yang You looked at what happened after periods of high returns.

A period of high returns was defined as a portfolio of shares in an industry returning 100% or more on a relative or absolute basis over two years. To eliminate the impact of a bounce off substantial lows the study authors also stipulated the industry’s absolute returns were 50% or more over the previous five years.

Between 1926 and 2014 there were 40 industries that meet their criteria in the US. Outside the US the researchers identified 107 scenarios between 1985 and 2014. Fama turned out to be right – in only half of the ‘bubbles’ a crash occurred. The researchers defined a crash as a 40% fall at some point in the two years following the period of high returns.

A normalised return index on the y-axis shows how an investment performs compared to a common starting point. As you can see the run-up average between the crash and non-crash outcomes looks similar to the overall market return index.

Talking about bubbles is one thing. Dramatically changing your portfolio is another. Incorrectly identify a bubble that doesn’t happen and it could make a dramatic difference in your investment outcomes.

New rules for a new era

Index providers have rules stipulating when new companies can join an index. For instance, the S&P 500 rules require 12 months of seasoning before a new company is included. The purpose of this seasoning is to avoid the volatility that often accompanies an IPO and to avoid hype-driven inclusion in the index.

The S&P 500 index also requires companies to be profitable on a GAAP (Generally Accepted Accounting Principles) basis. This rule is designed to only include mature and high-quality companies.

In what is shaping up to be a massive year for IPOs the S&P 500 has a problem. The first giant IPO, SpaceX, doesn’t meet the index criteria. Following a round of consultation which just ended Dow Jones S&P may let this new and wildly unprofitable company into the index.

If the S&P 500 caves they will follow the NASDAQ and FTSE indexes who have already changed their rules. And SpaceX is only the tip of the iceberg. The index providers are anticipating IPOs from Anthropic and OpenAI.

I know feigning outrage is in vogue. But I’m not a purist who thinks rules should never change. I don’t really care what the index providers do although I do own some index products tracking the S&P 500.

But I do think it is telling when the rules are changed in a hype-driven market to include companies that embody that hype.

Passive investors aren’t supposed to care about individual companies. Which is why I don’t care what happens with SpaceX in the portion of my portfolio that tracks an index.

But maybe this will make some ‘passive’ investors happy. They can say they own SpaceX and talk about the synergies between rockets, mobile broadband, Twitter and AI.

Or maybe this strange conglomeration of businesses that people are desperate to own is a product of a time which will look foolish in retrospect.

Mark LaMonica

Also in this week's edition...

The government’s tax proposal is supposed to help younger generations. Lauchlan Mackinnon explores the validity of these claims.

Shani Jayamanne sits down with Abbey John to learn the different ways you can minimise tax with a will.

Many investors are turning to AI to assist with investment decisions. Larry Swedroe doesn’t think AI can help you pick winning funds… but he does think AI can help avoid the losers.

Ashely Owen is back and turning his attention to inflation. According to Ashley Boomers got lucky and the next generations won’t be so fortunate.

The cost of financial advice continues to increase but expanded tax deductibility will increase affordability according to Sarah Abood.

Dr Joanne Earl returns with an update on her retirement.

Richard Holden argues the government has created the first ever productivity tax. He goes through the implications for young Australians.

This week's white paper is Capital Group's analysis of company dividends worldwide, as part of its broader Global Equity Study.

Curated by Mark LaMonica, Simonelle Mody and Leisa Bell

***

Weekend market update

From Diana Mousina, AMP

Whatever fragile ceasefire between the US and Iran cracked wide open this week - with Iranian strikes on Kuwait and Bahrain, Israeli strikes in Lebanon and a US strike on an oil tanker headed to the Islamic Republic. One day Trump asserts that a deal is close or in the final stages, the next there are threats to keep the Strait of Hormuz closed until US Labor Day in September. In any case, Iranian-backed militant group Hezbollah said they had rejected the US conditions.

Financial markets, though, seem to have moved on from deal-watching. The working assumption is that an agreement happens eventually, and in the meantime, investors are refocussing on what they can actually measure - underlying economic data and company profits – both of which are holding up well. The US data is looking like its turning up rather than down.

Nevertheless, let’s not forget that we are still in the midst of an oil shock, with very little vessel traffic going through the Strait of Hormuz which dipped again this week.

Despite the lack of supply, oil prices remain in a range between $90-$110/barrel and analysts continue to expect prices to continue trending down. This does show that the oil market was oversupplied prior to the start of the conflict and that oil has bypassed the Strait through other methods (like pipeline) and utilising reserves.

There is still the risk that the longer the ~10% oil supply hit continues that oil prices shoot up and then cause a bigger problem for global growth and inflation. The current disruption remains one of the biggest and longest in history.

In the meantime, US shares continue to dominate. Over the week, the S&P500 was flat but reached a record-high mid-week and is up 11% since the beginning of the year. Although this doesn’t compare to the parabolic performance of Korean equities, up 91% year to date from the semiconductor demand boom. Australia is massive laggard from rate hikes and recent budget tax concerns, despite better profit growth. The ASX200 was down by 1% this week, with gains in tech, consumer staples, energy and healthcare but more falls in financials (banks), real estate and materials.

It’s hard to get too negative on sharemarkets, especially in the US. Sure there are still a lot of downside risks - like the war and oil prices and the subsequent lift in inflation and slowing in growth, AI bubble concerns, lack of central bank rate cuts and issues in the private credit space but to counter that – US activity indicators are looking better, there is still plenty of spending for AI with plenty of excitement lately for the upcoming listing of Musk’s SpaceX and Anthropic. We see shares continuing to trend higher, although the long list of concerns means that there will be periods of drawdowns.

It’s also helpful for shares that bond yields have been trending down again. US and Japan have seen the highest increase to yields this year, with the US 10-year at 4.46%.

Australia is no longer expected to be an outlier with rising interest rates. Markets are pricing in higher interest rates globally, which is keeping yields elevated. This week, US Fed regional president Logan, spoke hawkishly about the outlook for rates and she sees the risk for higher interest rates later this year. Another Governor Williams was more neutral. Kevin Warsh, the new Fed Chair, will hold his first meeting as Chair in a few weeks so there may be some changes to Fed communication and focus ahead.

Bringing it back home, the House of Representatives passed the Labour government contentious budget tax changes and this bill will now go to the Senate, where it is likely to be met with more of a challenge because Labor does not have a majority in the House and needs crossbench support (primarily from Greens).

Interestingly, the May Westpac Melbourne Institute consumer sentiment survey which was conducted after the budget showed a rise in confidence for those aged 18-24 and 25-44, while confidence was flat for those aged over 45. Maybe it’s all the negative talkback in the weeks post-Budget that has gotten people down more and that was reflected in the poll result.

More rate hikes needed in Australia? The Fair Work Commission announced a larger-than-inflation increase to minimum (+6%) and award wages (+4.75%) starting from 1 July. This is larger than last year’s increase of 3.5% and exceed the industry submissions to the Fair Work Commission (which were around 3.7%), although were closer to the ACTU’s proposed 6% increase. The change impacts around 12% of Australia’s wage bill. However, this increase is likely to lead to a similar rise in enterprise bargaining agreement rates (some of which are derived from award rates) through the “signalling” effect as people demand wage increases on par with others, and this includes the private sector too. This is what happened in 2023.

Of course, the labour market has to be strong enough to allow people to demand higher wages (without losing their jobs). While labour market conditions have eased a little in Australia, the unemployment rate remains very low, and many industries are finding it hard to employ the right people. So there appears to be little excess capacity, which means businesses will need to lift wages (we now see annual wages growth accelerating to 3.7% later this year) and increase costs to pay for these increases. All of which means higher inflation. We are now allowing for 2 more rate increases from the RBA, with the next one to occur most likely in August followed up by another hike in November.

Latest updates

PDF version of Firstlinks Newsletter

Monthly Investment Podcast by UniSuper

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Plus updates and announcements on the Sponsor Noticeboard on our website